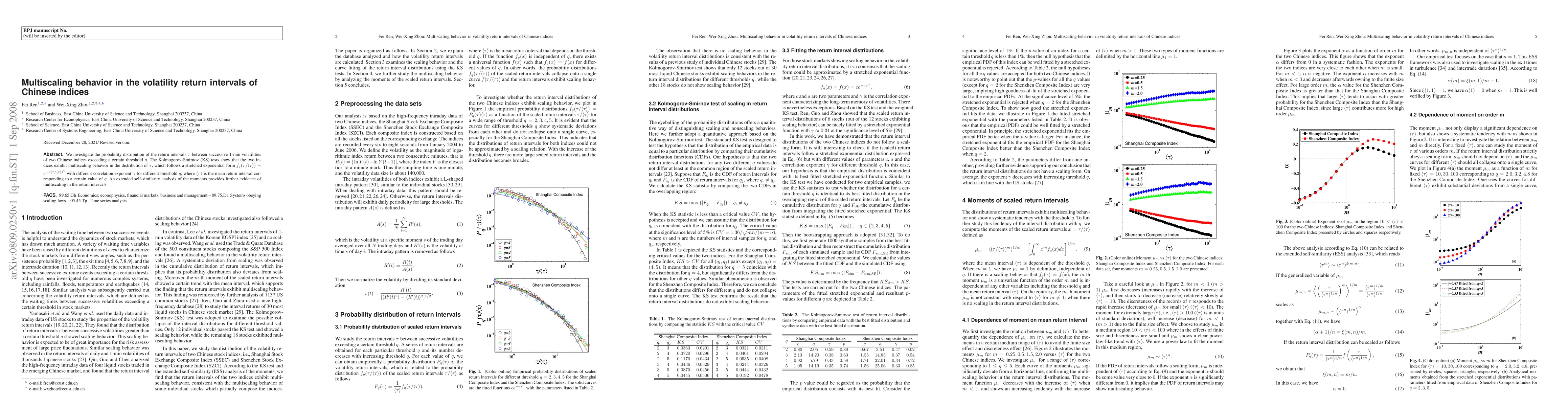

We investigate the probability distribution of the return intervals $\tau$

between successive 1-min volatilities of two Chinese indices exceeding a

certain threshold $q$. The Kolmogorov-Smirnov (KS) tests show that the two

indices exhibit multiscaling behavior in the distribution of $\tau$, which

follows a stretched exponential form $f_q(\tau/< \tau >)\sim e^{- a(\tau/ <

\tau >)^{\gamma}}$ with different correlation exponent $\gamma$ for different

threshold $q$, where $<\tau>$ is the mean return interval corresponding to a

certain value of $q$. An extended self-similarity analysis of the moments

provides further evidence of multiscaling in the return intervals.

Discussion 0