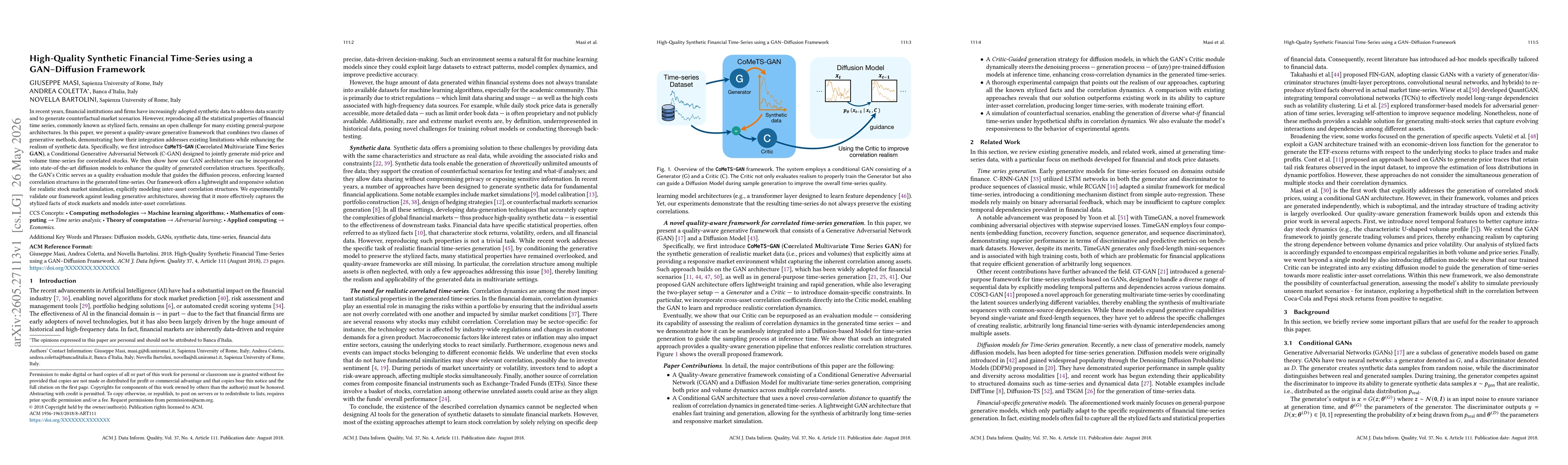

In recent years, financial institutions and firms have increasingly adopted synthetic data to address data scarcity and to generate counterfactual market scenarios. However, reproducing all the statistical properties of financial time series, commonly known as stylized facts, remains an open challenge for many existing general-purpose architectures. In this paper, we present a quality-aware generative framework that combines two classes of generative methods, demonstrating how their integration addresses existing limitations while enhancing the realism of synthetic data. Specifically, we first introduce CoMeTS-GAN (Correlated Multivariate Time Series GAN), a Conditional Generative Adversarial Network (C-GAN) designed to jointly generate mid-price and volume time-series for correlated stocks. We then show how our GAN architecture can be incorporated into state-of-the-art diffusion models to enhance the quality of generated correlation structures. Specifically, the GAN's Critic serves as a quality evaluation module that guides the diffusion process, enforcing learned correlation structures in the generated time-series. Our framework offers a lightweight and responsive solution for realistic stock market simulation, explicitly modeling inter-asset correlation structures. We experimentally validate our framework against leading generative architectures, showing that it more effectively captures the stylized facts of stock markets and models inter-asset correlations.

Discussion 0