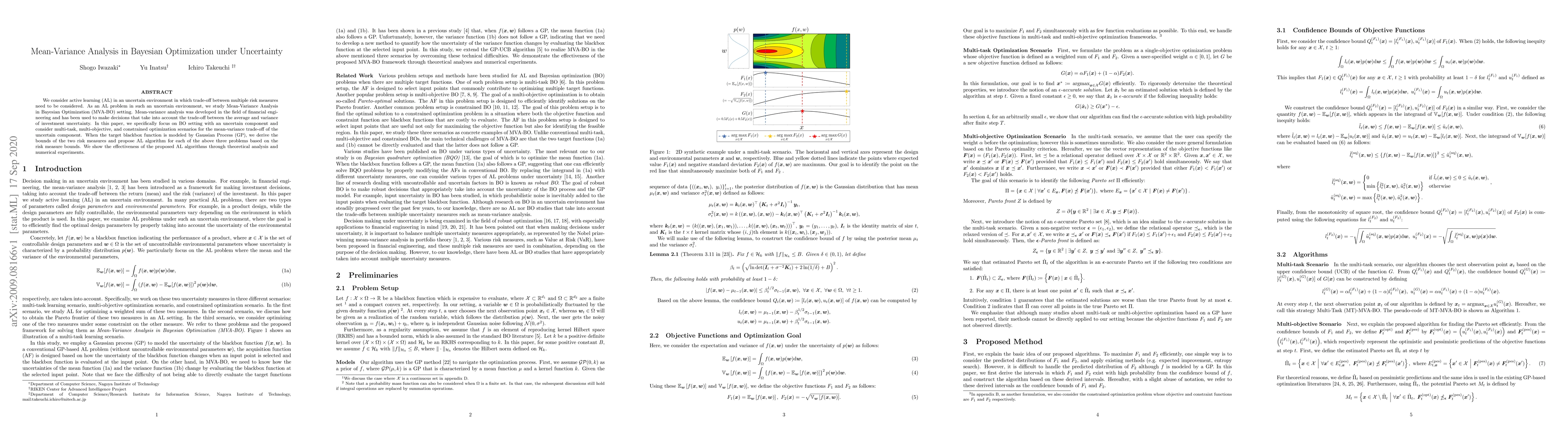

Mean-Variance Analysis in Bayesian Optimization under Uncertainty

Publication

Metrics

AI Quick Summary

This paper explores active learning in uncertain environments using Mean-Variance Analysis in Bayesian Optimization (MVA-BO) to balance multiple risk measures. It proposes algorithms for multi-task, multi-objective, and constrained optimization scenarios, deriving bounds for risk measures and demonstrating their effectiveness via theoretical and empirical analysis.

Paper Preview

Abstract

We consider active learning (AL) in an uncertain environment in which trade-off between multiple risk measures need to be considered. As an AL problem in such an uncertain environment, we study Mean-Variance Analysis in Bayesian Optimization (MVA-BO) setting. Mean-variance analysis was developed in the field of financial engineering and has been used to make decisions that take into account the trade-off between the average and variance of investment uncertainty. In this paper, we specifically focus on BO setting with an uncertain component and consider multi-task, multi-objective, and constrained optimization scenarios for the mean-variance trade-off of the uncertain component. When the target blackbox function is modeled by Gaussian Process (GP), we derive the bounds of the two risk measures and propose AL algorithm for each of the above three problems based on the risk measure bounds. We show the effectiveness of the proposed AL algorithms through theoretical analysis and numerical experiments.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0