Publication

Metrics

AI Quick Summary

Summary: This paper reviews kinetic models using partial differential equations to analyze stock price dynamics in financial markets, highlighting the significance of behavioral factors and agent heterogeneity in shaping market booms, crashes, and the emergence of power laws in price distributions.

Paper Preview

Abstract

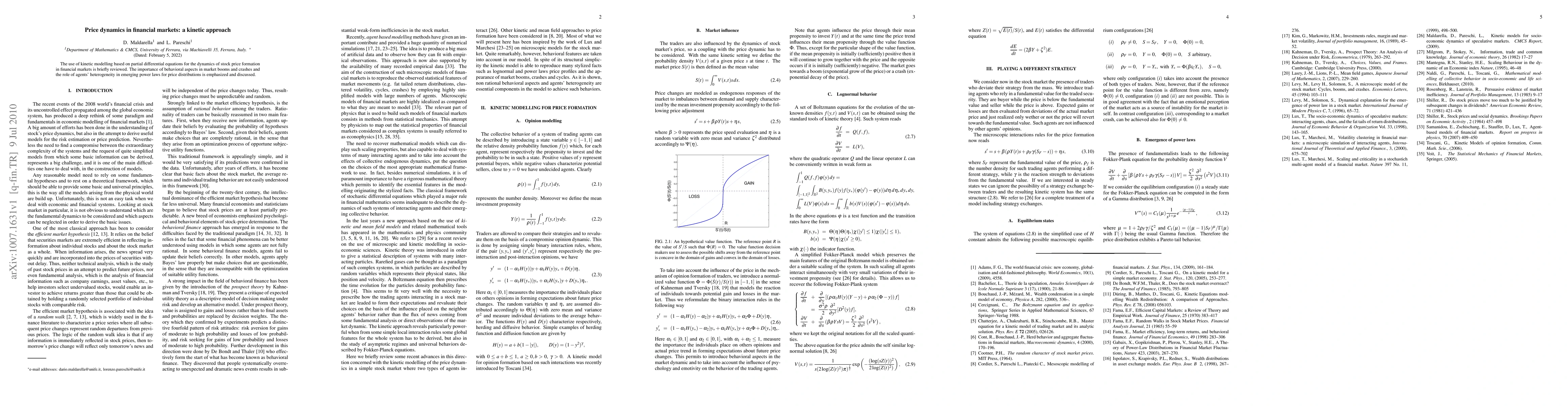

The use of kinetic modelling based on partial differential equations for the dynamics of stock price formation in financial markets is briefly reviewed. The importance of behavioral aspects in market booms and crashes and the role of agents' heterogeneity in emerging power laws for price distributions is emphasized and discussed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0