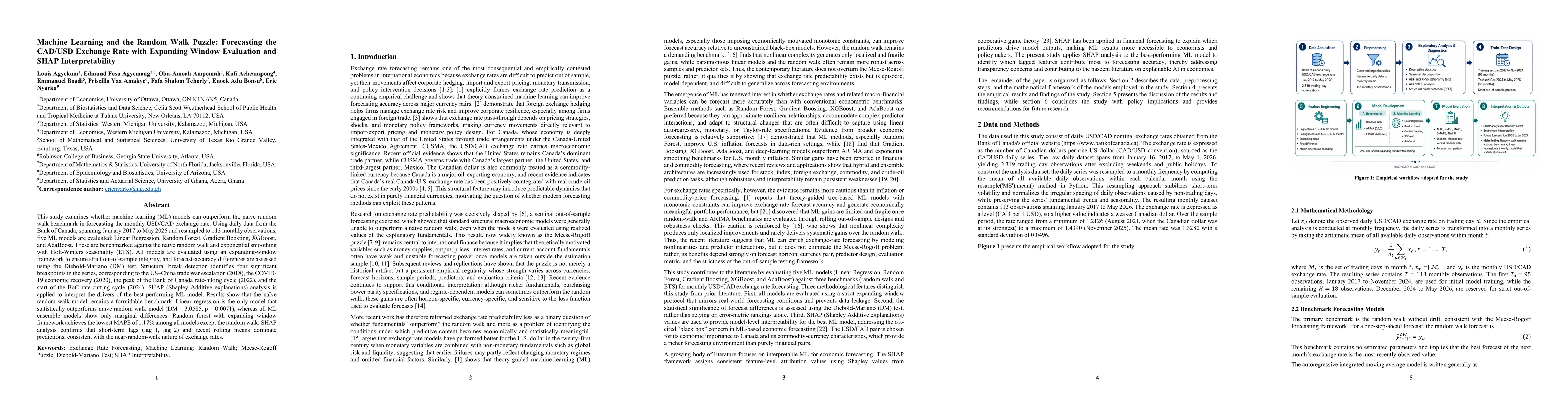

This study examines whether machine learning (ML) models can outperform the naive random walk benchmark in forecasting the monthly USD/CAD exchange rate. Using daily data from the Bank of Canada spanning January 2017 to May 2026, resampled into 113 monthly observations, five ML models are evaluated: linear regression, random forest, gradient boosting, XGBoost, and AdaBoost. These models are benchmarked against the naive random walk model and exponential smoothing with Holt-Winters seasonality (ETS). All models are evaluated using an expanding-window framework to maintain strict out-of-sample integrity, and forecast-accuracy differences are assessed using the Diebold-Mariano (DM) test. Structural break detection identifies four significant breakpoints in the series, corresponding to the escalation of the US-China trade war in 2018, the COVID-19 economic recovery in 2020, the peak of the Bank of Canada rate-hiking cycle in 2022, and the start of the Bank of Canada rate-cutting cycle in 2024. SHAP, or Shapley Additive Explanations, analysis is applied to interpret the drivers of the best-performing ML model. The results show that the naive random walk model remains a formidable benchmark. Linear regression is the only model that statistically outperforms the naive random walk model, with a DM statistic of 3.0585 and a p value of 0.0071, whereas the ML ensemble models show only marginal differences. Random Forest with an expanding-window framework achieves the lowest MAPE of 1.17 percent among all models except the random walk. SHAP analysis confirms that short-term lags, particularly lag1 and lag2, and recent rolling means dominate predictions, consistent with the near-random-walk behavior of exchange rates.

Discussion 0