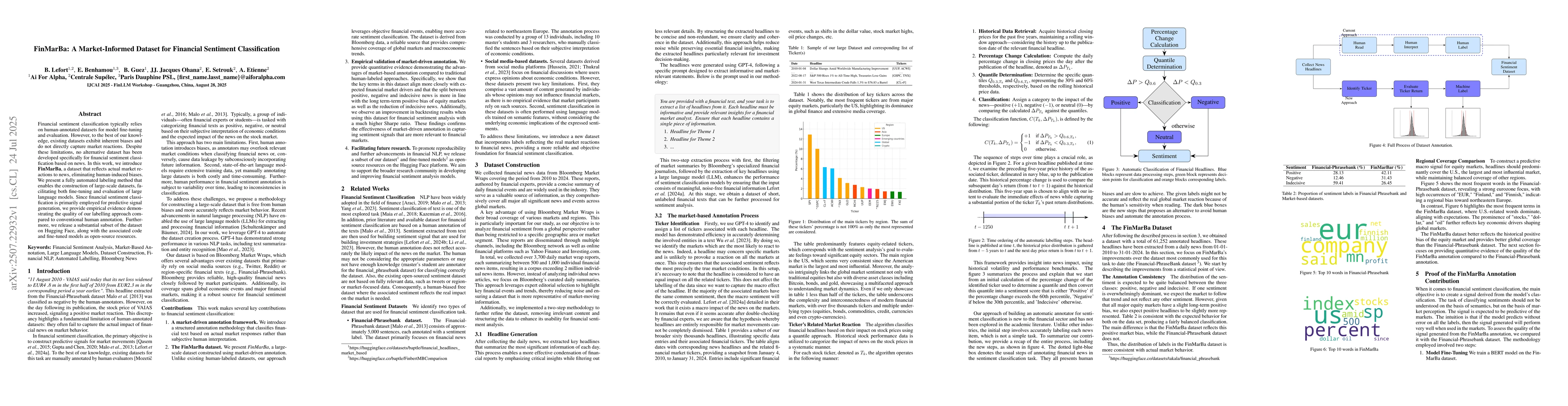

FinMarBa: A Market-Informed Dataset for Financial Sentiment Classification

Publication

Metrics

Paper Preview

Abstract

This paper presents a novel hierarchical framework for portfolio optimization, integrating lightweight Large Language Models (LLMs) with Deep Reinforcement Learning (DRL) to combine sentiment signals from financial news with traditional market indicators. Our three-tier architecture employs base RL agents to process hybrid data, meta-agents to aggregate their decisions, and a super-agent to merge decisions based on market data and sentiment analysis. Evaluated on data from 2018 to 2024, after training on 2000-2017, the framework achieves a 26% annualized return and a Sharpe ratio of 1.2, outperforming equal-weighted and S&P 500 benchmarks. Key contributions include scalable cross-modal integration, a hierarchical RL structure for enhanced stability, and open-source reproducibility.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0