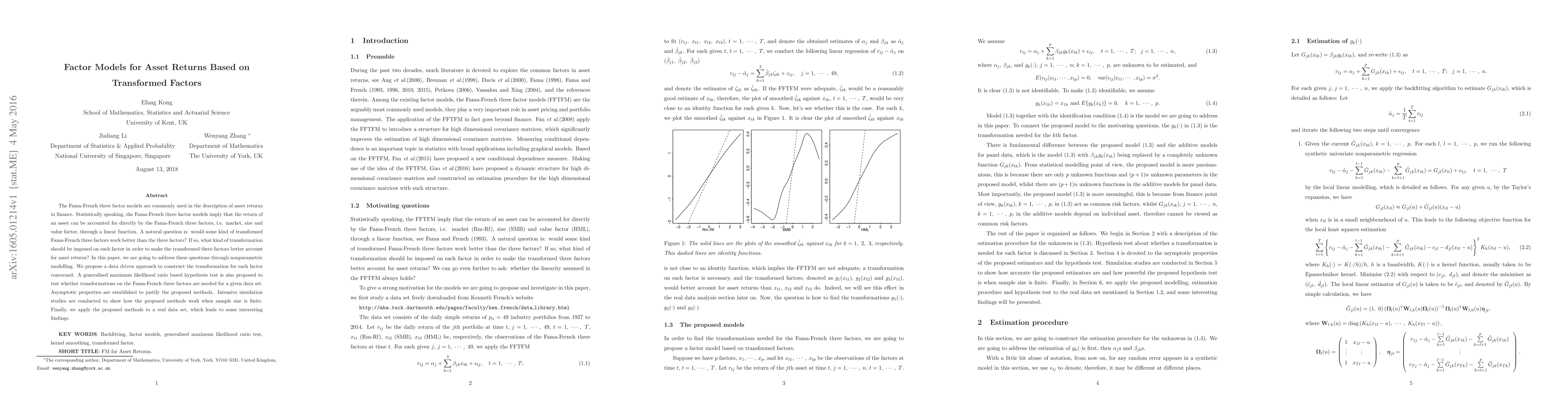

The Fama-French three factor models are commonly used in the description of

asset returns in finance. Statistically speaking, the Fama-French three factor

models imply that the return of an asset can be accounted for directly by the

Fama-French three factors, i.e. market, size and value factor, through a linear

function. A natural question is: would some kind of transformed Fama-French

three factors work better than the three factors? If so, what kind of

transformation should be imposed on each factor in order to make the

transformed three factors better account for asset returns? In this paper, we

are going to address these questions through nonparametric modelling. We

propose a data driven approach to construct the transformation for each factor

concerned. A generalised maximum likelihood ratio based hypothesis test is also

proposed to test whether transformations on the Fama-French three factors are

needed for a given data set. Asymptotic properties are established to justify

the proposed methods. Intensive simulation studies are conducted to show how

the proposed methods work when sample size is finite. Finally, we apply the

proposed methods to a real data set, which leads to some interesting findings.

Discussion 0