On the universality of the volatility formation process: when machine learning and rough volatility agree

Publication

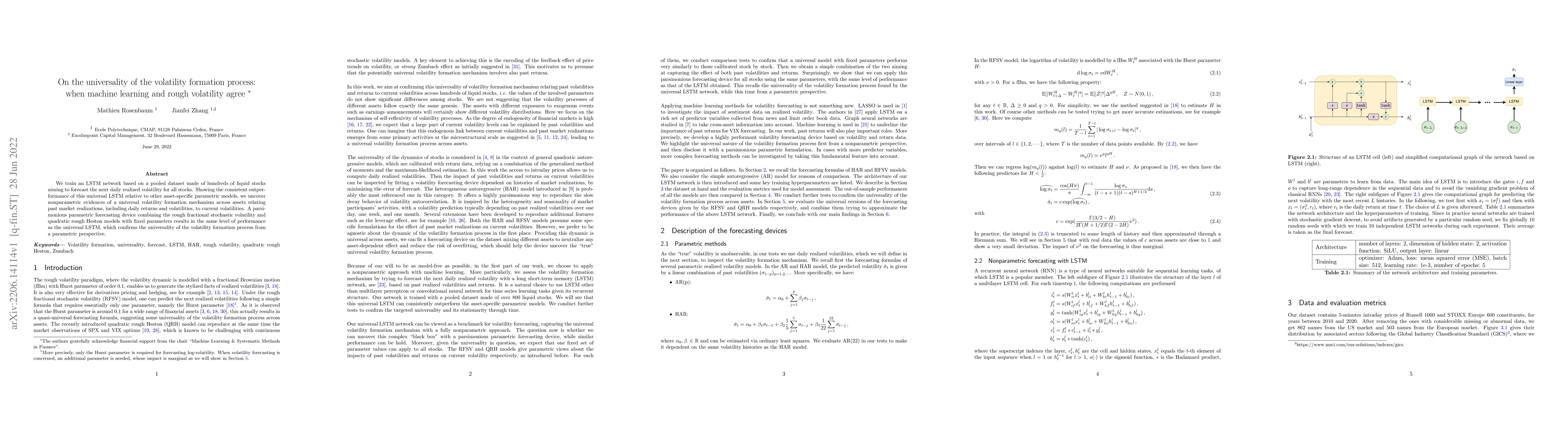

Metrics

AI Quick Summary

This paper demonstrates that an LSTM network trained on a dataset of liquid stocks consistently outperforms asset-specific models in forecasting daily realized volatility, suggesting a universal volatility formation process. The study also finds that a parametric model combining rough fractional stochastic volatility and quadratic rough Heston models achieves similar performance, confirming the universality of the volatility formation process.

Paper Preview

Abstract

We train an LSTM network based on a pooled dataset made of hundreds of liquid stocks aiming to forecast the next daily realized volatility for all stocks. Showing the consistent outperformance of this universal LSTM relative to other asset-specific parametric models, we uncover nonparametric evidences of a universal volatility formation mechanism across assets relating past market realizations, including daily returns and volatilities, to current volatilities. A parsimonious parametric forecasting device combining the rough fractional stochastic volatility and quadratic rough Heston models with fixed parameters results in the same level of performance as the universal LSTM, which confirms the universality of the volatility formation process from a parametric perspective.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0