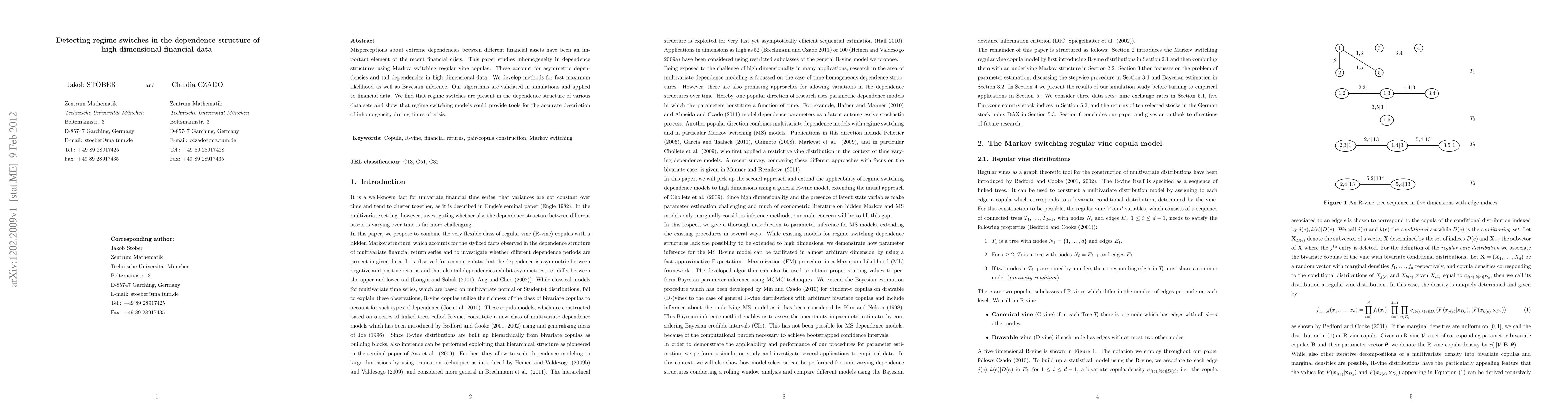

Detecting regime switches in the dependence structure of high dimensional financial data

Publication

Metrics

AI Quick Summary

This paper develops methods to detect regime switches in the dependence structure of high-dimensional financial data using Markov switching regular vine copulas, which account for asymmetric and tail dependencies. The proposed fast maximum likelihood and Bayesian inference algorithms are validated and applied to financial data, revealing the presence of regime switches and suggesting their utility in accurately describing inhomogeneity during crises.

Paper Preview

Abstract

Misperceptions about extreme dependencies between different financial assets have been an im- portant element of the recent financial crisis. This paper studies inhomogeneity in dependence structures using Markov switching regular vine copulas. These account for asymmetric depen- dencies and tail dependencies in high dimensional data. We develop methods for fast maximum likelihood as well as Bayesian inference. Our algorithms are validated in simulations and applied to financial data. We find that regime switches are present in the dependence structure of various data sets and show that regime switching models could provide tools for the accurate description of inhomogeneity during times of crisis.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0