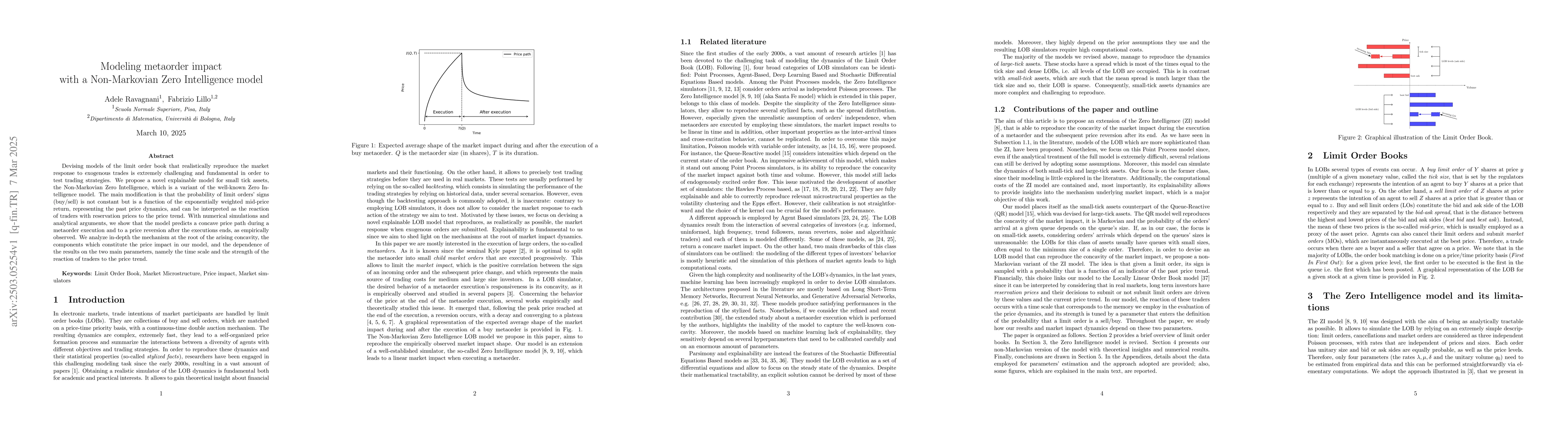

Devising models of the limit order book that realistically reproduce the

market response to exogenous trades is extremely challenging and fundamental in

order to test trading strategies. We propose a novel explainable model for

small tick assets, the Non-Markovian Zero Intelligence, which is a variant of

the well-known Zero Intelligence model. The main modification is that the

probability of limit orders' signs (buy/sell) is not constant but is a function

of the exponentially weighted mid-price return, representing the past price

dynamics, and can be interpreted as the reaction of traders with reservation

prices to the price trend. With numerical simulations and analytical arguments,

we show that the model predicts a concave price path during a metaorder

execution and to a price reversion after the executions ends, as empirically

observed. We analyze in-depth the mechanism at the root of the arising

concavity, the components which constitute the price impact in our model, and

the dependence of the results on the two main parameters, namely the time scale

and the strength of the reaction of traders to the price trend.

Discussion 0