FinMem: A Performance-Enhanced LLM Trading Agent with Layered Memory and Character Design

Publication

Metrics

AI Quick Summary

FinMem is an advanced LLM-based trading agent designed for financial decision-making, featuring a layered memory system and customizable character design. It outperforms other algorithmic agents in stock trading by leveraging its interpretable memory module and adaptive cognitive span to enhance trading outcomes.

Paper Preview

Abstract

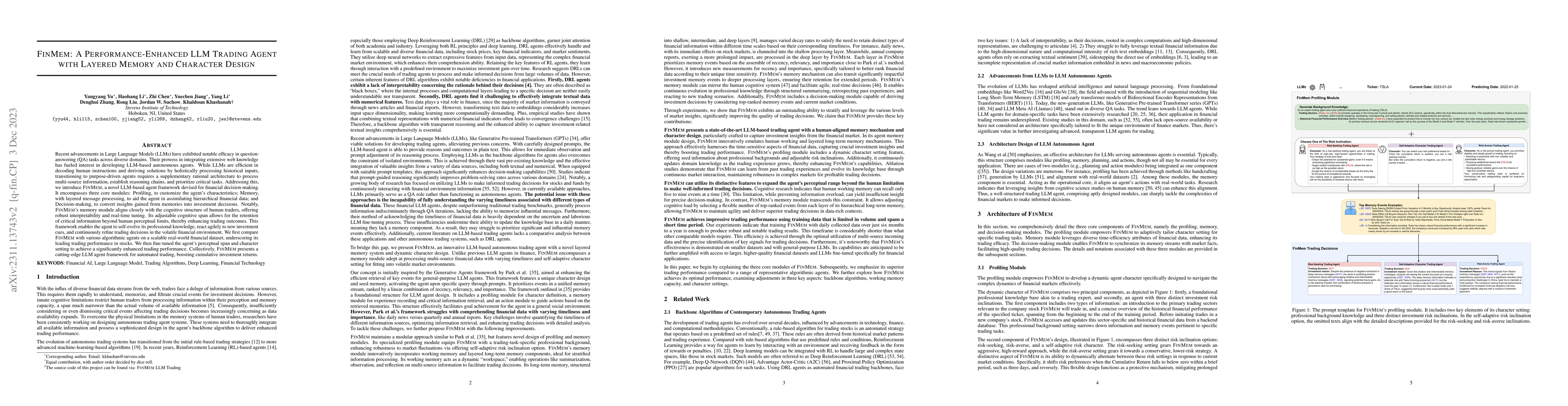

Recent advancements in Large Language Models (LLMs) have exhibited notable efficacy in question-answering (QA) tasks across diverse domains. Their prowess in integrating extensive web knowledge has fueled interest in developing LLM-based autonomous agents. While LLMs are efficient in decoding human instructions and deriving solutions by holistically processing historical inputs, transitioning to purpose-driven agents requires a supplementary rational architecture to process multi-source information, establish reasoning chains, and prioritize critical tasks. Addressing this, we introduce \textsc{FinMem}, a novel LLM-based agent framework devised for financial decision-making. It encompasses three core modules: Profiling, to customize the agent's characteristics; Memory, with layered message processing, to aid the agent in assimilating hierarchical financial data; and Decision-making, to convert insights gained from memories into investment decisions. Notably, \textsc{FinMem}'s memory module aligns closely with the cognitive structure of human traders, offering robust interpretability and real-time tuning. Its adjustable cognitive span allows for the retention of critical information beyond human perceptual limits, thereby enhancing trading outcomes. This framework enables the agent to self-evolve its professional knowledge, react agilely to new investment cues, and continuously refine trading decisions in the volatile financial environment. We first compare \textsc{FinMem} with various algorithmic agents on a scalable real-world financial dataset, underscoring its leading trading performance in stocks. We then fine-tuned the agent's perceptual span and character setting to achieve a significantly enhanced trading performance. Collectively, \textsc{FinMem} presents a cutting-edge LLM agent framework for automated trading, boosting cumulative investment returns.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0