Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces a new risk-on risk-off strategy for the stock market, which combines a financial stress indicator with a sentiment analysis done by ChatGPT reading and interpreting Bloomberg d...

We used a dataset of daily Bloomberg Financial Market Summaries from 2010 to 2023, reposted on large financial media, to determine how global news headlines may affect stock market movements using C...

While researchers in the asset management industry have mostly focused on techniques based on financial and risk planning techniques like Markowitz efficient frontier, minimum variance, maximum dive...

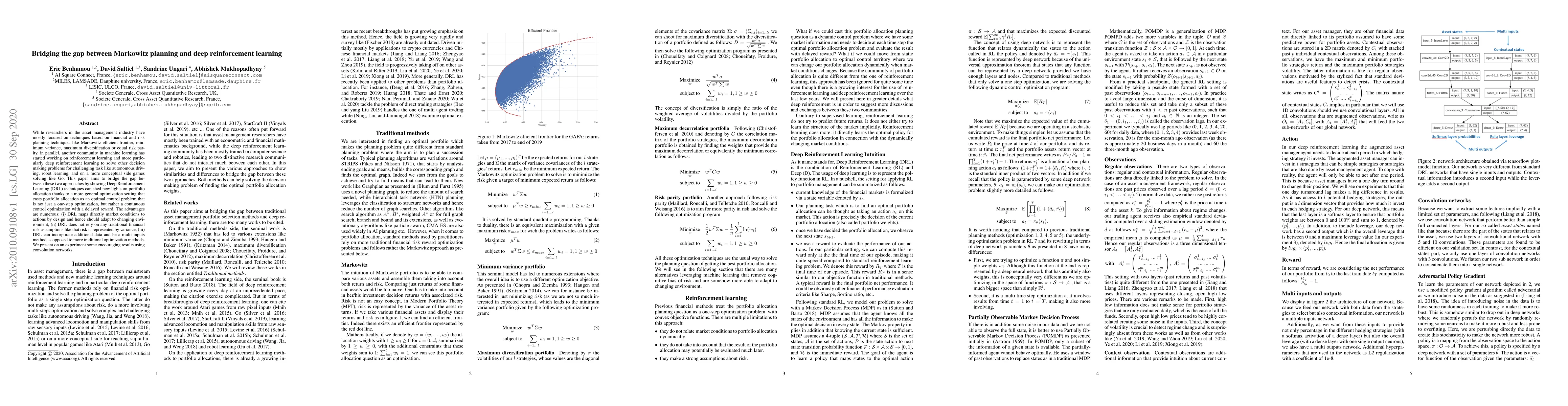

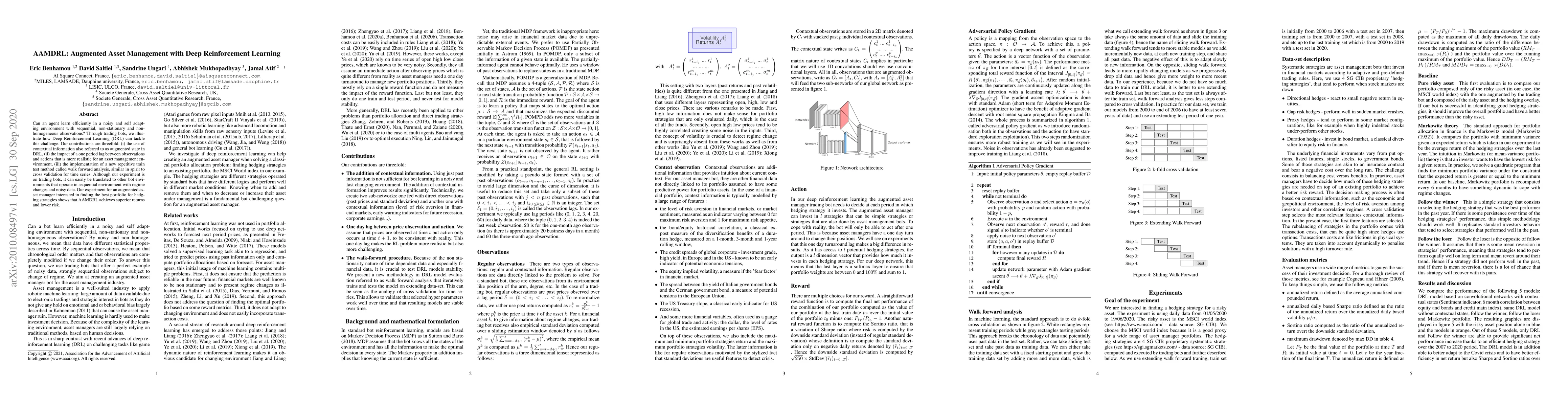

Can an agent learn efficiently in a noisy and self adapting environment with sequential, non-stationary and non-homogeneous observations? Through trading bots, we illustrate how Deep Reinforcement L...

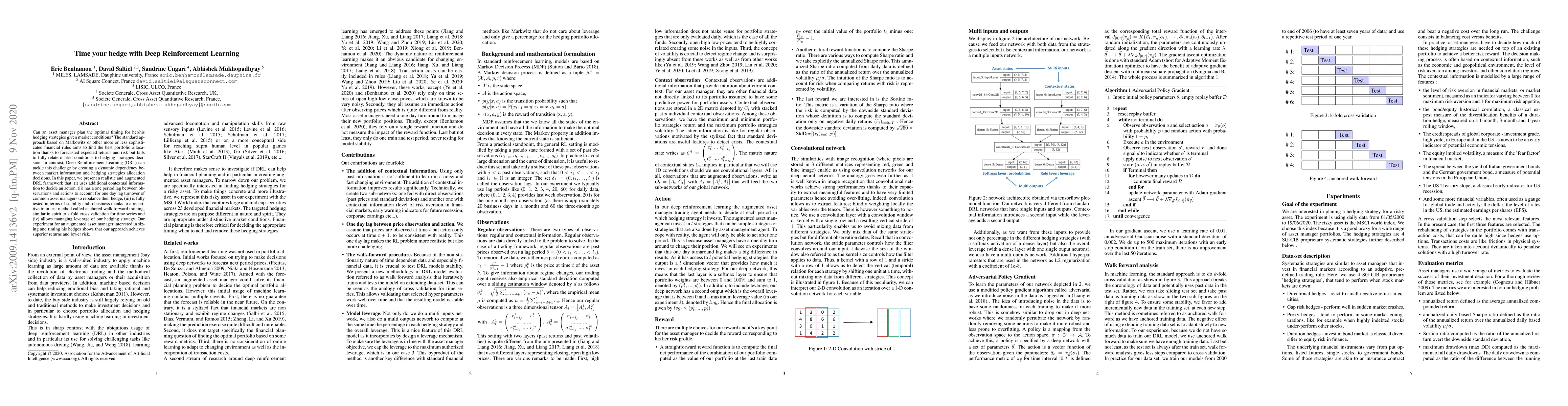

Can an asset manager plan the optimal timing for her/his hedging strategies given market conditions? The standard approach based on Markowitz or other more or less sophisticated financial rules aims...

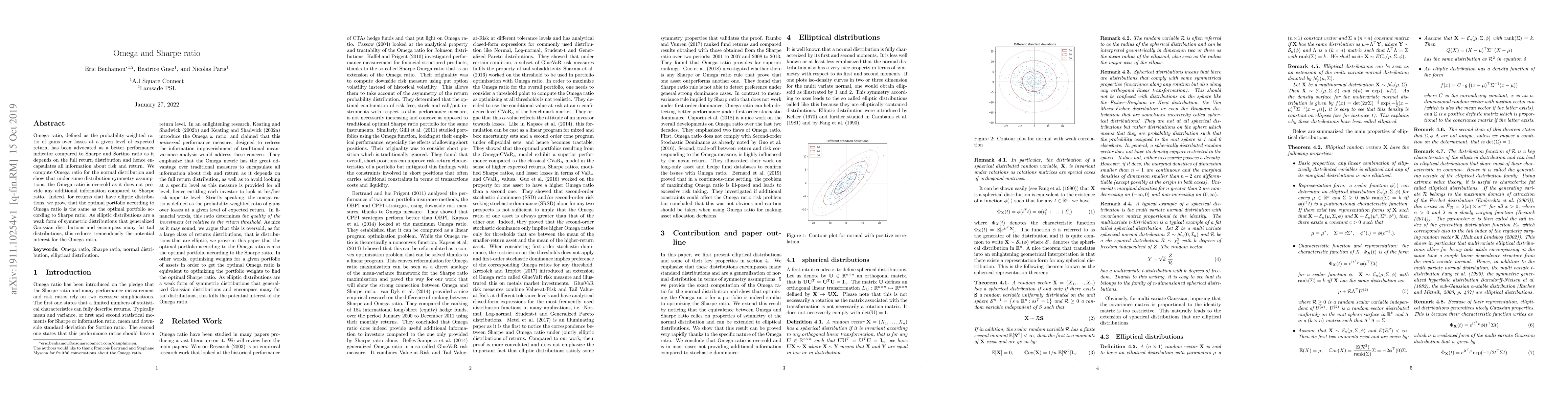

Omega ratio, defined as the probability-weighted ratio of gains over losses at a given level of expected return, has been advocated as a better performance indicator compared to Sharpe and Sortino r...

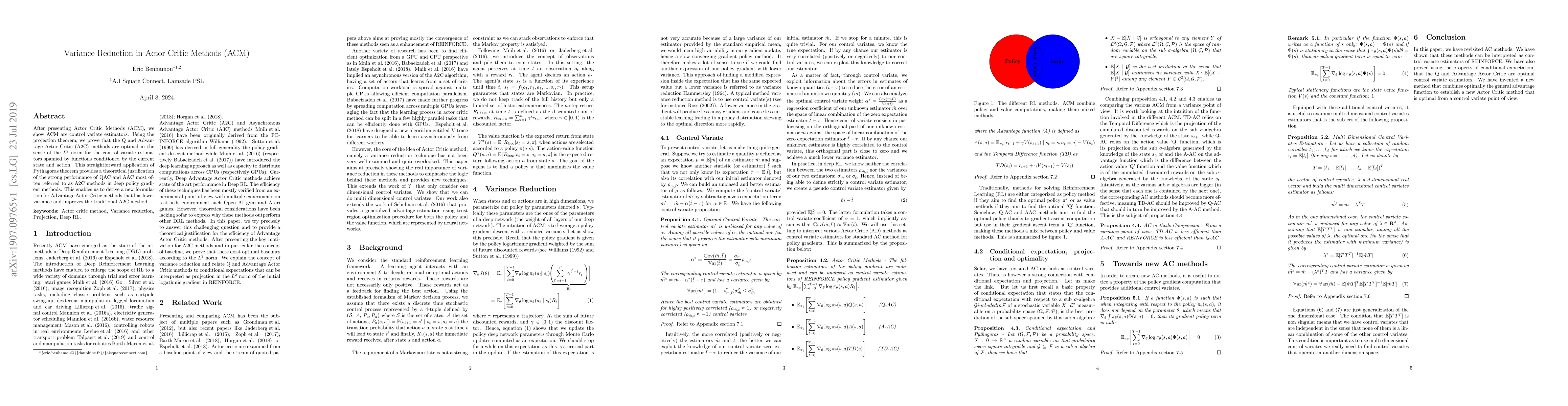

After presenting Actor Critic Methods (ACM), we show ACM are control variate estimators. Using the projection theorem, we prove that the Q and Advantage Actor Critic (A2C) methods are optimal in the...

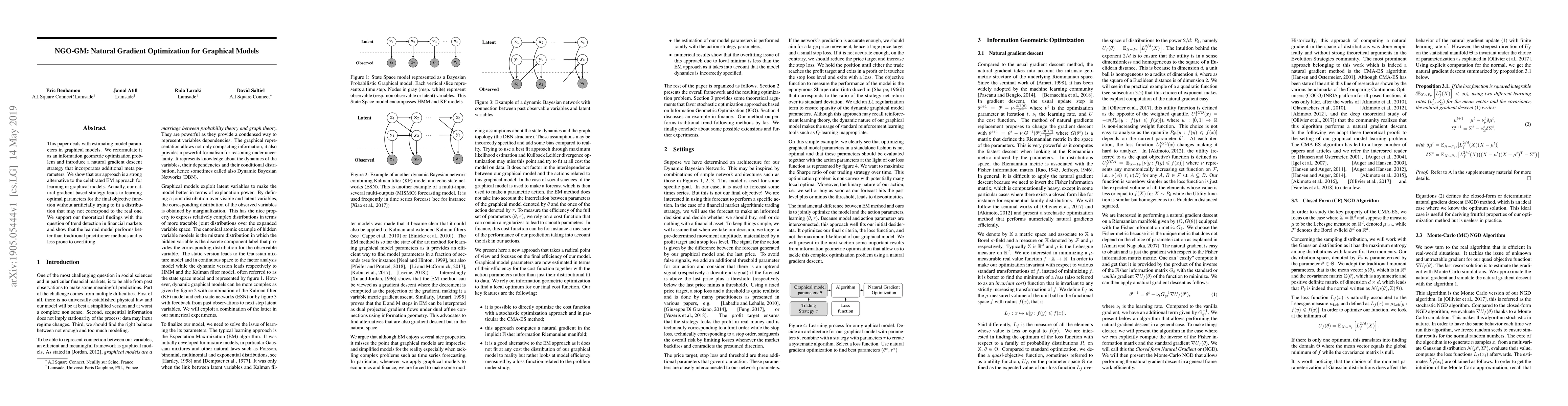

This paper deals with estimating model parameters in graphical models. We reformulate it as an information geometric optimization problem and introduce a natural gradient descent strategy that incor...

In this paper, we present three remarkable properties of the normal distribution: first that if two independent variables's sum is normally distributed, then each random variable follows a normal di...

Sharpe ratio is widely used in asset management to compare and benchmark funds and asset managers. It computes the ratio of the excess return over the strategy standard deviation. However, the eleme...

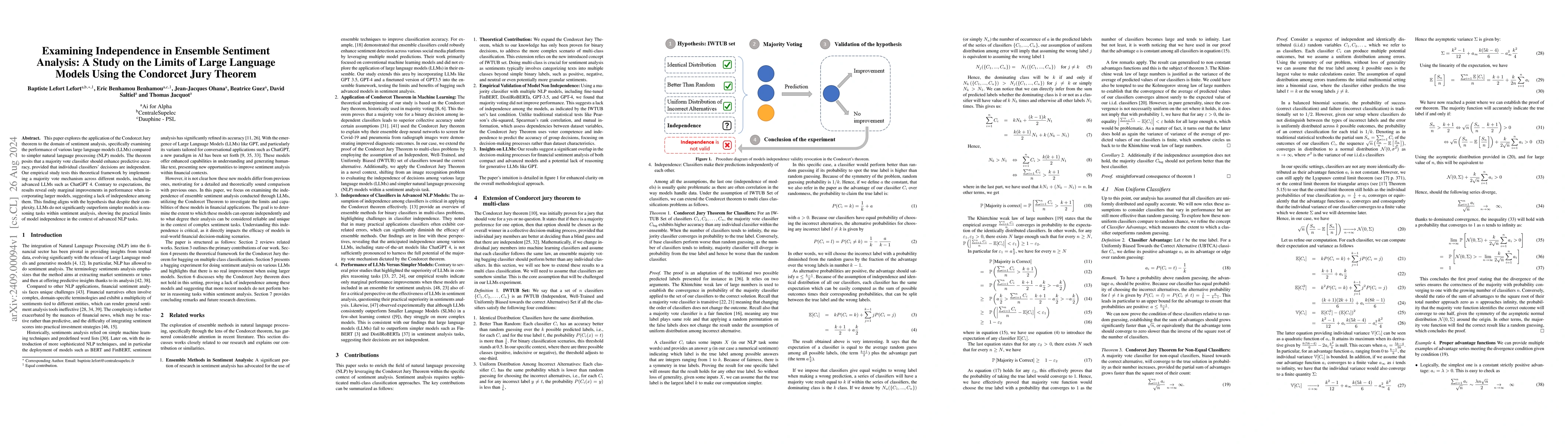

This paper explores the application of the Condorcet Jury theorem to the domain of sentiment analysis, specifically examining the performance of various large language models (LLMs) compared to simple...

In this paper, we demonstrate that non-generative, small-sized models such as FinBERT and FinDRoBERTa, when fine-tuned, can outperform GPT-3.5 and GPT-4 models in zero-shot learning settings in sentim...

Commodity Trading Advisors (CTAs) have historically relied on trend-following rules that operate on vastly different horizons from long-term breakouts that capture major directional moves to short-ter...

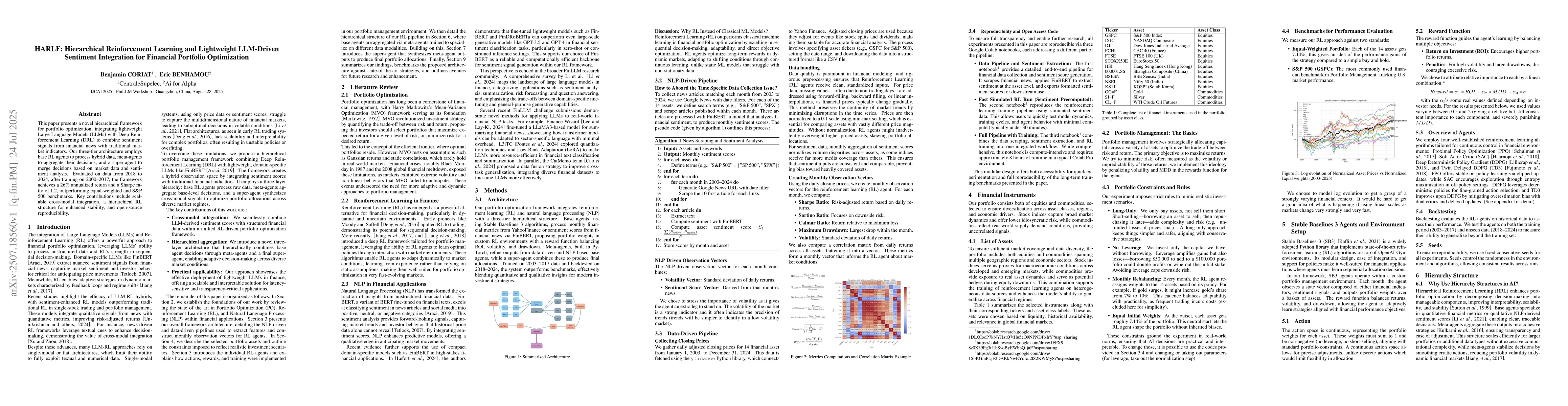

This paper presents a novel hierarchical framework for portfolio optimization, integrating lightweight Large Language Models (LLMs) with Deep Reinforcement Learning (DRL) to combine sentiment signals ...

This paper presents a novel hierarchical framework for portfolio optimization, integrating lightweight Large Language Models (LLMs) with Deep Reinforcement Learning (DRL) to combine sentiment signals ...

Recent work has emphasized the diversification benefits of combining trend signals across multiple horizons, with the medium-term window-typically six months to one year-long viewed as the "sweet spot...

Trend-following strategies underpin many systematic trading approaches yet struggle under nonstationary and nonlinear market regimes. We propose an LSTM-based framework to forecast next-day trend diff...