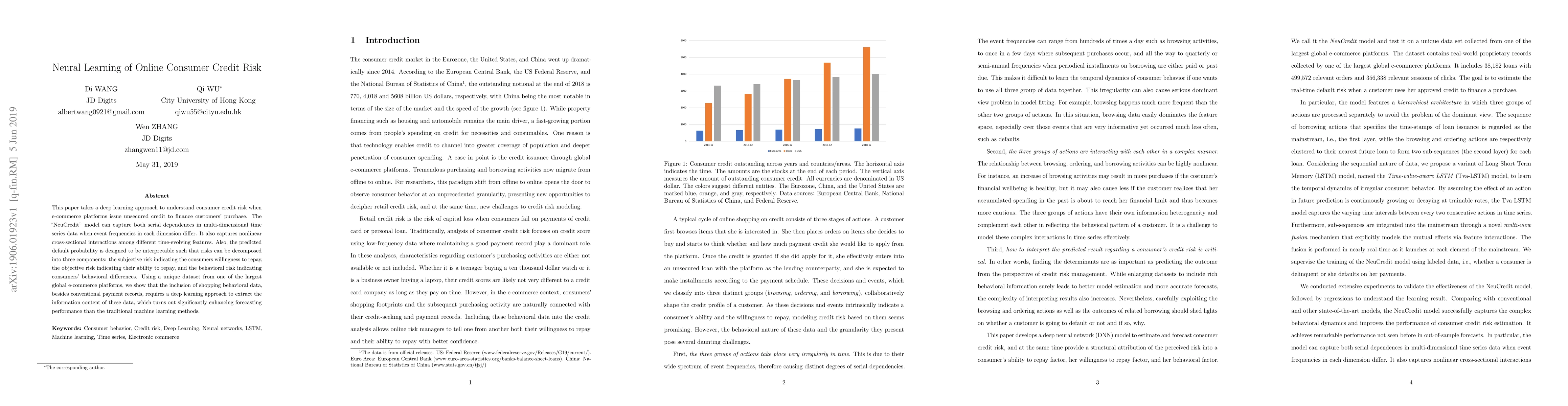

Publication

Metrics

AI Quick Summary

This paper introduces the "NeuCredit" deep learning model to assess consumer credit risk in e-commerce, capturing complex temporal dependencies and nonlinear interactions. It enhances forecasting performance by incorporating shopping behavioral data, decomposing default probability into subjective, objective, and behavioral risk components.

Paper Preview

Abstract

This paper takes a deep learning approach to understand consumer credit risk when e-commerce platforms issue unsecured credit to finance customers' purchase. The "NeuCredit" model can capture both serial dependences in multi-dimensional time series data when event frequencies in each dimension differ. It also captures nonlinear cross-sectional interactions among different time-evolving features. Also, the predicted default probability is designed to be interpretable such that risks can be decomposed into three components: the subjective risk indicating the consumers' willingness to repay, the objective risk indicating their ability to repay, and the behavioral risk indicating consumers' behavioral differences. Using a unique dataset from one of the largest global e-commerce platforms, we show that the inclusion of shopping behavioral data, besides conventional payment records, requires a deep learning approach to extract the information content of these data, which turns out significantly enhancing forecasting performance than the traditional machine learning methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0