In this paper, we model USD-CNY bilateral exchange rate fluctuations as a

general stochastic process and incorporate monetary policy shock to examine how

bilateral exchange rate fluctuations affect the Revealed Comparative Advantage

(RCA) index. Numerical simulations indicate that as the mean of bilateral

exchange rate fluctuations increases, i.e., currency devaluation, the RCA index

rises. Moreover, smaller bilateral exchange rate fluctuations after the policy

shock cause the RCA index to gradually converge toward its mean level. For the

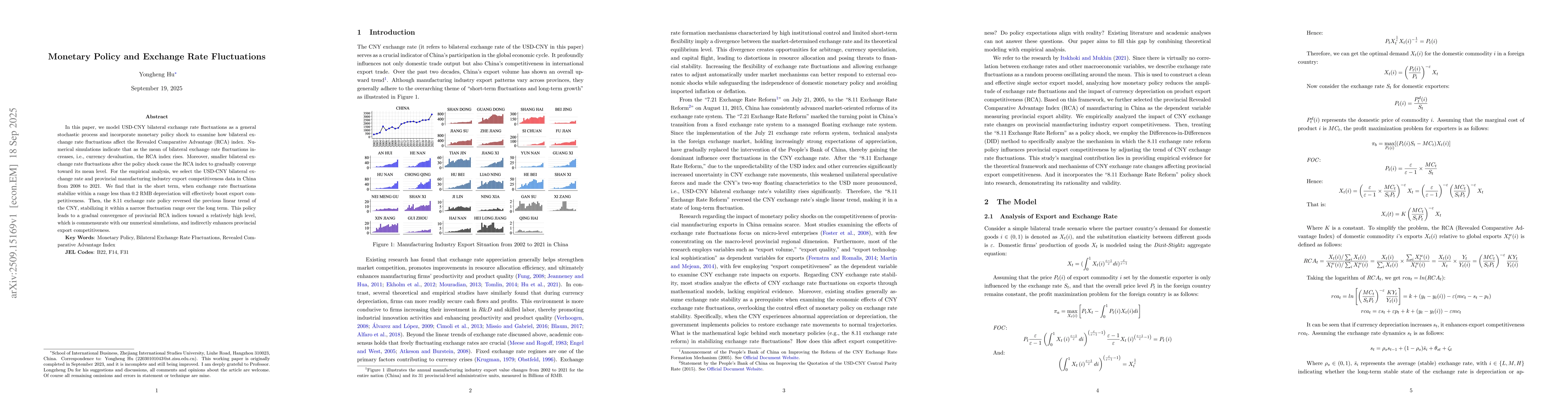

empirical analysis, we select the USD-CNY bilateral exchange rate and

provincial manufacturing industry export competitiveness data in China from

2008 to 2021. We find that in the short term, when exchange rate fluctuations

stabilize within a range less than 0.2 RMB depreciation will effectively boost

export competitiveness. Then, the 8.11 exchange rate policy reversed the

previous linear trend of the CNY, stabilizing it within a narrow fluctuation

range over the long term. This policy leads to a gradual convergence of

provincial RCA indices toward a relatively high level, which is commensurate

with our numerical simulations, and indirectly enhances provincial export

competitiveness.

Discussion 0