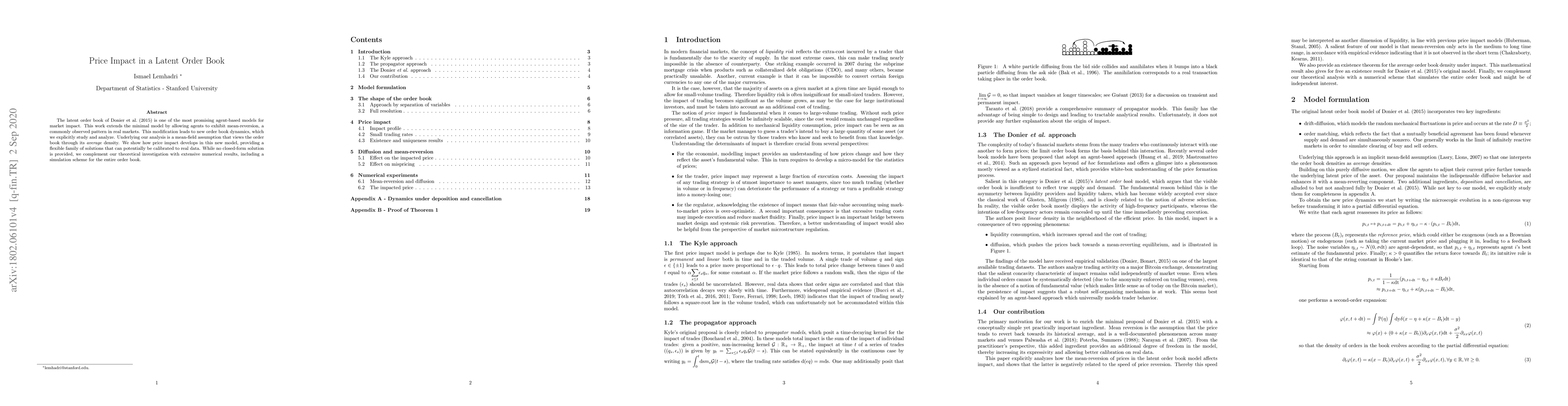

Market Impact in a Latent Order Book

Publication

Metrics

AI Quick Summary

This paper extends a minimal agent-based model of a latent order book to include mean-reversion, altering order book dynamics and allowing for more realistic market behavior. Theoretical analysis and numerical simulations are used to explore how price impact develops under these new dynamics, offering a flexible solution family for better calibration to real market data.

Paper Preview

Abstract

The latent order book of \cite{donier2015fully} is one of the most promising agent-based models for market impact. This work extends the minimal model by allowing agents to exhibit mean-reversion, a commonly observed pattern in real markets. This modification leads to new order book dynamics, which we explicitly study and analyze. Underlying our analysis is a mean-field assumption that views the order book through its \textit{average} density. We show how price impact develops in this new model, providing a flexible family of solutions that can potentially improve calibration to real data. While no closed-form solution is provided, we complement our theoretical investigation with extensive numerical results, including a simulation scheme for the entire order book.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0