01

MethodologyHow they did it

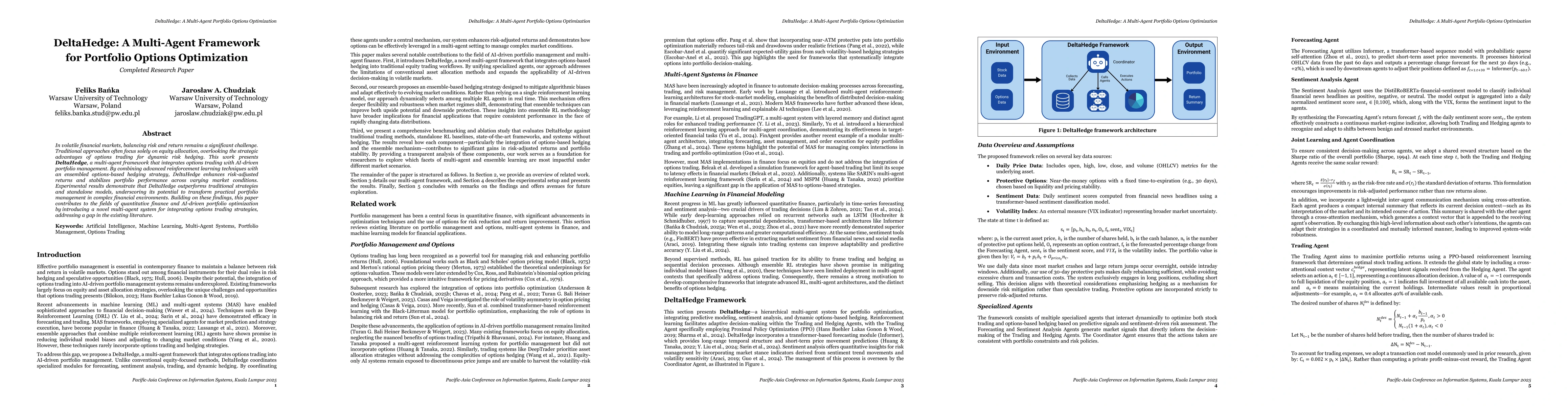

The research introduces DeltaHedge, a hierarchical multi-agent framework combining reinforcement learning with options trading. It employs specialized agents for forecasting, sentiment analysis, trading, and hedging, with an ensemble mechanism selecting optimal hedging policies. Data sources include stock prices, sentiment analysis, and options data, validated through empirical testing on S&P 500, Apple, and Tesla.

Discussion 0