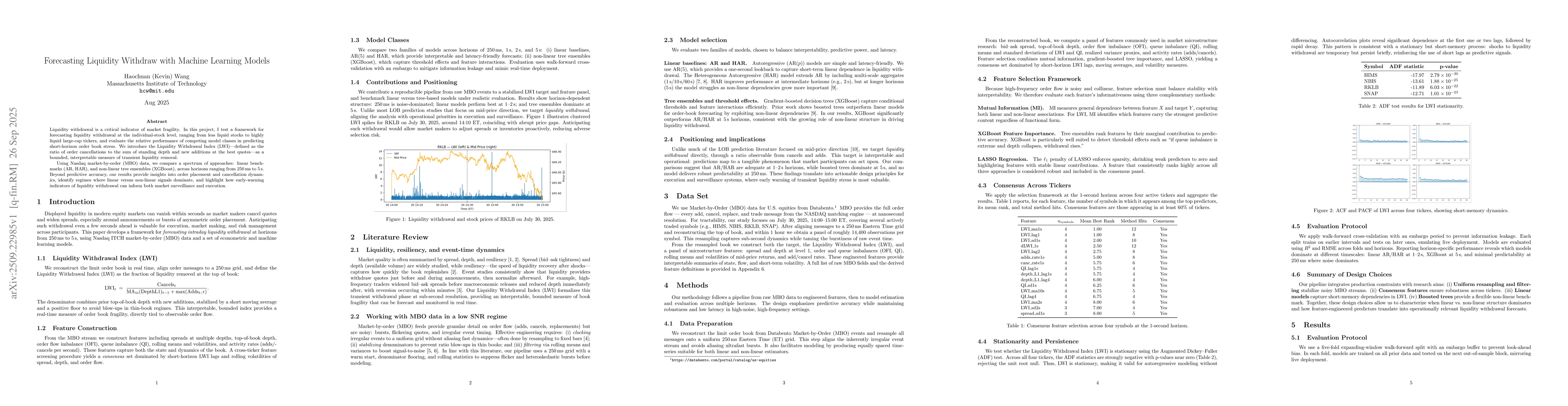

Liquidity withdrawal is a critical indicator of market fragility. In this

project, I test a framework for forecasting liquidity withdrawal at the

individual-stock level, ranging from less liquid stocks to highly liquid

large-cap tickers, and evaluate the relative performance of competing model

classes in predicting short-horizon order book stress. We introduce the

Liquidity Withdrawal Index (LWI) -- defined as the ratio of order cancellations

to the sum of standing depth and new additions at the best quotes -- as a

bounded, interpretable measure of transient liquidity removal.

Using Nasdaq market-by-order (MBO) data, we compare a spectrum of approaches:

linear benchmarks (AR, HAR), and non-linear tree ensembles (XGBoost), across

horizons ranging from 250\,ms to 5\,s. Beyond predictive accuracy, our results

provide insights into order placement and cancellation dynamics, identify

regimes where linear versus non-linear signals dominate, and highlight how

early-warning indicators of liquidity withdrawal can inform both market

surveillance and execution.

Discussion 0