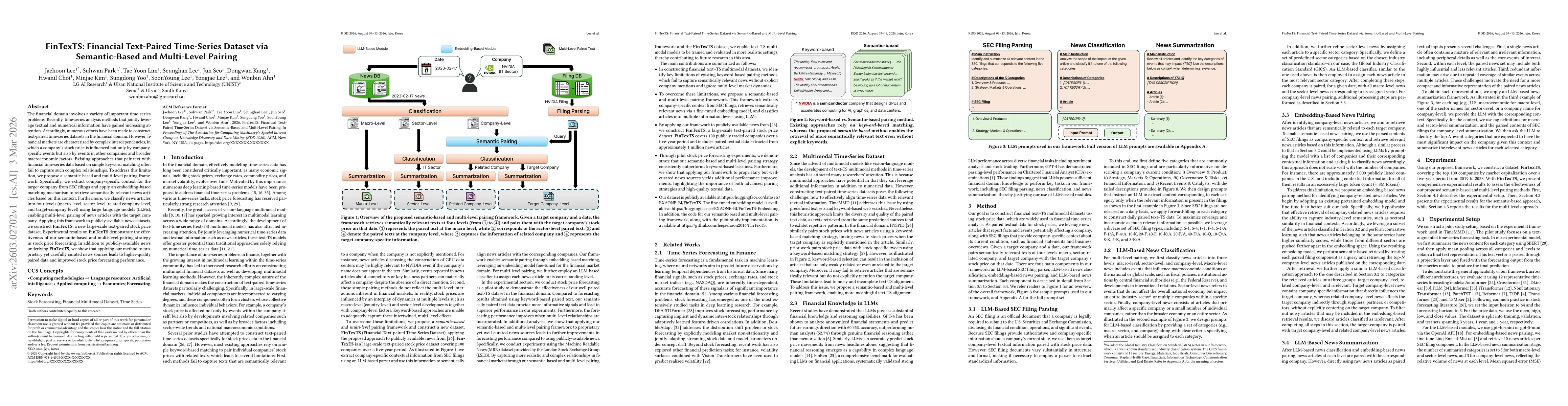

The financial domain involves a variety of important time-series problems. Recently, time-series analysis methods that jointly leverage textual and numerical information have gained increasing attention. Accordingly, numerous efforts have been made to construct text-paired time-series datasets in the financial domain. However, financial markets are characterized by complex interdependencies, in which a company's stock price is influenced not only by company-specific events but also by events in other companies and broader macroeconomic factors. Existing approaches that pair text with financial time-series data based on simple keyword matching often fail to capture such complex relationships. To address this limitation, we propose a semantic-based and multi-level pairing framework. Specifically, we extract company-specific context for the target company from SEC filings and apply an embedding-based matching mechanism to retrieve semantically relevant news articles based on this context. Furthermore, we classify news articles into four levels (macro-level, sector-level, related company-level, and target-company level) using large language models (LLMs), enabling multi-level pairing of news articles with the target company. Applying this framework to publicly-available news datasets, we construct \textbf{FinTexTS}, a new large-scale text-paired stock price dataset. Experimental results on \textbf{FinTexTS} demonstrate the effectiveness of our semantic-based and multi-level pairing strategy in stock price forecasting. In addition to publicly-available news underlying \textbf{FinTexTS}, we show that applying our method to proprietary yet carefully curated news sources leads to higher-quality paired data and improved stock price forecasting performance.

Discussion 0