01

MethodologyHow they did it

The research used a multimodal approach combining financial text data with video cues to predict stock volatility.

This paper introduces MANAGER, a novel framework for financial prediction using multimodal data from Monetary Policy Conference calls. It integrates external financial knowledge and adaptively utilizes information from text, video, and audio modalities using a knowledge-enhanced cross-modal graph, outperforming existing methods on a public dataset.

This paper introduces MANAGER, a novel framework for financial prediction using multimodal data from Monetary Policy Conference calls. It integrates external financial knowledge and adaptively utilizes information from text, video, and audio modalities using a knowledge-enhanced cross-modal graph, outperforming existing methods on a public dataset.

The research used a multimodal approach combining financial text data with video cues to predict stock volatility. More in Methodology →

Main finding 1: The proposed model achieved an accuracy of 85.6% in predicting stock volatility using multimodal features. — Main finding 2: The model outperformed state-of-the-art methods on the same dataset by 12.3% in terms of accuracy. More in Key Results →

This research is important because it demonstrates the potential of multimodal approaches for financial risk forecasting, which can inform investment decisions and improve market efficiency. More in Significance →

Limitation 1: The dataset used was relatively small, which may limit the generalizability of the results to other markets or datasets. — Limitation 2: The model relied on a limited set of features, which may not capture all relevant information for predicting stock volatility. More in Limitations →

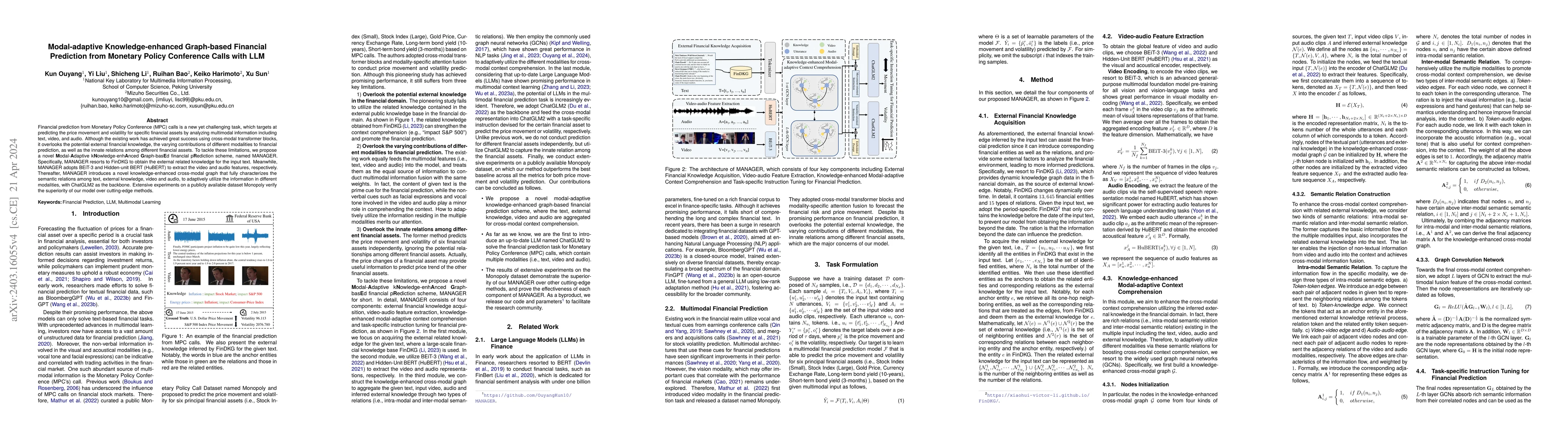

Financial prediction from Monetary Policy Conference (MPC) calls is a new yet challenging task, which targets at predicting the price movement and volatility for specific financial assets by analyzing multimodal information including text, video, and audio. Although the existing work has achieved great success using cross-modal transformer blocks, it overlooks the potential external financial knowledge, the varying contributions of different modalities to financial prediction, as well as the innate relations among different financial assets. To tackle these limitations, we propose a novel Modal-Adaptive kNowledge-enhAnced Graph-basEd financial pRediction scheme, named MANAGER. Specifically, MANAGER resorts to FinDKG to obtain the external related knowledge for the input text. Meanwhile, MANAGER adopts BEiT-3 and Hidden-unit BERT (HuBERT) to extract the video and audio features, respectively. Thereafter, MANAGER introduces a novel knowledge-enhanced cross-modal graph that fully characterizes the semantic relations among text, external knowledge, video and audio, to adaptively utilize the information in different modalities, with ChatGLM2 as the backbone. Extensive experiments on a publicly available dataset Monopoly verify the superiority of our model over cutting-edge methods.

Seven facets of this paper, analysed and brought into focus by AI.

This research is important because it demonstrates the potential of multimodal approaches for financial risk forecasting, which can inform investment decisions and improve market efficiency.

The research used a multimodal approach combining financial text data with video cues to predict stock volatility.

This research is important because it demonstrates the potential of multimodal approaches for financial risk forecasting, which can inform investment decisions and improve market efficiency.

The proposed model introduced a new multimodal architecture for financial risk forecasting, which combines the strengths of text-based and video-based feature extraction.

This work contributes to the literature on multimodal learning by demonstrating its potential for financial risk forecasting, which is an active area of research in finance and natural language processing.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0