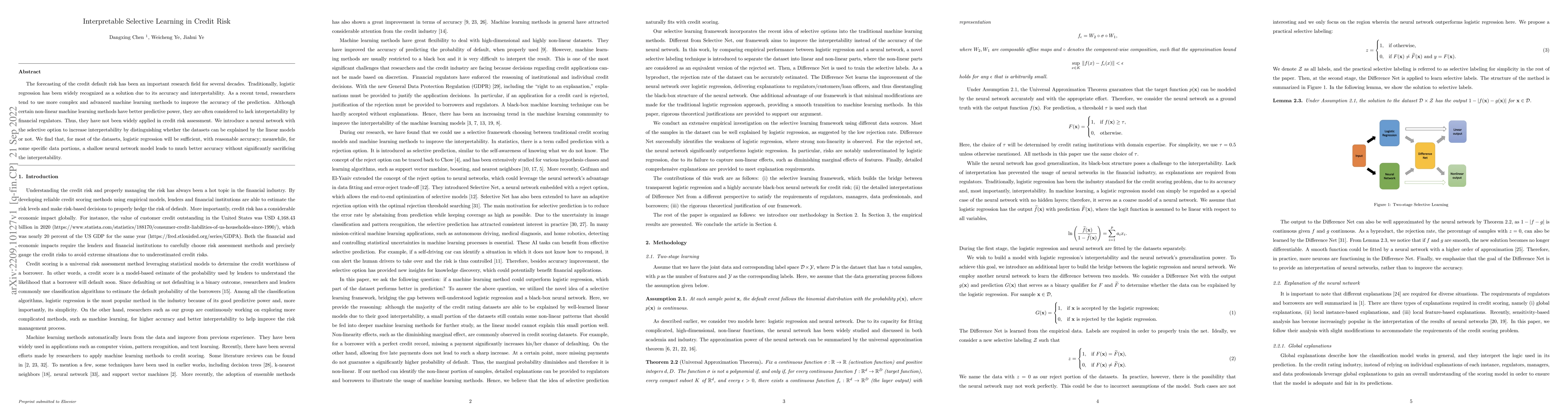

Interpretable Selective Learning in Credit Risk

Publication

Metrics

AI Quick Summary

This paper proposes a selective learning approach combining logistic regression and a shallow neural network to improve credit default risk prediction. It aims to maintain interpretability preferred by regulators, finding that while logistic regression suffices for most data, neural networks enhance accuracy for specific subsets without significant loss of clarity.

Paper Preview

Abstract

The forecasting of the credit default risk has been an important research field for several decades. Traditionally, logistic regression has been widely recognized as a solution due to its accuracy and interpretability. As a recent trend, researchers tend to use more complex and advanced machine learning methods to improve the accuracy of the prediction. Although certain non-linear machine learning methods have better predictive power, they are often considered to lack interpretability by financial regulators. Thus, they have not been widely applied in credit risk assessment. We introduce a neural network with the selective option to increase interpretability by distinguishing whether the datasets can be explained by the linear models or not. We find that, for most of the datasets, logistic regression will be sufficient, with reasonable accuracy; meanwhile, for some specific data portions, a shallow neural network model leads to much better accuracy without significantly sacrificing the interpretability.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0