Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the context of whether investors are aware of carbon-related risks, it is often hypothesized that there may be a carbon premium in the value of stocks of firms, conferring an abnormal excess valu...

This paper proposes an algorithmic trading framework integrating Environmental, Social, and Governance (ESG) ratings with a pairs trading strategy. It addresses the demand for socially responsible i...

In this article, we consider the problem of a bank's loan portfolio in the context of liquidity risk, while allowing for the limited liability protection enjoyed by the bank. Accordingly, we constru...

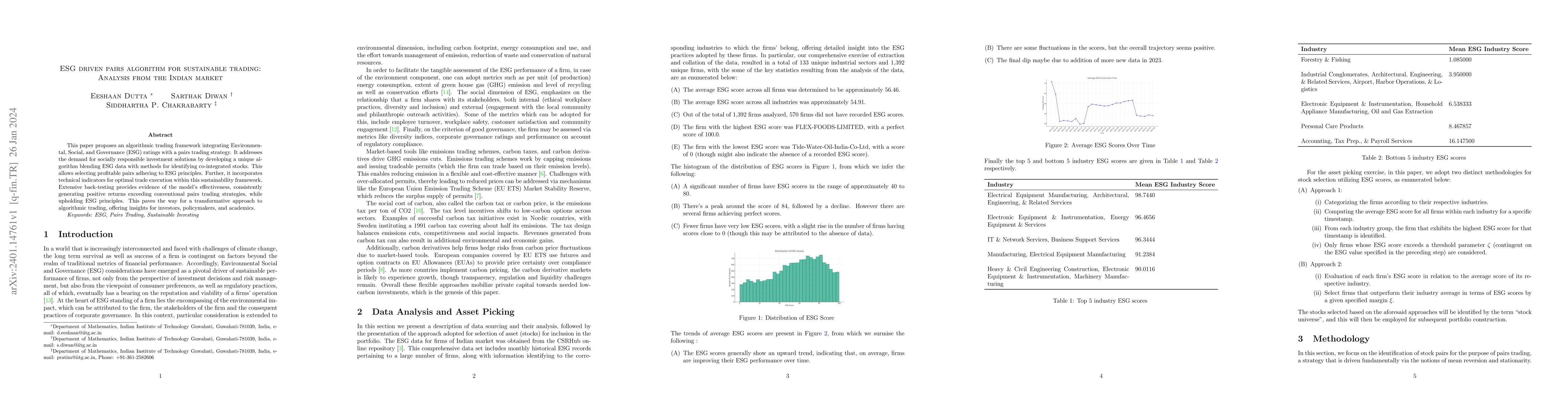

In this article, we present a novel approach for the construction of an environment-friendly green portfolio using the ESG ratings, and application of the modern portfolio theory to present what we ...

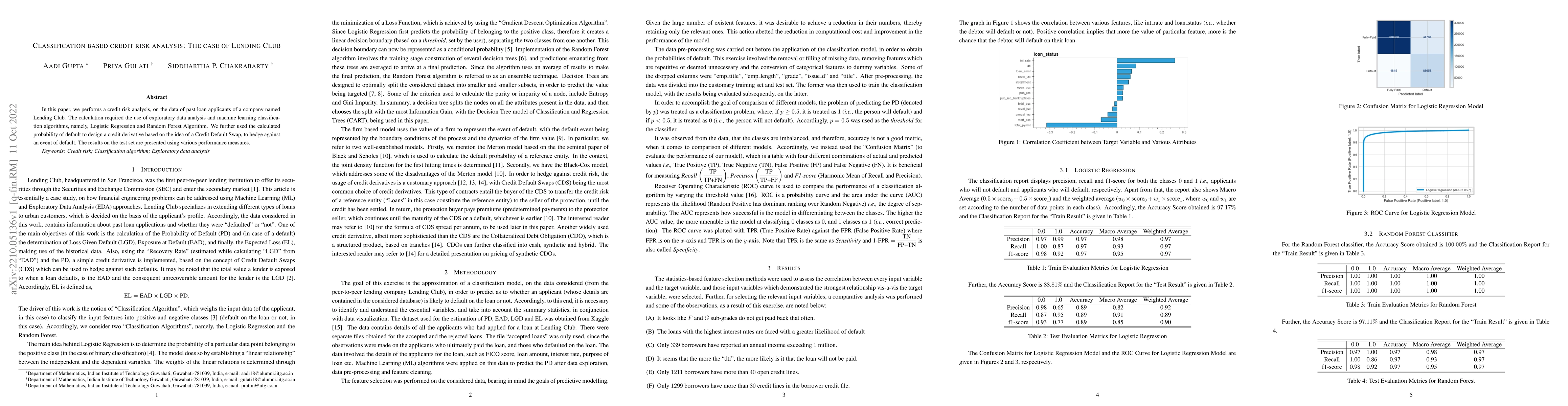

In this paper, we performs a credit risk analysis, on the data of past loan applicants of a company named Lending Club. The calculation required the use of exploratory data analysis and machine lear...

In this article, we present a review of the recent developments on the topic of Multilevel Monte Carlo (MLMC) algorithm, in the paradigm of applications in financial engineering. We specifically foc...

Return-risk models are the two pillars of modern portfolio theory, which are widely used to make decisions in choosing the loan portfolio of a bank. Banks and other financial institutions are subjec...

In this paper, we propose and analyze a novel combination of multilevel Richardson-Romberg (ML2R) and importance sampling algorithm, with the aim of reducing the overall computational time, while ac...

Chronic Myeloid Leukemia (CML) is a biphasic malignant clonal disorder that progresses, first with a chronic phase, where the cells have enhanced proliferation only, and then to a blast phase, where...

This paper empirically analyzes a dataset published by the European Banking Authority. Our main aim was to study how the Leverage Ratio is affected by adverse financial scenarios. This was be follow...

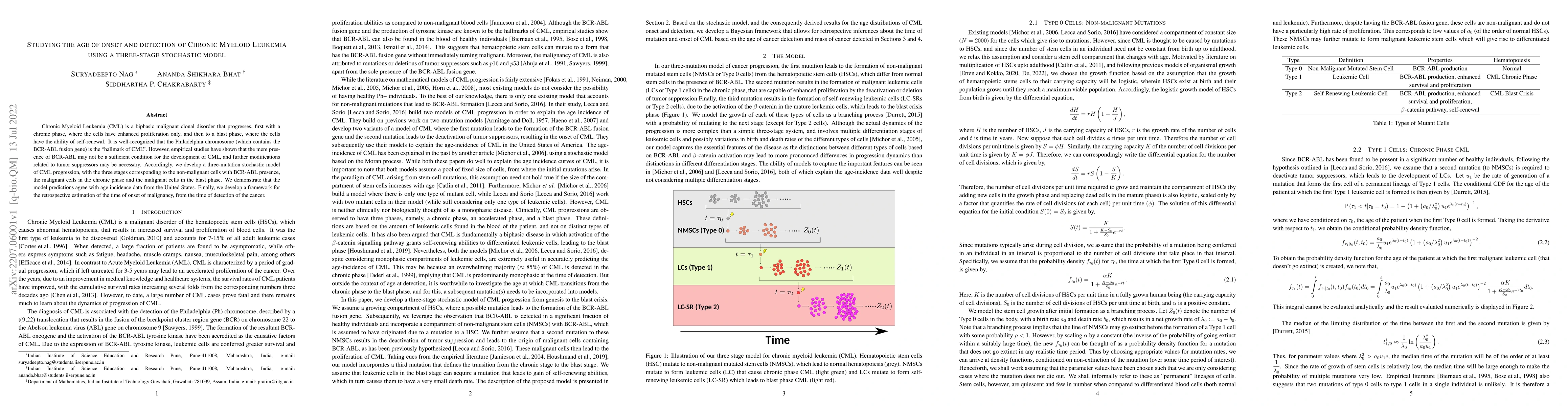

We present a three-stage probabilistic model for the progression of Chronic Myeloid Leukemia (CML), as manifested by the leukemic stem cells, progenitor cells and mature leukemic cells. This progres...

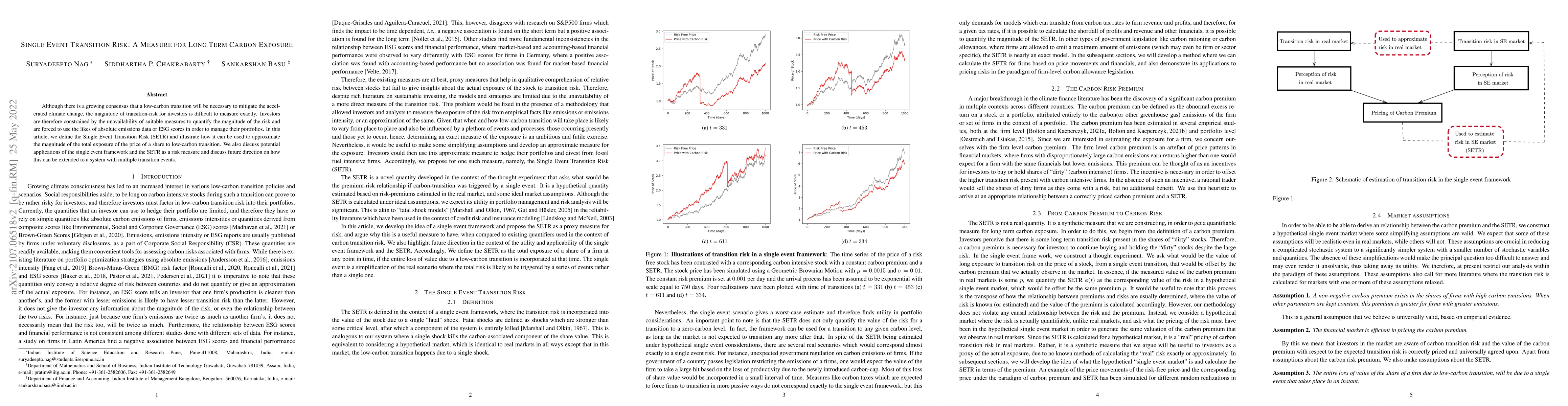

Although there is a growing consensus that a low-carbon transition will be necessary to mitigate the accelerated climate change, the magnitude of transition-risk for investors is difficult to measur...

We undertake an empirical analysis for the premium data of non-life insurance companies operating in India, in the paradigm of fitting the data for the parametric distribution of Lognormal and the e...

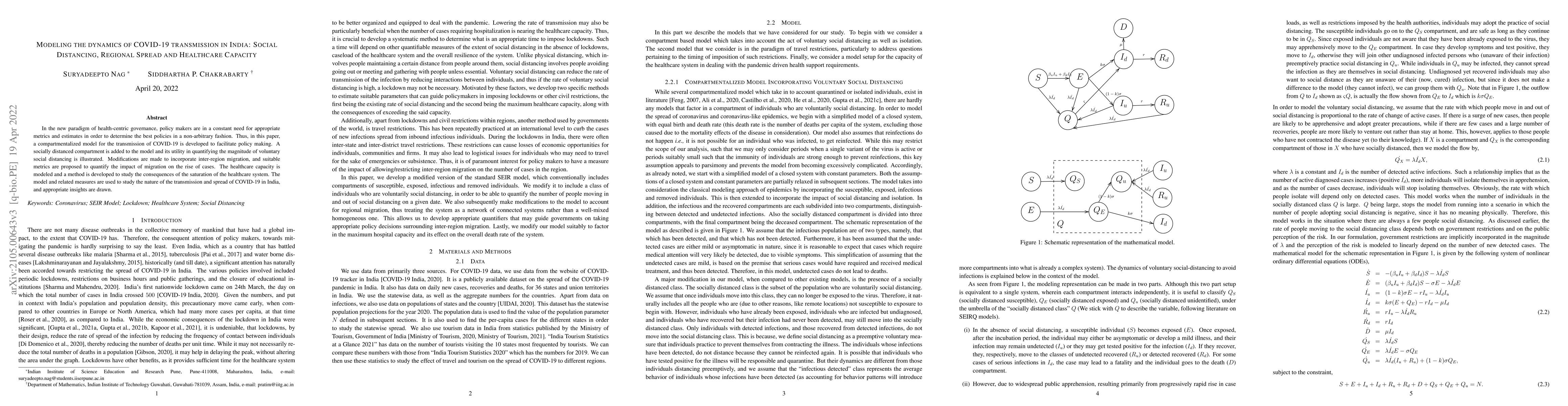

In the new paradigm of health-centric governance, policy makers are in a constant need for appropriate metrics and estimates in order to determine the best policies in a non-arbitrary fashion. Thus,...

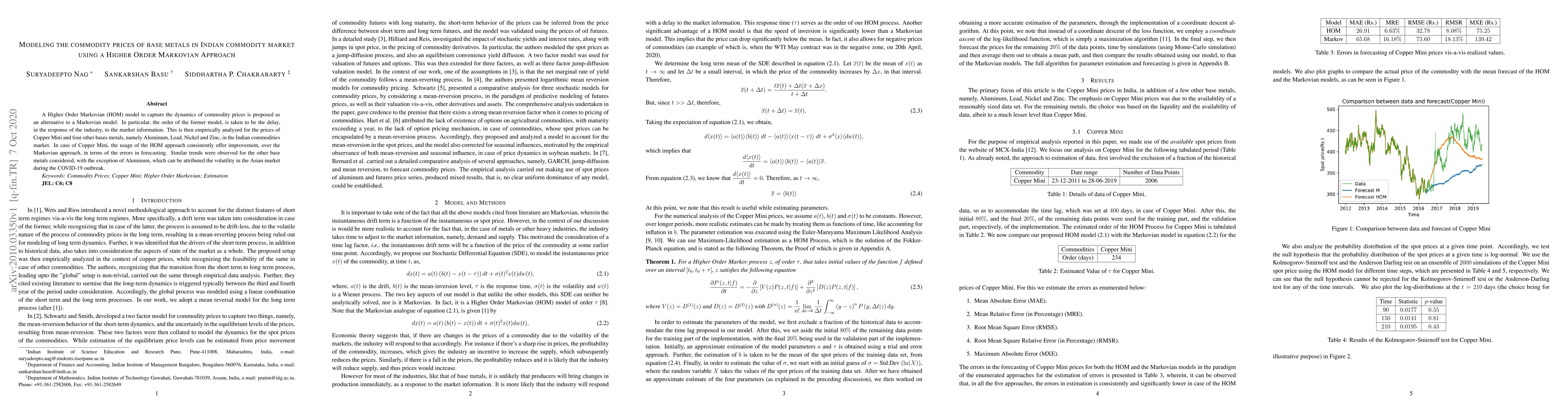

A Higher Order Markovian (HOM) model to capture the dynamics of commodity prices is proposed as an alternative to a Markovian model. In particular, the order of the former model, is taken to be the ...

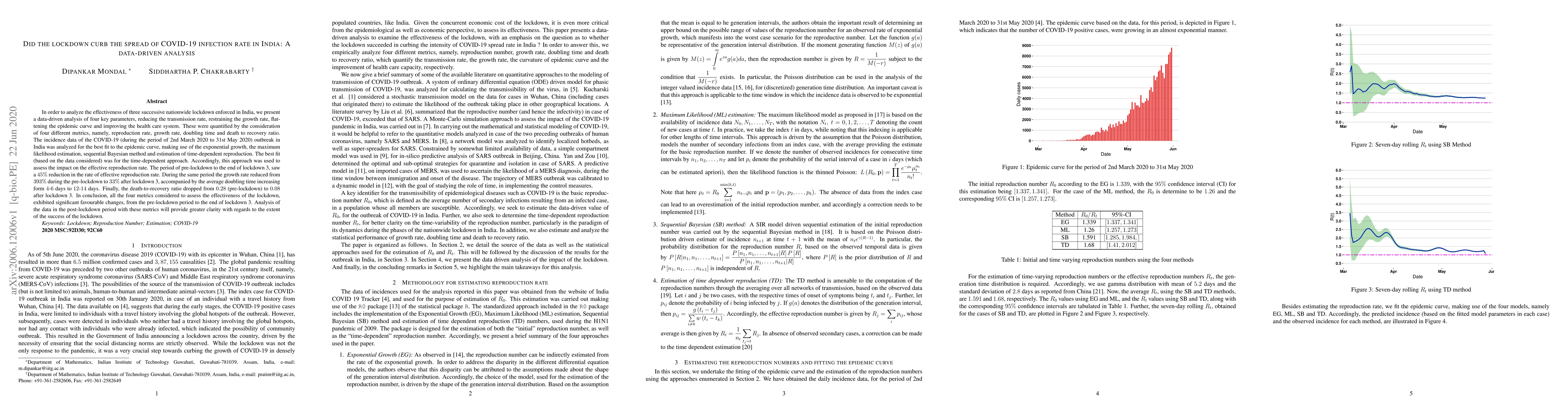

In order to analyze the effectiveness of three successive nationwide lockdown enforced in India, we present a data-driven analysis of four key parameters, reducing the transmission rate, restraining...

The problem of data uncertainty has motivated the incorporation of robust optimization in various arenas, beyond the Markowitz portfolio optimization. This work presents the extension of the robust ...

The emergence of robust optimization has been driven primarily by the necessity to address the demerits of the Markowitz model. There has been a noteworthy debate regarding consideration of robust a...

In this paper, we examine the Sample Average Approximation (SAA) procedure within a framework where the Monte Carlo estimator of the expectation is biased. We also introduce Multilevel Monte Carlo (ML...

This paper studies the bank dynamic decision problem in the intermediate time step for a discrete-time setup. We have considered a three-time-step model. Initially, the banks raise money through debt ...

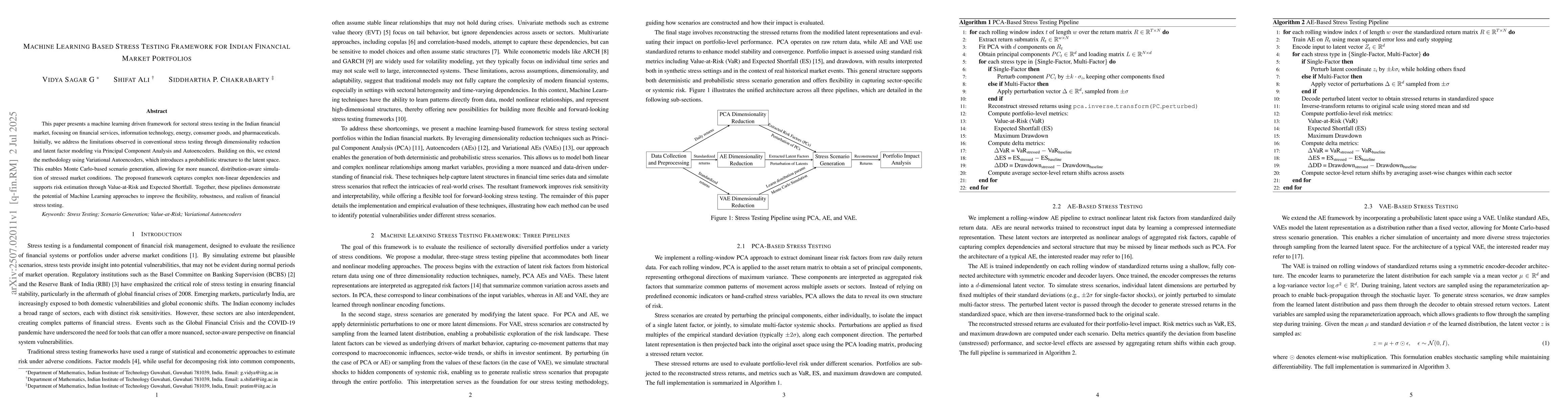

This paper presents a machine learning driven framework for sectoral stress testing in the Indian financial market, focusing on financial services, information technology, energy, consumer goods, and ...

A central challenge in Human Immunodeficiency Virus (HIV) public health policy lies in determining whether to universally expand treatment access, despite the risk of sub-optimal adherence and consequ...

We present a novel approach for the bank's decision problem, incorporating Limited Liability in the objective function. Accordingly, we consider continuous time models, with and without Limited Liabil...