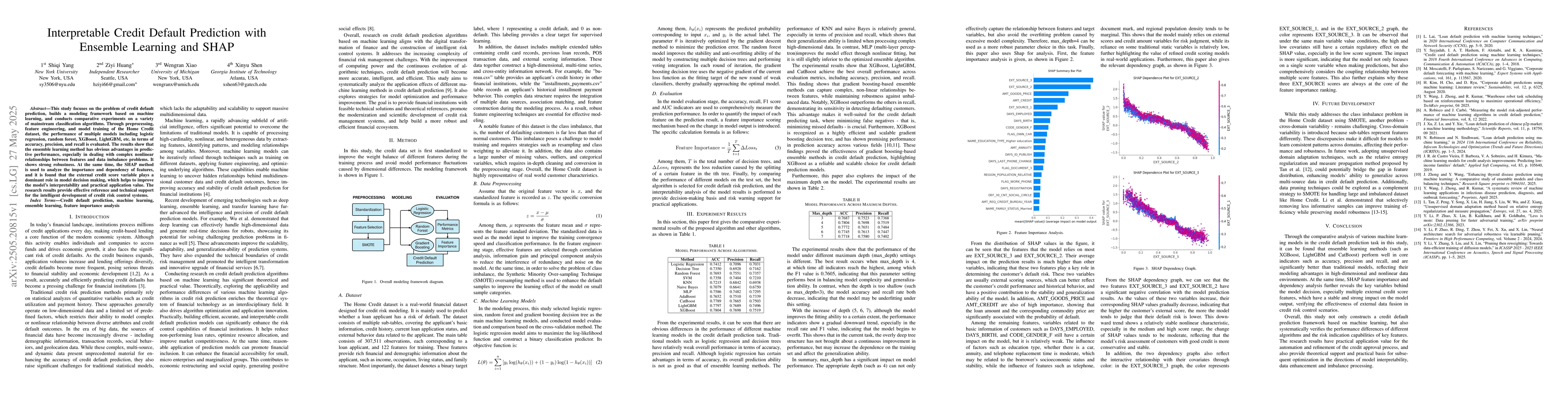

This study focuses on the problem of credit default prediction, builds a

modeling framework based on machine learning, and conducts comparative

experiments on a variety of mainstream classification algorithms. Through

preprocessing, feature engineering, and model training of the Home Credit

dataset, the performance of multiple models including logistic regression,

random forest, XGBoost, LightGBM, etc. in terms of accuracy, precision, and

recall is evaluated. The results show that the ensemble learning method has

obvious advantages in predictive performance, especially in dealing with

complex nonlinear relationships between features and data imbalance problems.

It shows strong robustness. At the same time, the SHAP method is used to

analyze the importance and dependency of features, and it is found that the

external credit score variable plays a dominant role in model decision making,

which helps to improve the model's interpretability and practical application

value. The research results provide effective reference and technical support

for the intelligent development of credit risk control systems.

Discussion 0