01

MethodologyHow they did it

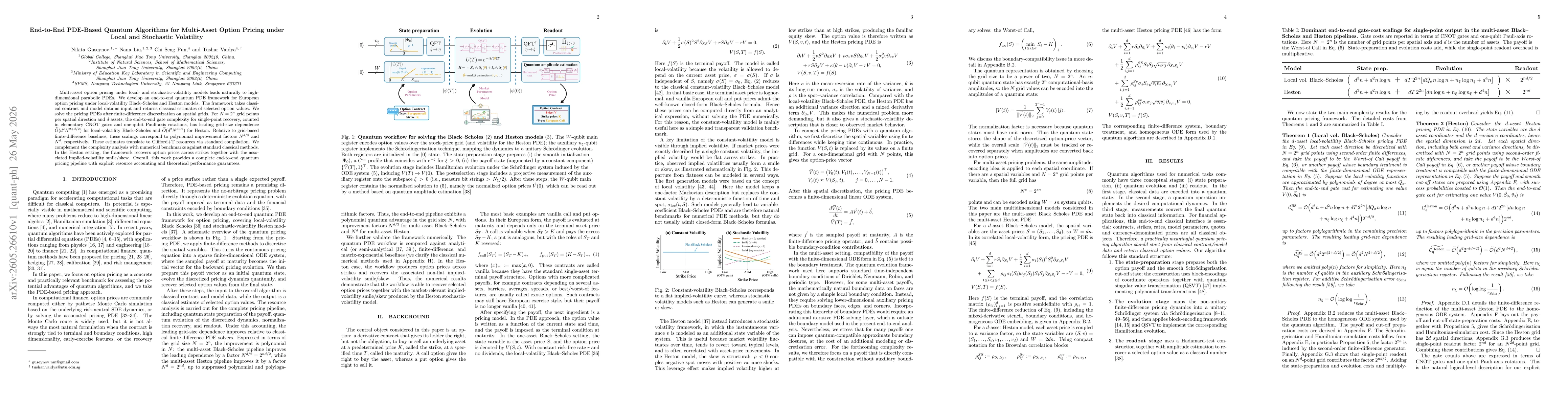

The study develops an end-to-end quantum PDE-based framework for European option pricing under local-volatility Black-Scholes and Heston models. It discretizes spatial variables via finite differences to obtain a sparse ODE system, encodes the terminal payoff as an initial quantum state, evolves the system quantum-mechanically, and recovers prices from the final state using amplitude estimation. Resource accounting includes state preparation, Hamiltonian evolution, normalization, and readout, with complexity analyzed in terms of grid size N and asset count d, and complemented by numerical benchmarks against classical methods.

Discussion 0