Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate the trading behavior of a large set of single investors trading the highly liquid Nokia stock over the period 2003-2008 with the aim of determining the relative role of endogenous and...

Identification of market abuse is an extremely complicated activity that requires the analysis of large and complex datasets. We propose an unsupervised machine learning method for contextual anomal...

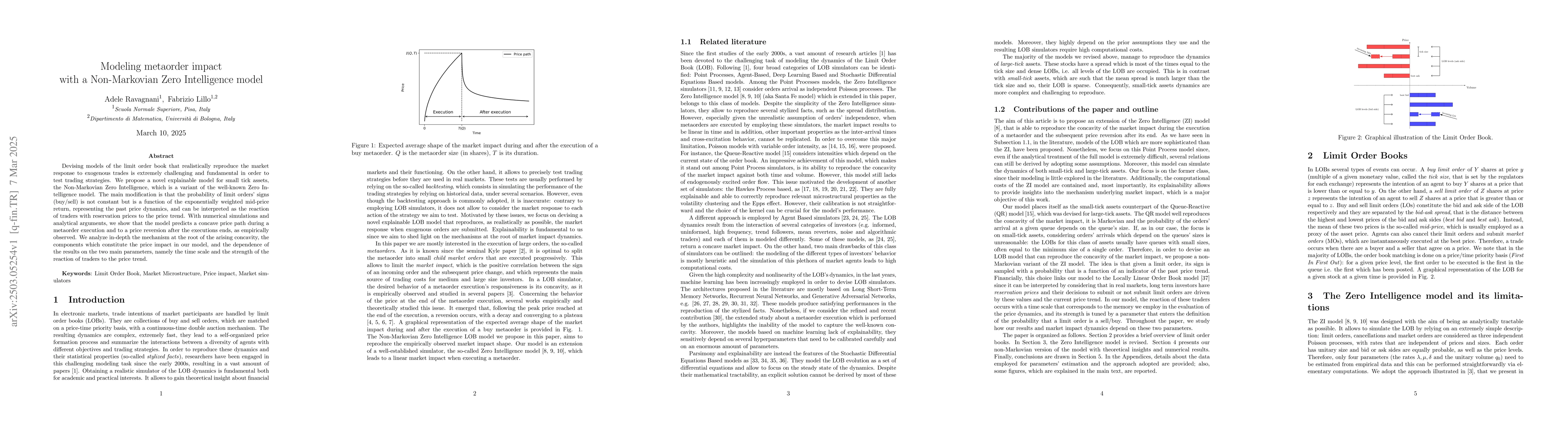

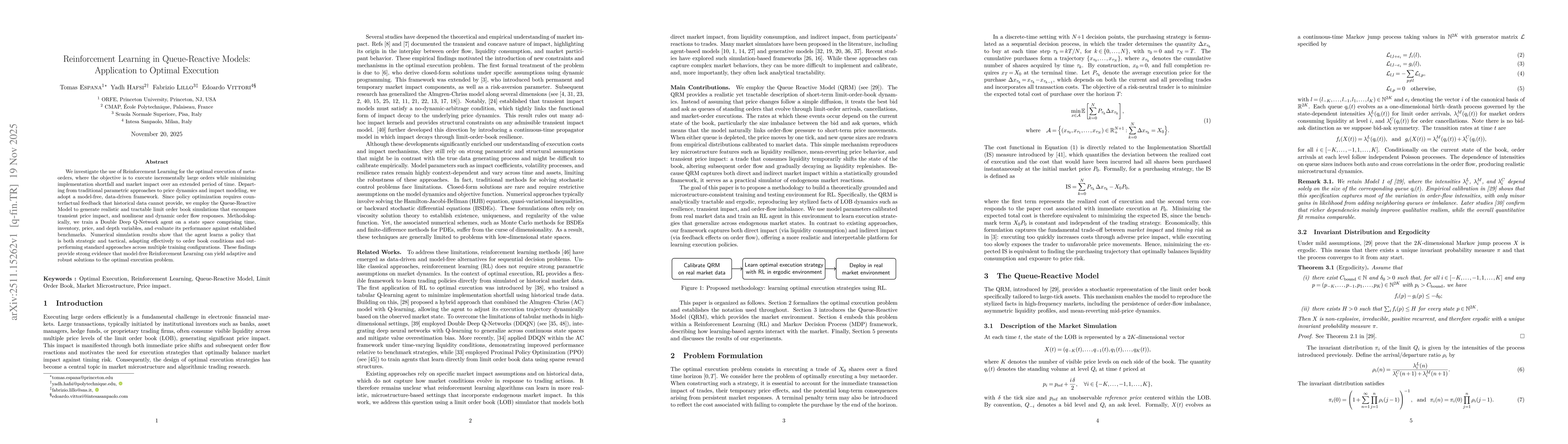

Optimal execution is an important problem faced by any trader. Most solutions are based on the assumption of constant market impact, while liquidity is known to be dynamic. Moreover, models with tim...

Financial order flow exhibits a remarkable level of persistence, wherein buy (sell) trades are often followed by subsequent buy (sell) trades over extended periods. This persistence can be attribute...

Identifying market abuse activity from data on investors' trading activity is very challenging both for the data volume and for the low signal to noise ratio. Here we propose two complementary unsup...

This paper presents results from the SESAR ER3 Domino project. Three mechanisms are assessed at the ECAC-wide level: 4D trajectory adjustments (a combination of actively waiting for connecting passe...

This paper investigates how Covid mobility restrictions impacted the population of investors of the Italian stock market. The analysis tracks the trading activity of individual investors in Italian ...

A large body of empirical literature has shown that market impact of financial prices is transient. However, from a theoretical standpoint, the origin of this temporary nature is still unclear. We s...

The estimation of the volatility with high-frequency data is plagued by the presence of microstructure noise, which leads to biased measures. Alternative estimators have been developed and tested ei...

While the vast majority of the literature on models for temporal networks focuses on binary graphs, often one can associate a weight to each link. In such cases the data are better described by a we...

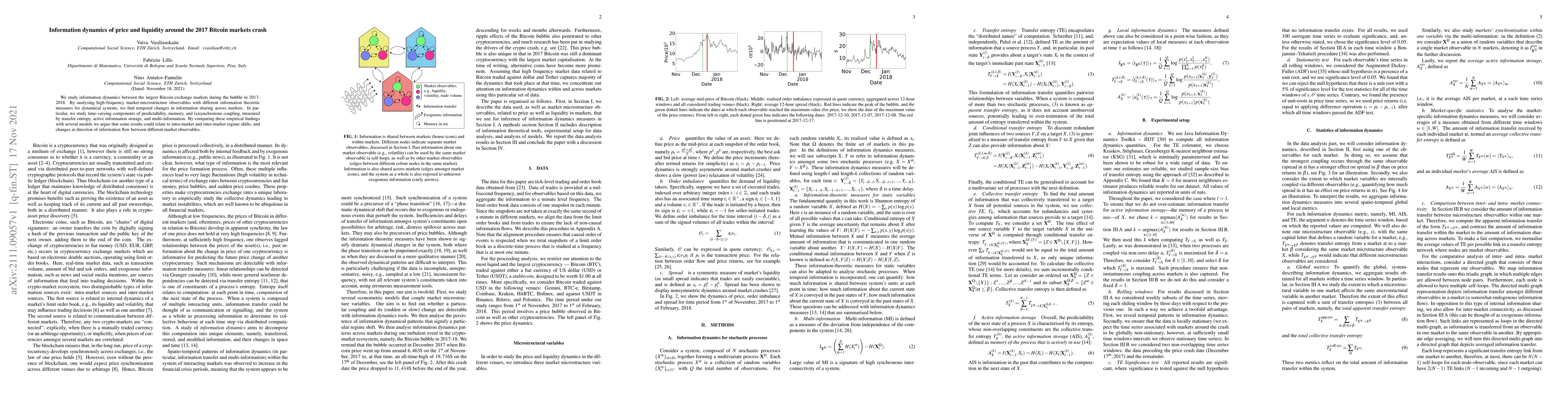

We study the information dynamics between the largest Bitcoin exchange markets during the bubble in 2017-2018. By analysing high-frequency market-microstructure observables with different informatio...

I present an overview of some recent advancements on the empirical analysis and theoretical modeling of the process of price formation in financial markets as the result of the arrival of orders in ...

We consider a model of a simple financial system consisting of a leveraged investor that invests in a risky asset and manages risk by using Value-at-Risk (VaR). The VaR is estimated by using past da...

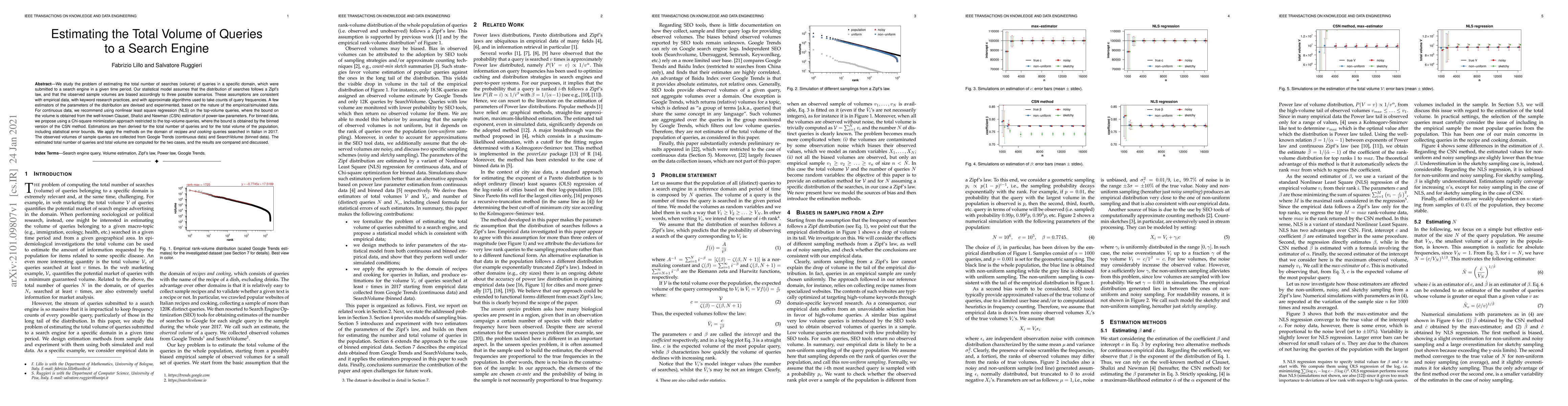

We study the problem of estimating the total number of searches (volume) of queries in a specific domain, which were submitted to a search engine in a given time period. Our statistical model assume...

We consider the general problem of a set of agents trading a portfolio of assets in the presence of transient price impact and additional quadratic transaction costs and we study, with analytical an...

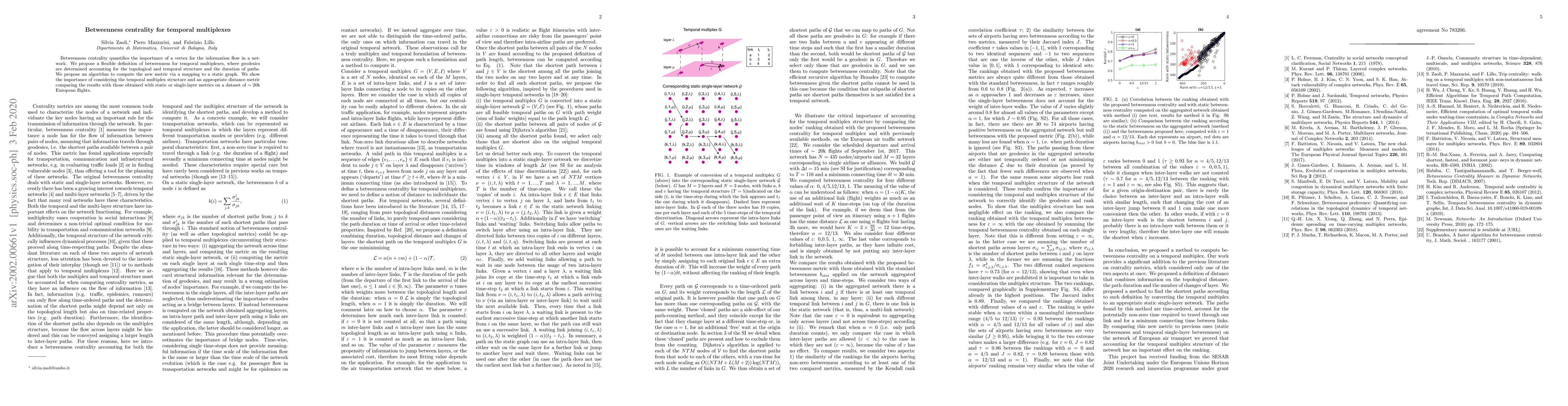

Betweenness centrality quantifies the importance of a vertex for the information flow in a network. We propose a flexible definition of betweenness for temporal multiplexes, where geodesics are dete...

We propose a method to infer lead-lag networks of traders from the observation of their trade record as well as to reconstruct their state of supply and demand when they do not trade. The method rel...

The complex networks approach has been gaining popularity in analysing investor behaviour and stock markets, but within this approach, initial public offerings (IPO) have barely been explored. We fi...

We consider the problem of inferring a causality structure from multiple binary time series by using the Kinetic Ising Model in datasets where a fraction of observations is missing. We take our step...

Using a perturbation technique, we derive a new approximate filtering and smoothing methodology generalizing along different directions several existing approaches to robust filtering based on the s...

Change points in real-world systems mark significant regime shifts in system dynamics, possibly triggered by exogenous or endogenous factors. These points define regimes for the time evolution of the ...

The use of reinforcement learning algorithms in financial trading is becoming increasingly prevalent. However, the autonomous nature of these algorithms can lead to unexpected outcomes that deviate fr...

We propose a theory of unimodal maps perturbed by an heteroscedastic Markov chain noise and experiencing another heteroscedastic noise due to uncertain observation. We address and treat the filtering ...

In financial risk management, Value at Risk (VaR) is widely used to estimate potential portfolio losses. VaR's limitation is its inability to account for the magnitude of losses beyond a certain thres...

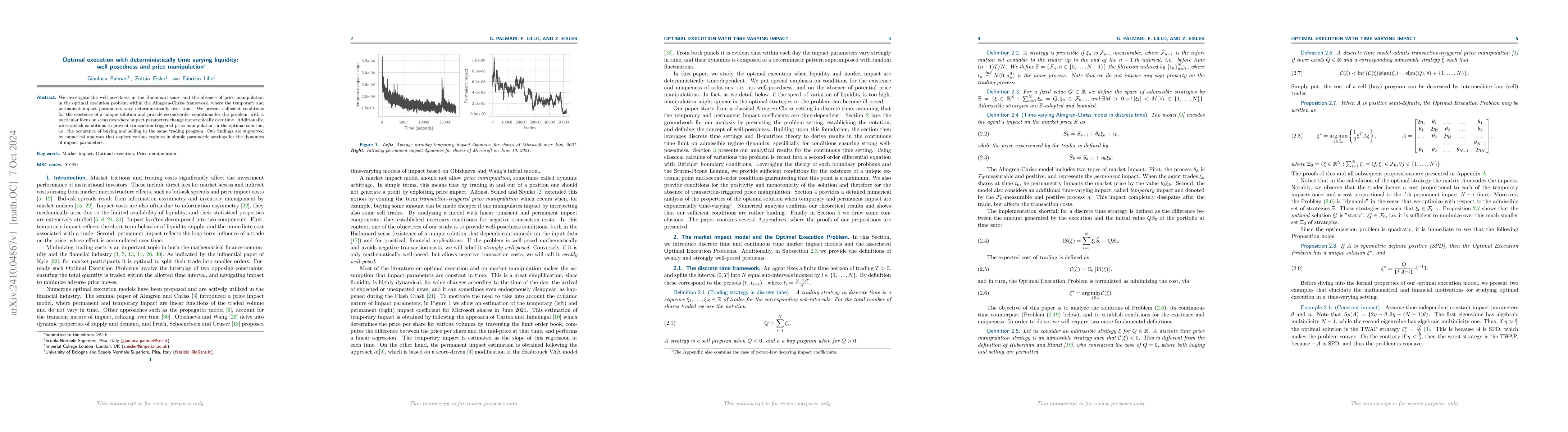

We investigate the well-posedness in the Hadamard sense and the absence of price manipulation in the optimal execution problem within the Almgren-Chriss framework, where the temporary and permanent im...

Modelling how a shock propagates in a temporal network and how the system relaxes back to equilibrium is challenging but important in many applications, such as financial systemic risk. Most studies s...

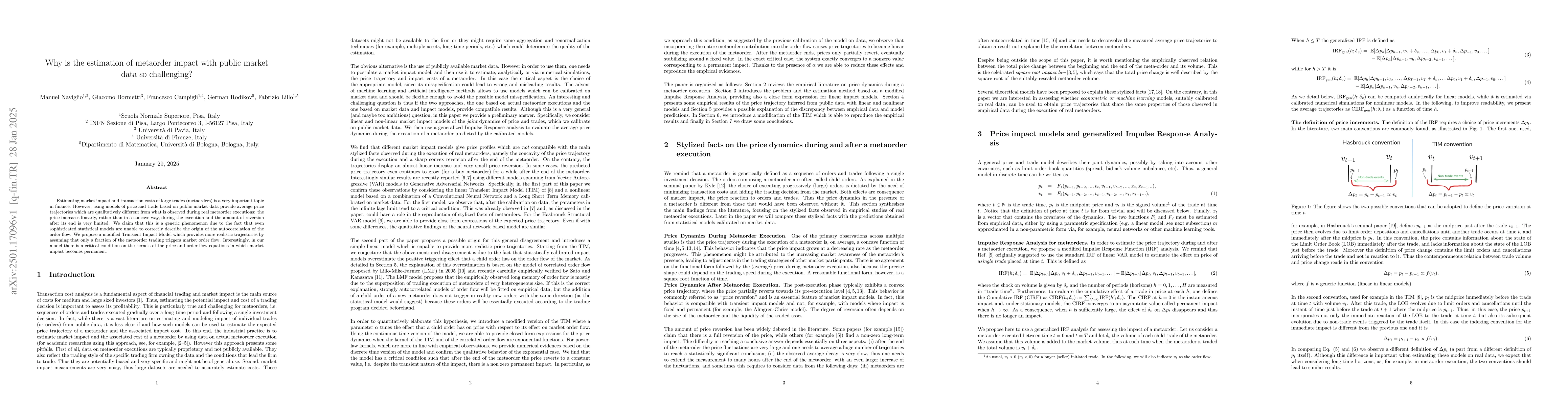

Estimating market impact and transaction costs of large trades (metaorders) is a very important topic in finance. However, using models of price and trade based on public market data provide average p...

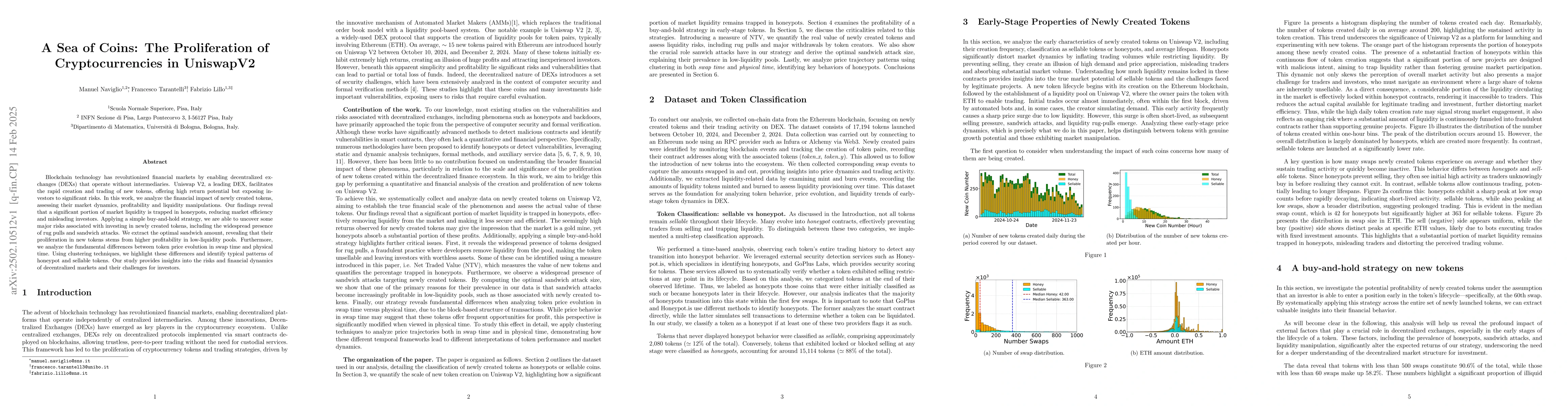

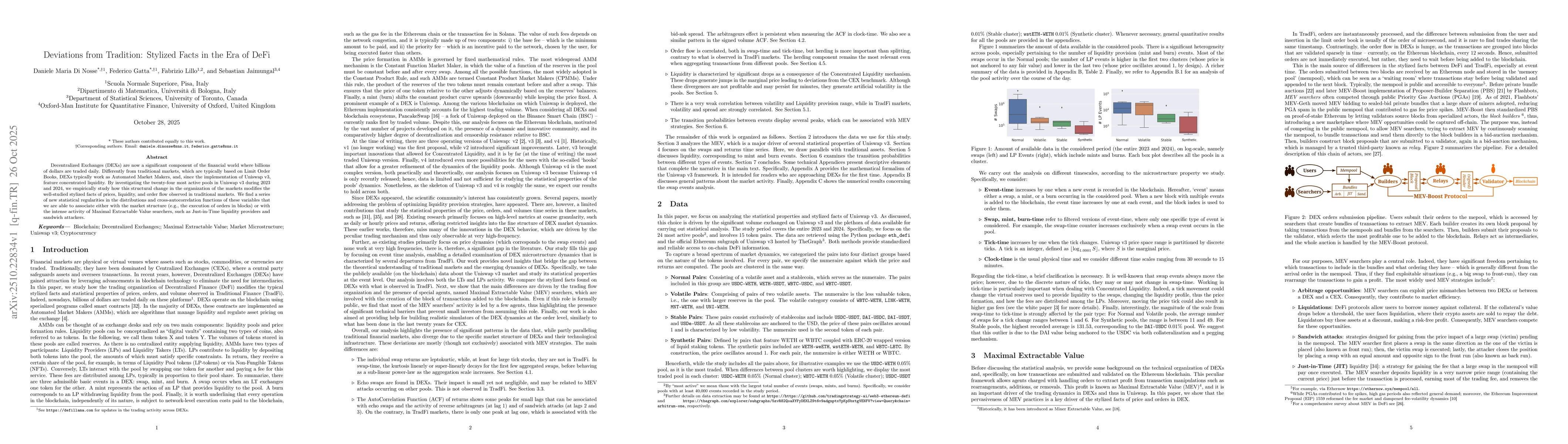

Blockchain technology has revolutionized financial markets by enabling decentralized exchanges (DEXs) that operate without intermediaries. Uniswap V2, a leading DEX, facilitates the rapid creation and...

Devising models of the limit order book that realistically reproduce the market response to exogenous trades is extremely challenging and fundamental in order to test trading strategies. We propose a ...

The Kelly criterion provides a general framework for optimizing the growth rate of an investment portfolio over time by maximizing the expected logarithmic utility of wealth. However, the optimality c...

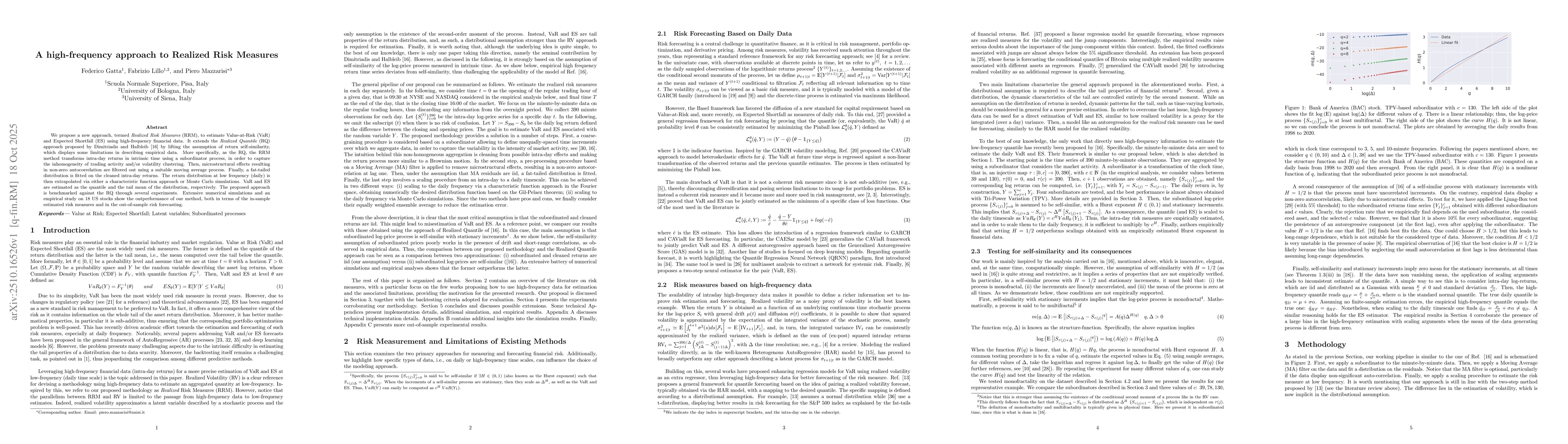

We propose a new approach, termed Realized Risk Measures (RRM), to estimate Value-at-Risk (VaR) and Expected Shortfall (ES) using high-frequency financial data. It extends the Realized Quantile (RQ) a...

Decentralized Exchanges (DEXs) are now a significant component of the financial world where billions of dollars are traded daily. Differently from traditional markets, which are typically based on Lim...

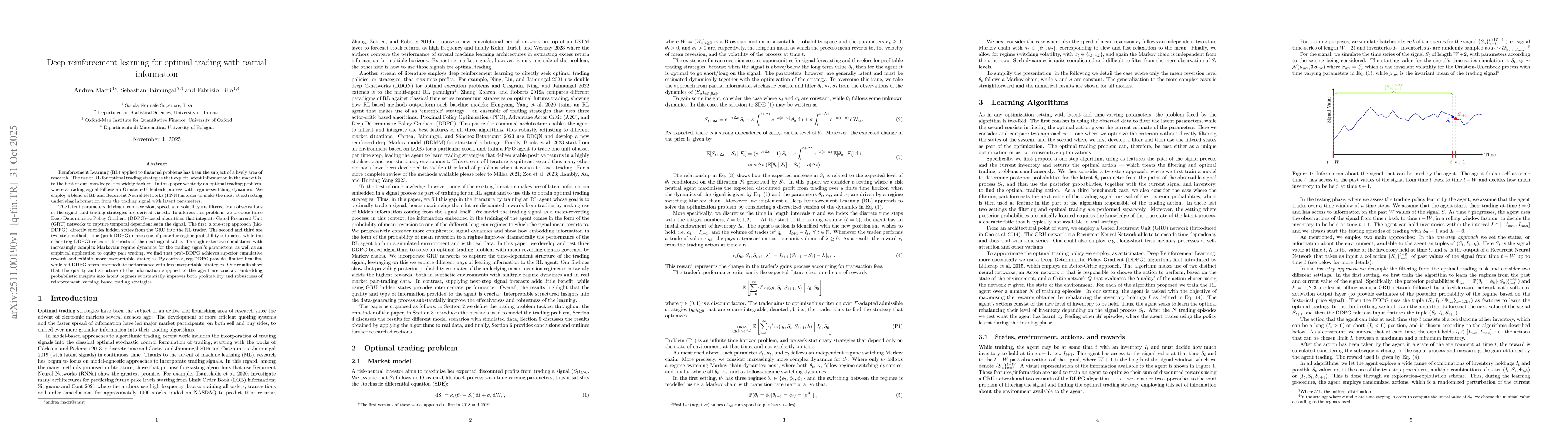

Reinforcement Learning (RL) applied to financial problems has been the subject of a lively area of research. The use of RL for optimal trading strategies that exploit latent information in the market ...

We investigate the use of Reinforcement Learning for the optimal execution of meta-orders, where the objective is to execute incrementally large orders while minimizing implementation shortfall and ma...

We study the dynamics of token launched on Pump.fun, a Solana-based launchpad platform, to identify the determinants of the token success. Pump.fun employs a bonding curve mechanism to bootstrap initi...

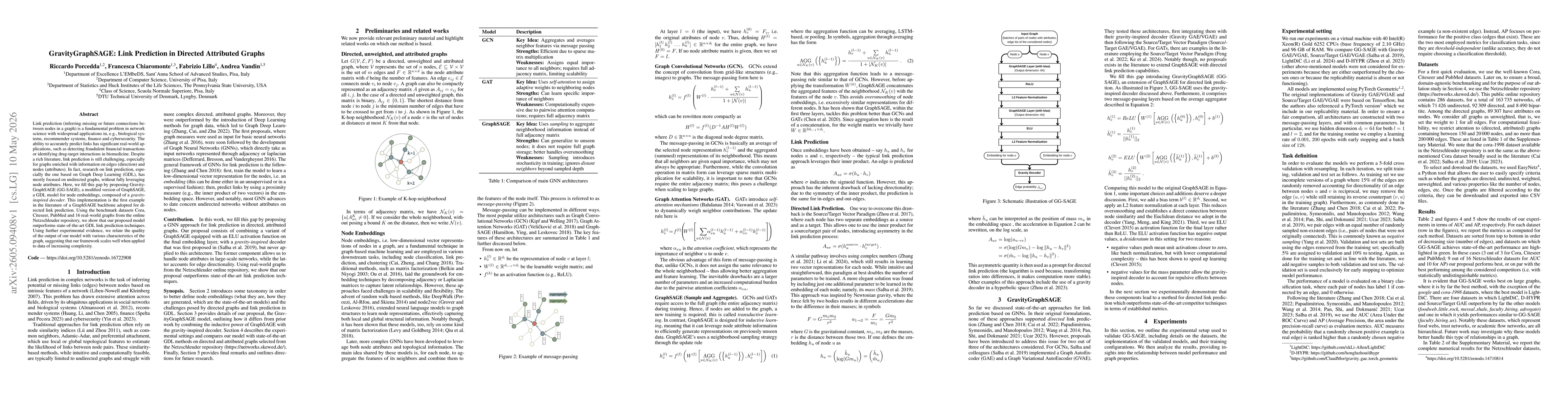

Link prediction (inferring missing or future connections between nodes in a graph) is a fundamental problem in network science with widespread applications in, e.g., biological systems, recommender sy...

Sunshine trading theory predicts that publicly disclosing trading intentions can reduce adverse selection and attract liquidity provision, lowering execution costs. Evidence is scarce, because explici...

Automated Market Makers based on concentrated liquidity, such as Uniswap v3, significantly improve capital efficiency but expose Liquidity Providers (LPs) to adverse selection costs, formalized as Los...