Dynamic loan portfolio management in a three time step model

Publication

Metrics

AI Quick Summary

This paper investigates a three-time-step model for dynamic loan portfolio management in banks, focusing on decisions made at the intermediate time step to meet short-term obligations and regulatory capital requirements. The study explores the impact of raising new equity and debt, showing that these actions can either increase or decrease return on equity depending on the circumstances, while ensuring equity holders' constraints to prevent default.

Paper Preview

Abstract

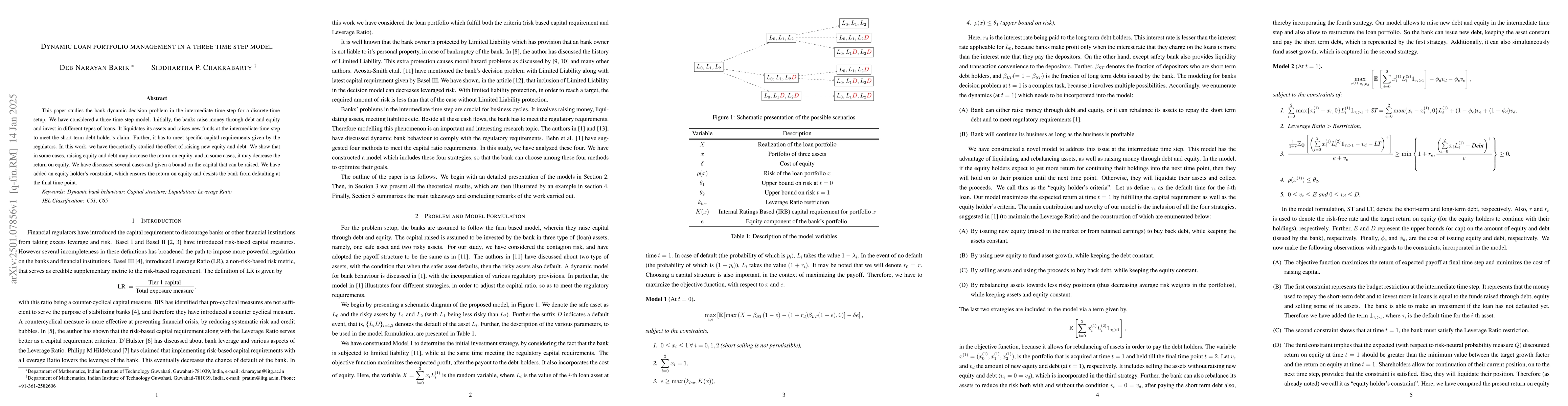

This paper studies the bank dynamic decision problem in the intermediate time step for a discrete-time setup. We have considered a three-time-step model. Initially, the banks raise money through debt and equity and invest in different types of loans. It liquidates its assets and raises new funds at the intermediate-time step to meet the short-term debt holders claim. Further, it has to meet specific capital requirements given by the regulators. In this work, we have theoretically studied the effect of raising new equity and debt. We show that in some cases, raising equity and debt may increase the return on equity, and in some cases, it may decrease the return on equity. We have discussed several cases and given a bound on the capital that can be raised. We have added an equity holders constraint, which ensures the return on equity and desists the bank from defaulting at the final time point.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0