KACDP: A Highly Interpretable Credit Default Prediction Model

Publication

Metrics

AI Quick Summary

This paper proposes the KACDP model using Kolmogorov-Arnold Networks (KANs) for highly interpretable credit default prediction, showing superior performance over existing methods and offering transparent insights through feature attribution and visualization.

Paper Preview

Abstract

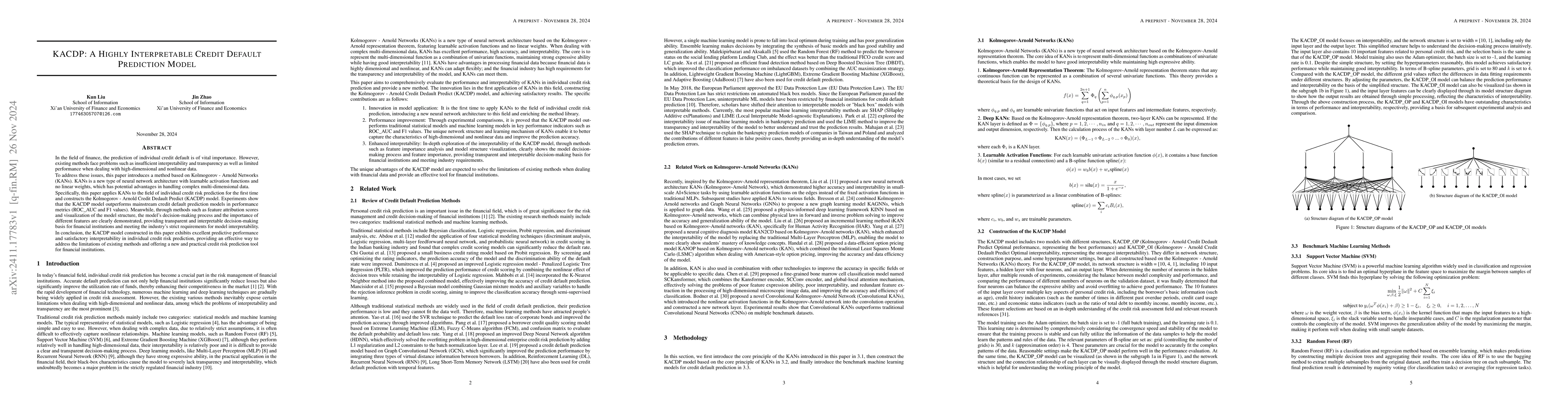

In the field of finance, the prediction of individual credit default is of vital importance. However, existing methods face problems such as insufficient interpretability and transparency as well as limited performance when dealing with high-dimensional and nonlinear data. To address these issues, this paper introduces a method based on Kolmogorov-Arnold Networks (KANs). KANs is a new type of neural network architecture with learnable activation functions and no linear weights, which has potential advantages in handling complex multi-dimensional data. Specifically, this paper applies KANs to the field of individual credit risk prediction for the first time and constructs the Kolmogorov-Arnold Credit Default Predict (KACDP) model. Experiments show that the KACDP model outperforms mainstream credit default prediction models in performance metrics (ROC_AUC and F1 values). Meanwhile, through methods such as feature attribution scores and visualization of the model structure, the model's decision-making process and the importance of different features are clearly demonstrated, providing transparent and interpretable decision-making basis for financial institutions and meeting the industry's strict requirements for model interpretability. In conclusion, the KACDP model constructed in this paper exhibits excellent predictive performance and satisfactory interpretability in individual credit risk prediction, providing an effective way to address the limitations of existing methods and offering a new and practical credit risk prediction tool for financial institutions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0