Performance and Risk Analytics of Asian Exchange-Traded Funds

Publication

Metrics

Paper Preview

Abstract

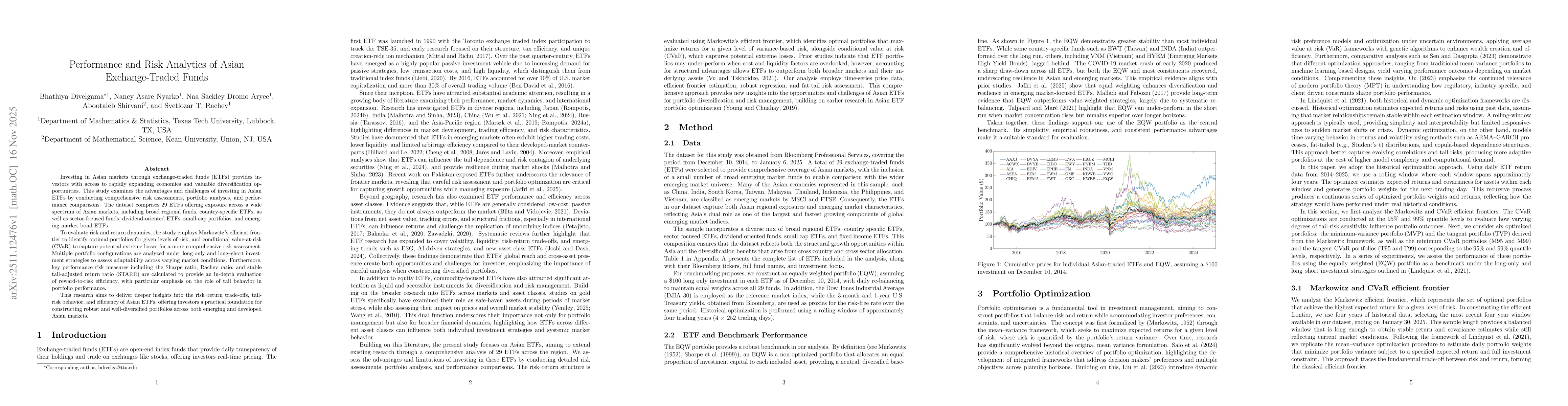

Investing in Asian markets through exchange-traded funds (ETFs) provides investors with access to rapidly expanding economies and valuable diversification opportunities. This study examines the advantages and challenges of investing in Asian ETFs by conducting comprehensive risk assessments, portfolio analyses, and performance comparisons. The dataset comprises 29 ETFs offering exposure across a wide spectrum of Asian markets, including broad regional funds, country-specific ETFs, as well as sector-focused funds, dividend-oriented ETFs, small-cap portfolios, and emerging market bond ETFs. To evaluate risk and return dynamics, the study employs Markowitz's efficient frontier to identify optimal portfolios for given levels of risk, and conditional value-at-risk (CVaR) to capture potential extreme losses for a more comprehensive risk assessment. Multiple portfolio configurations are analyzed under long-only and long-short investment strategies to assess adaptability across varying market conditions. Furthermore, key performance risk measures, including the Sharpe ratio, Rachev ratio, and stable tail-adjusted return ratio (STARR), are calculated to provide an in-depth evaluation of reward-to-risk efficiency, with particular emphasis on the role of tail behavior in portfolio performance. This research aims to deliver deeper insights into the risk-return trade-offs, tail-risk behavior, and efficiency of Asian ETFs, offering investors a practical foundation for constructing robust and well-diversified portfolios across both emerging and developed Asian markets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0