Academic Profile

Statistics

Similar Authors

Papers on arXiv

The goal of this paper is to disentangle the roles of volume and of participation rate in the price response of the market to a sequence of transactions. To do so, we are inspired the methodology in...

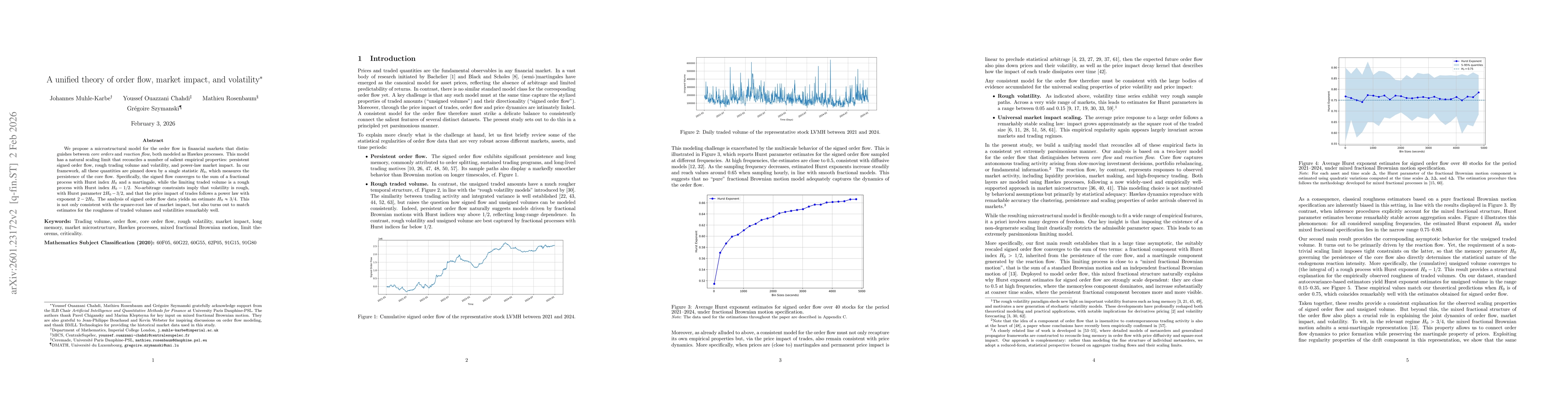

We extend the application and test the performance of a recently introduced volatility prediction framework encompassing LSTM and rough volatility. Our asset class of interest is cryptocurrencies, a...

Transfer learning is an emerging and popular paradigm for utilizing existing knowledge from previous learning tasks to improve the performance of new ones. In this paper, we propose a novel concept ...

We study a toy two-player game for periodic double auction markets to generate liquidity. The game has imperfect information, which allows us to link market spreads with signal strength. We characte...

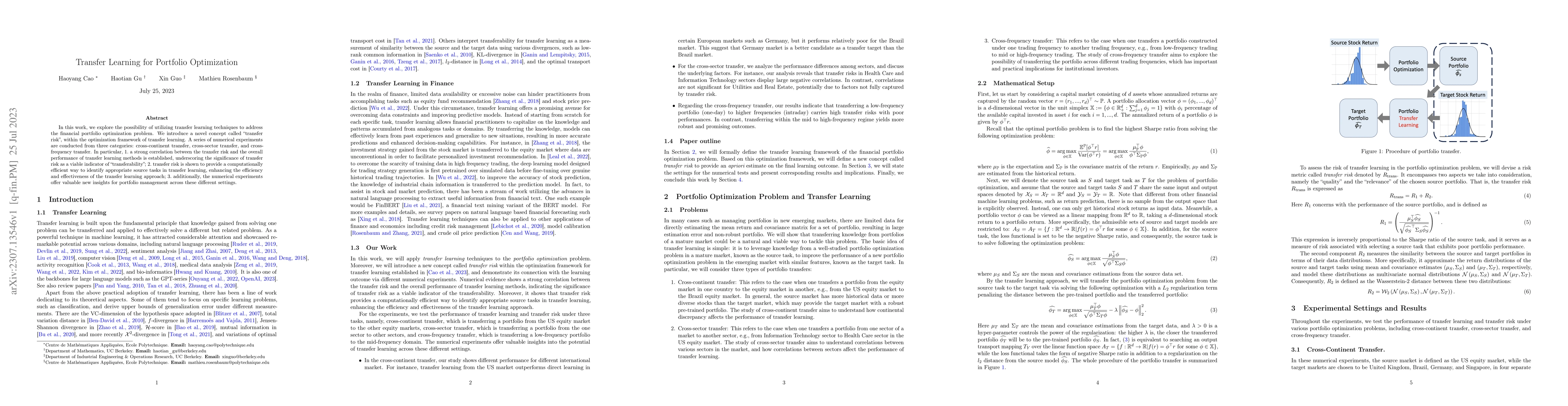

In this work, we explore the possibility of utilizing transfer learning techniques to address the financial portfolio optimization problem. We introduce a novel concept called "transfer risk", withi...

News can convey bearish or bullish views on financial assets. Institutional investors need to evaluate automatically the implied news sentiment based on textual data. Given the huge amount of news a...

Transfer learning is an emerging and popular paradigm for utilizing existing knowledge from previous learning tasks to improve the performance of new ones. Despite its numerous empirical successes, ...

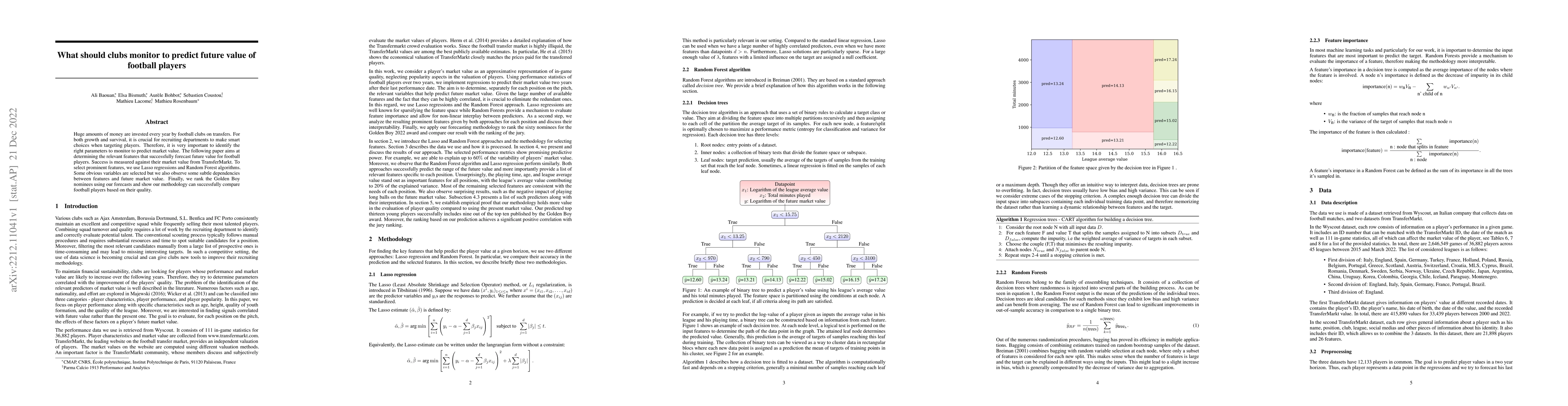

Huge amounts of money are invested every year by football clubs on transfers. For both growth and survival, it is crucial for recruiting departments to make smart choices when targeting players. The...

Given the promising results on joint modeling of SPX/VIX smiles of the recently introduced quadratic rough Heston model, we consider a multi-asset market making problem on SPX and its derivatives, e...

With an increasing amount of data in the art world, discovering artists and artworks suitable to collectors' tastes becomes a challenge. It is no longer enough to use visual information, as contextu...

In recent years, there has been a substantive interest in rough volatility models. In this class of models, the local behavior of stochastic volatility is much more irregular than semimartingales an...

Rough volatility models have gained considerable interest in the quantitative finance community in recent years. In this paradigm, the volatility of the asset price is driven by a fractional Brownia...

Recommendation systems have been widely used in various domains such as music, films, e-shopping etc. After mostly avoiding digitization, the art world has recently reached a technological turning p...

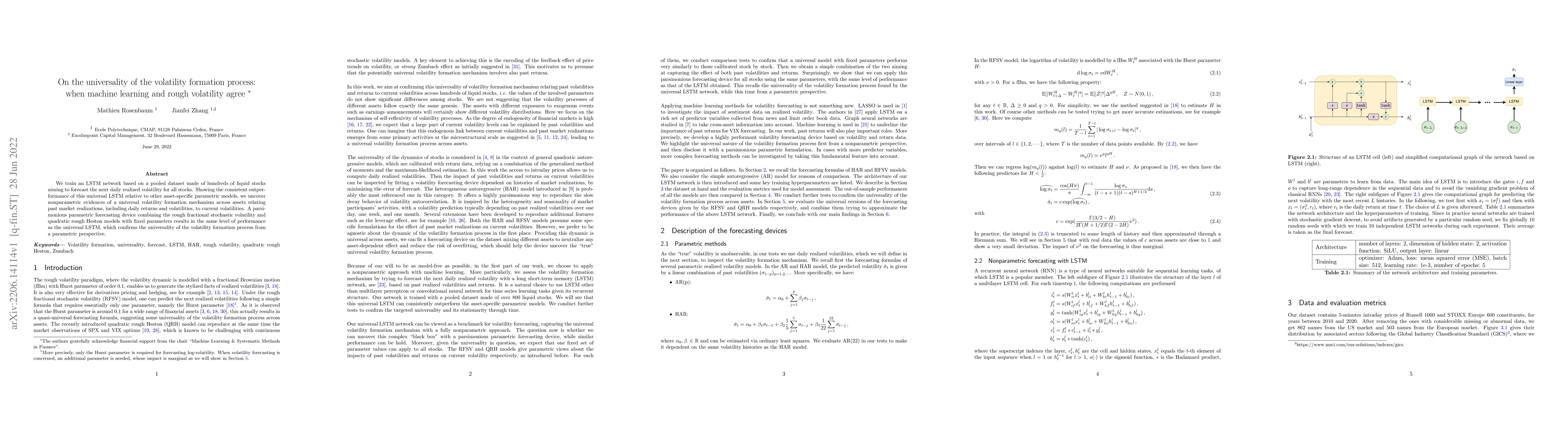

We train an LSTM network based on a pooled dataset made of hundreds of liquid stocks aiming to forecast the next daily realized volatility for all stocks. Showing the consistent outperformance of th...

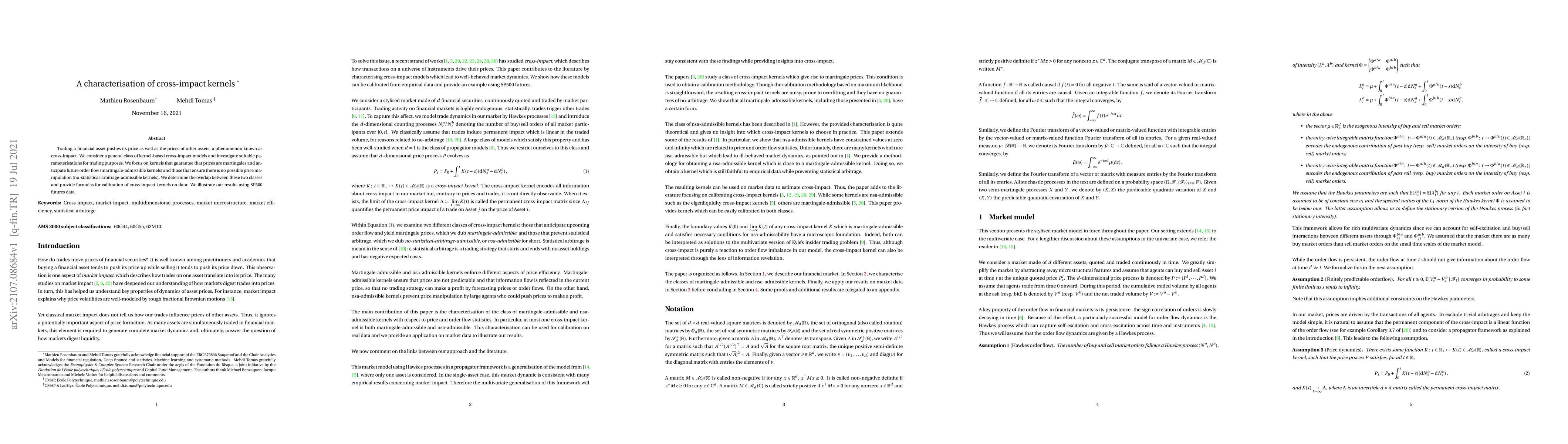

Trading a financial asset pushes its price as well as the prices of other assets, a phenomenon known as cross-impact. We consider a general class of kernel-based cross-impact models and investigate ...

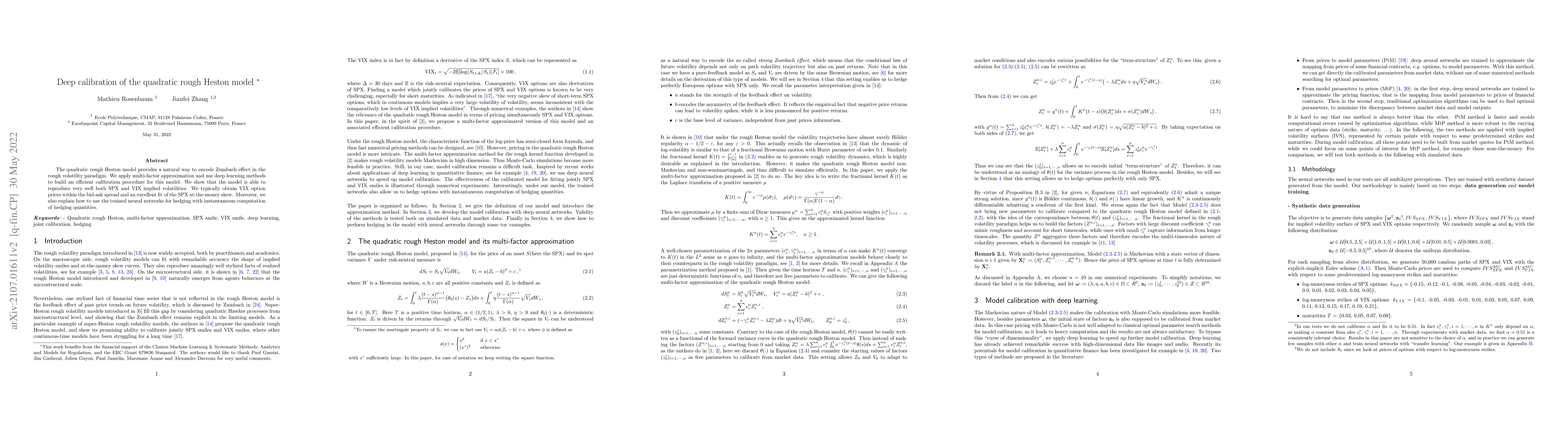

The quadratic rough Heston model provides a natural way to encode Zumbach effect in the rough volatility paradigm. We apply multi-factor approximation and use deep learning methods to build an effic...

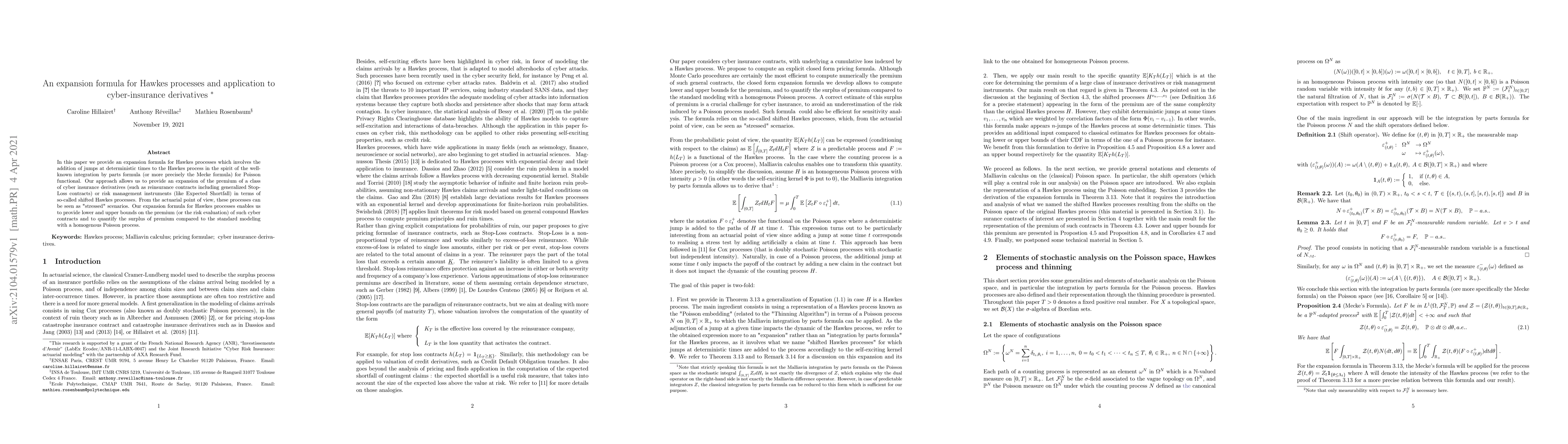

In this paper we provide an expansion formula for Hawkes processes which involves the addition of jumps at deterministic times to the Hawkes process in the spirit of the well-known integration by pa...

We introduce a new matching design for financial transactions in an electronic market. In this mechanism, called ad-hoc electronic auction design (AHEAD), market participants can trade between thems...

The tick size, which is the smallest increment between two consecutive prices for a given asset, is a key parameter of market microstructure. In particular, the behavior of high frequency market mak...

Fitting simultaneously SPX and VIX smiles is known to be one of the most challenging problems in volatility modeling. A long-standing conjecture due to Julien Guyon is that it may not be possible to...

We consider the issue of a market maker acting at the same time in the lit and dark pools of an exchange. The exchange wishes to establish a suitable make-take fees policy to attract transactions on...

We consider the problem of designing a derivatives exchange aiming at addressing clients needs in terms of listed options and providing suitable liquidity. We proceed into two steps. First we use a ...

Following the recent literature on make take fees policies, we consider an exchange wishing to set a suitable contract with several market makers in order to improve trading quality on its platform....

We propose a general non-linear order book model that is built from the individual behaviours of the agents. Our framework encompasses Markovian and Hawkes based models. Under mild assumptions, we p...

We consider an auction market in which market makers fill the order book during a given time period while some other investors send market orders. We define the clearing price of the auction as the ...

We consider an exchange who wishes to set suitable make-take fees to attract liquidity on its platform. Using a principal-agent approach, we are able to describe in quasi-explicit form the optimal c...

While the market impact of aggressive orders has been extensively studied, the impact of passive orders, those executed through limit orders, remains less understood. The goal of this paper is to inve...

This study presents a quantitative framework to compare teams in collective sports with respect to their style of play. The style of play is characterized by the team's spatial distribution over a col...

We investigate the weak limit of the hyper-rough square-root process as the Hurst index $H$ goes to $-1/2\,$. This limit corresponds to the fractional kernel $t^{H - 1 / 2}$ losing integrability. We e...

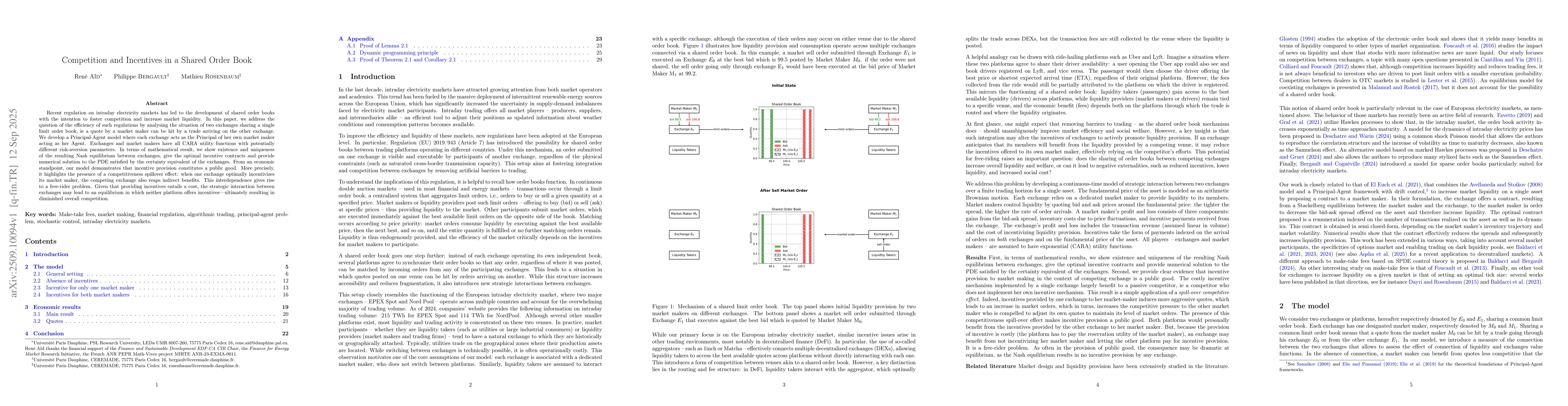

Recent regulation on intraday electricity markets has led to the development of shared order books with the intention to foster competition and increase market liquidity. In this paper, we address the...

True Volterra equations are inherently non stationary and therefore do not admit $\textit{genuine stationary regimes}$ over finite horizons. This motivates the study of the finite-time behavior of the...

We propose a microstructural model for the order flow in financial markets that distinguishes between {\it core orders} and {\it reaction flow}, both modeled as Hawkes processes. This model has a natu...

This paper investigates the asymptotic behavior of suitably time-modulated Hawkes processes with heavy-tailed kernels in a nearly unstable regime. We show that, under appropriate scaling, both the int...

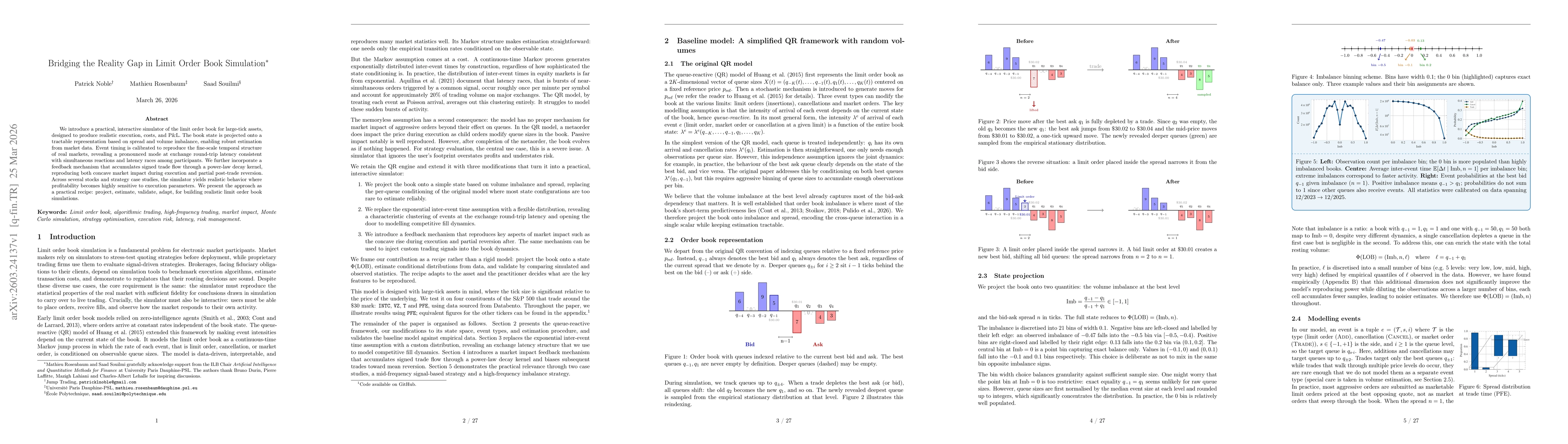

We introduce a practical, interactive simulator of the limit order book for large-tick assets, designed to produce realistic execution, costs, and P&L. The book state is projected onto a tractable rep...

Market impact is defined as the difference between the observed price trajectory under a given execution strategy and the counterfactual trajectory that would have prevailed without it. Since this cou...

We propose a new approach to model rainfall by combining heterogeneous data sources at different time scales. Continuous arrivals of rain cells are incorporated into a Hawkes process formalism that en...