A new wave of work on covariance cleaning and nonlinear shrinkage has delivered asymptotically optimal analytical solutions for large covariance matrices. Building on this progress, these ideas have been generalized to empirical cross-covariance matrices, whose singular-value shrinkage characterizes comovements between one set of assets and another. Existing analytical cross-covariance cleaners are derived under strong stationarity and large-sample assumptions, and they typically rely on mesoscopic regularity conditions such as bounded spectra; macroscopic common modes (e.g., a global market factor) violate these conditions. When applied to real equity returns, where dependence structures drift over time and global modes are prominent, we find that these theoretically optimal formulas do not translate into robust out-of-sample performance. We address this gap by designing a random-matrix-inspired neural architecture that operates in the empirical singular-vector basis and learns a nonlinear mapping from empirical singular values to their corresponding cleaned values. By construction, the network can recover the analytical solution as a special case, yet it remains flexible enough to adapt to non-stationary dynamics and mode-driven distortions. Trained on a long history of equity returns, the proposed method achieves a more favorable bias-variance trade-off than purely analytical cleaners and delivers systematically lower out-of-sample cross-covariance prediction errors. Our results demonstrate that combining random-matrix theory with machine learning makes asymptotic theories practically effective in realistic time-varying markets.

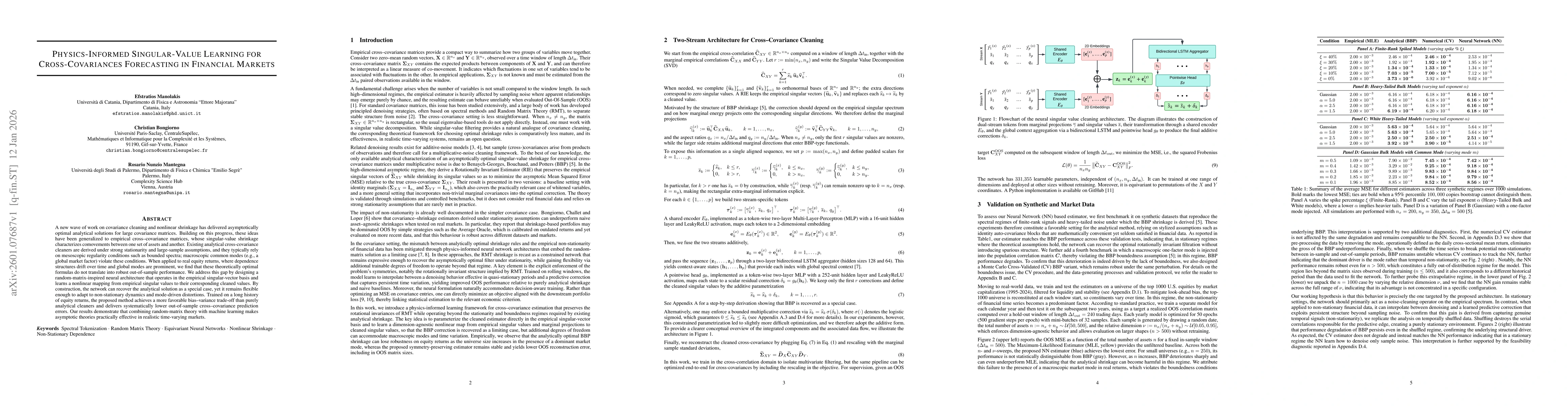

Discussion 0