Re-evaluating Short- and Long-Term Trend Factors in CTA Replication: A Bayesian Graphical Approach

Publication

Metrics

Paper Preview

Abstract

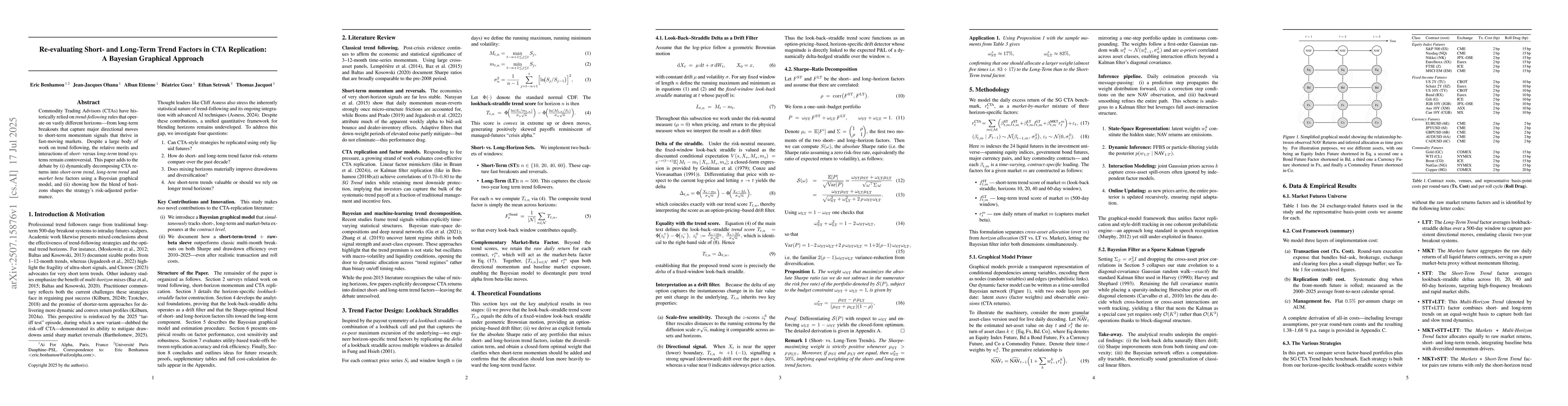

Commodity Trading Advisors (CTAs) have historically relied on trend-following rules that operate on vastly different horizons from long-term breakouts that capture major directional moves to short-term momentum signals that thrive in fast-moving markets. Despite a large body of work on trend following, the relative merits and interactions of short-versus long-term trend systems remain controversial. This paper adds to the debate by (i) dynamically decomposing CTA returns into short-term trend, long-term trend and market beta factors using a Bayesian graphical model, and (ii) showing how the blend of horizons shapes the strategy's risk-adjusted performance.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0