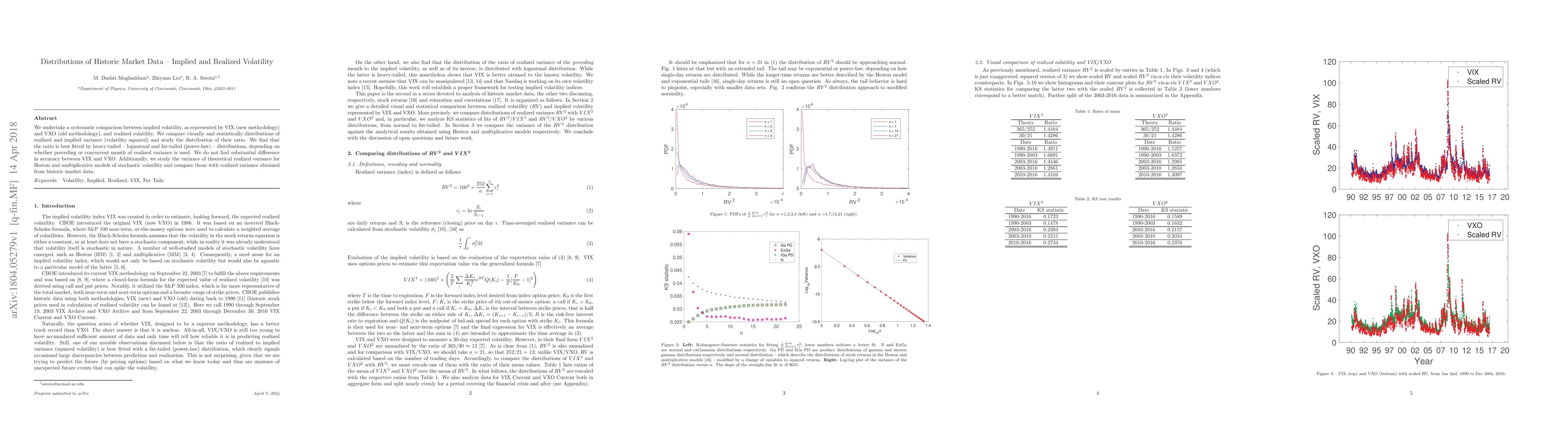

We undertake a systematic comparison between implied volatility, as

represented by VIX (new methodology) and VXO (old methodology), and realized

volatility. We compare visually and statistically distributions of realized and

implied variance (volatility squared) and study the distribution of their

ratio. We find that the ratio is best fitted by heavy-tailed -- lognormal and

fat-tailed (power-law) -- distributions, depending on whether preceding or

concurrent month of realized variance is used. We do not find substantial

difference in accuracy between VIX and VXO. Additionally, we study the variance

of theoretical realized variance for Heston and multiplicative models of

stochastic volatility and compare those with realized variance obtained from

historic market data.

Discussion 0