01

MethodologyHow they did it

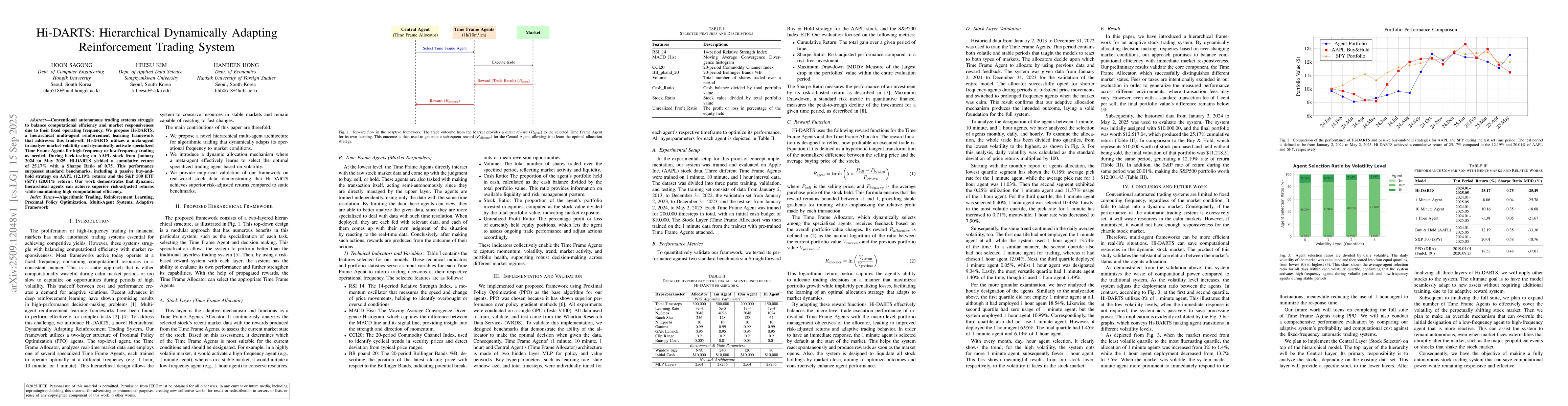

Hi-DARTS employs a hierarchical multi-agent reinforcement learning framework with a meta-agent (CentralAgent) that dynamically selects specialized TimeFrameAgents (1m/10m/1h) based on market volatility. The system uses Proximal Policy Optimization (PPO) for training and evaluates performance using cumulative return, Sharpe Ratio, and Maximum Drawdown metrics.

Discussion 0