Summary

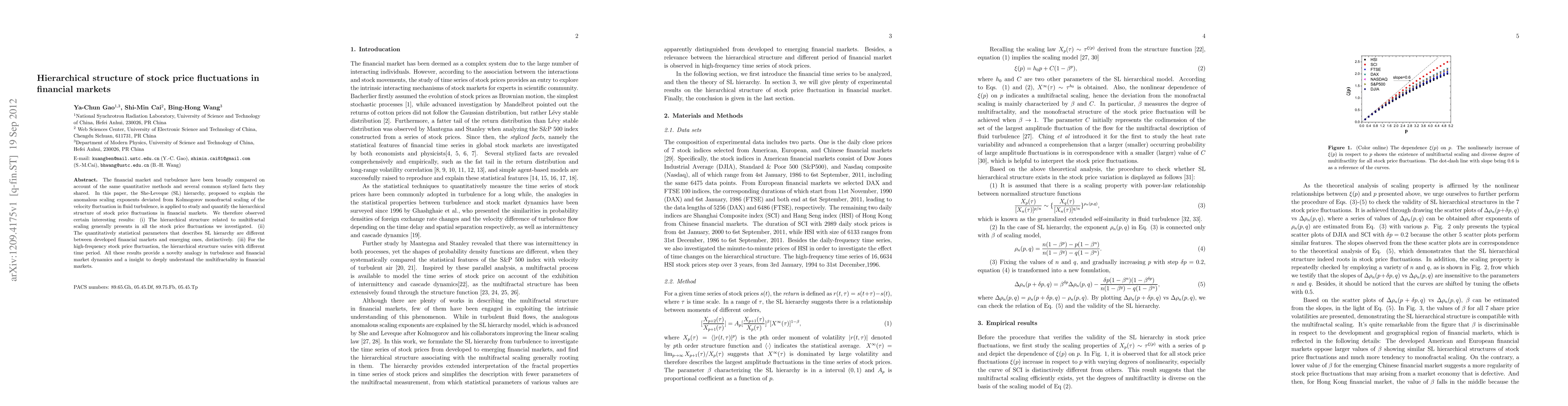

The financial market and turbulence have been broadly compared on account of the same quantitative methods and several common stylized facts they shared. In this paper, the She-Leveque (SL) hierarchy, proposed to explain the anomalous scaling exponents deviated from Kolmogorov monofractal scaling of the velocity fluctuation in fluid turbulence, is applied to study and quantify the hierarchical structure of stock price fluctuations in financial markets. We therefore observed certain interesting results: (i) The hierarchical structure related to multifractal scaling generally presents in all the stock price fluctuations we investigated. (ii) The quantitatively statistical parameters that describes SL hierarchy are different between developed financial markets and emerging ones, distinctively. (iii) For the high-frequency stock price fluctuation, the hierarchical structure varies with different time period. All these results provide a novelty analogy in turbulence and financial market dynamics and a insight to deeply understand the multifractality in financial markets.

AI Key Findings

Generated Sep 02, 2025

Methodology

The research applies the She-Leveque (SL) hierarchy to study the hierarchical structure of stock price fluctuations in financial markets, using scaling properties and extended self-similarity.

Key Results

- The hierarchical structure related to multifractal scaling is observed in all investigated stock price fluctuations.

- Quantitatively statistical parameters describing the SL hierarchy differ between developed and emerging financial markets.

- For high-frequency stock price fluctuations, the hierarchical structure varies with different time periods.

Significance

This research provides a novel analogy between turbulence and financial market dynamics, offering insights into multifractality in financial markets.

Technical Contribution

The paper introduces the application of the She-Leveque (SL) hierarchy to financial market dynamics, providing a quantitative analysis of stock price fluctuations.

Novelty

This work is novel in applying turbulence theory to financial markets, revealing differences between developed and emerging markets, and highlighting the time-dependent nature of high-frequency fluctuations.

Limitations

- The study is limited to specific financial markets and does not cover all global markets.

- High-frequency fluctuation analysis is dependent on the chosen time period.

Future Work

- Investigate the SL hierarchy in a broader range of financial markets.

- Explore the impact of various economic and political factors on the SL hierarchy.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersMamba Meets Financial Markets: A Graph-Mamba Approach for Stock Price Prediction

Xiaohong Chen, Ehsan Hoseinzade, Ali Mehrabian et al.

| Title | Authors | Year | Actions |

|---|

Comments (0)