Credit Default Swaps (CDS) on a reference entity may be traded in multiple

currencies, in that protection upon default may be offered either in the

domestic currency where the entity resides, or in a more liquid and global

foreign currency. In this situation currency fluctuations clearly introduce a

source of risk on CDS spreads. For emerging markets, but in some cases even in

well developed markets, the risk of dramatic Foreign Exchange (FX) rate

devaluation in conjunction with default events is relevant. We address this

issue by proposing and implementing a model that considers the risk of foreign

currency devaluation that is synchronous with default of the reference entity.

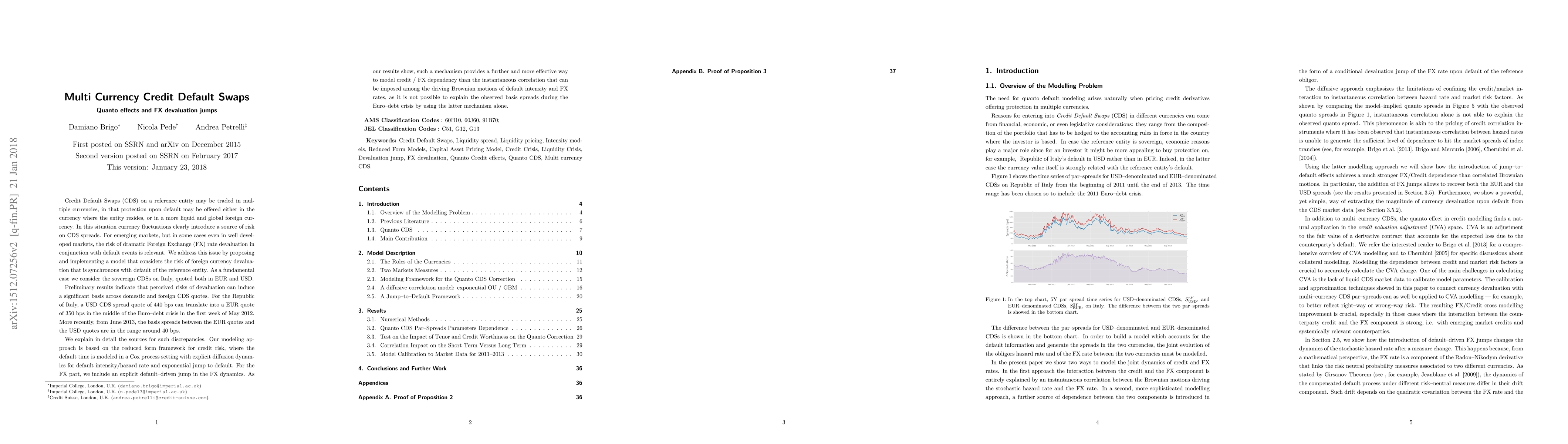

Preliminary results indicate that perceived risks of devaluation can induce a

significant basis across domestic and foreign CDS quotes. For the Republic of

Italy, a USD CDS spread quote of 440 bps can translate into a EUR quote of 350

bps in the middle of the Euro-debt crisis in the first week of May 2012. More

recently, from June 2013, the basis spreads between the EUR quotes and the USD

quotes are in the range around 40 bps.

We explain in detail the sources for such discrepancies. Our modeling

approach is based on the reduced form framework for credit risk, where the

default time is modeled in a Cox process setting with explicit diffusion

dynamics for default intensity/hazard rate and exponential jump to default. For

the FX part, we include an explicit default-driven jump in the FX dynamics. As

our results show, such a mechanism provides a further and more effective way to

model credit / FX dependency than the instantaneous correlation that can be

imposed among the driving Brownian motions of default intensity and FX rates,

as it is not possible to explain the observed basis spreads during the

Euro-debt crisis by using the latter mechanism alone.

Discussion 0