Directional forecasting in financial markets requires both accuracy and

interpretability. Before the advent of deep learning, interpretable approaches

based on human-defined patterns were prevalent, but their structural vagueness

and scale ambiguity hindered generalization. In contrast, deep learning models

can effectively capture complex dynamics, yet often offer limited transparency.

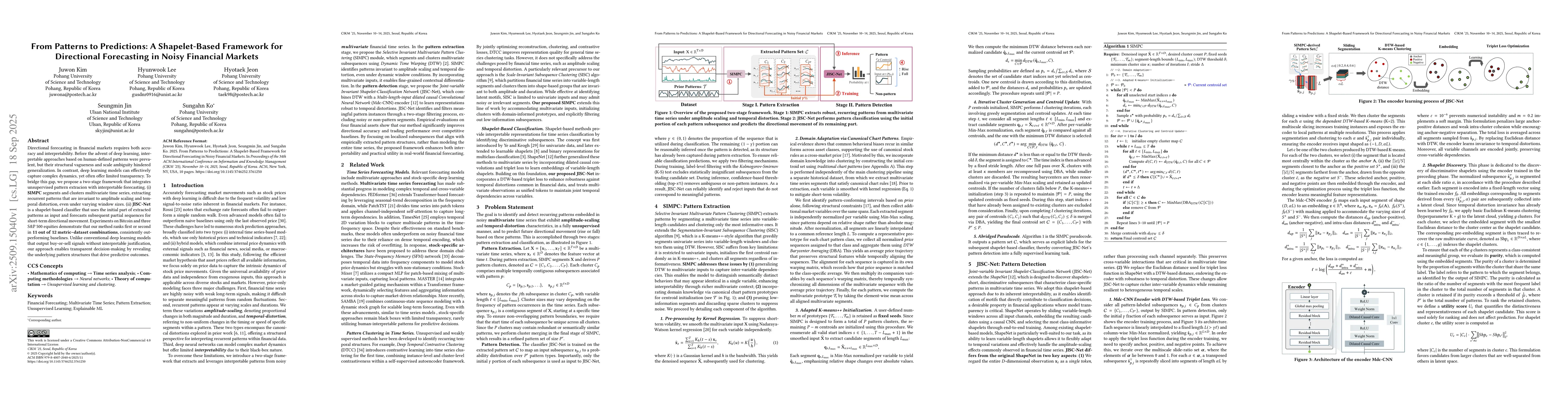

To bridge this gap, we propose a two-stage framework that integrates

unsupervised pattern extracion with interpretable forecasting. (i) SIMPC

segments and clusters multivariate time series, extracting recurrent patterns

that are invariant to amplitude scaling and temporal distortion, even under

varying window sizes. (ii) JISC-Net is a shapelet-based classifier that uses

the initial part of extracted patterns as input and forecasts subsequent

partial sequences for short-term directional movement. Experiments on Bitcoin

and three S&P 500 equities demonstrate that our method ranks first or second in

11 out of 12 metric--dataset combinations, consistently outperforming

baselines. Unlike conventional deep learning models that output buy-or-sell

signals without interpretable justification, our approach enables transparent

decision-making by revealing the underlying pattern structures that drive

predictive outcomes.

Discussion 0