Christian Bongiorno

12 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Quantifying the information lost in optimal covariance matrix cleaning

In this work, we examine the prevalent use of Frobenius error minimization in covariance matrix cleaning. Currently, minimizing the Frobenius error offers a limited interpretation within information...

Covariance matrix filtering and portfolio optimisation: the Average Oracle vs Non-Linear Shrinkage and all the variants of DCC-NLS

The Average Oracle, a simple and very fast covariance filtering method, is shown to yield superior Sharpe ratios than the current state-of-the-art (and complex) methods, Dynamic Conditional Covarian...

Optimal Covariance Cleaning for Heavy-Tailed Distributions: Insights from Information Theory

In optimal covariance cleaning theory, minimizing the Frobenius norm between the true population covariance matrix and a rotational invariant estimator is a key step. This estimator can be obtained ...

Statistical inference of lead-lag at various timescales between asynchronous time series from p-values of transfer entropy

Symbolic transfer entropy is a powerful non-parametric tool to detect lead-lag between time series. Because a closed expression of the distribution of Transfer Entropy is not known for finite-size s...

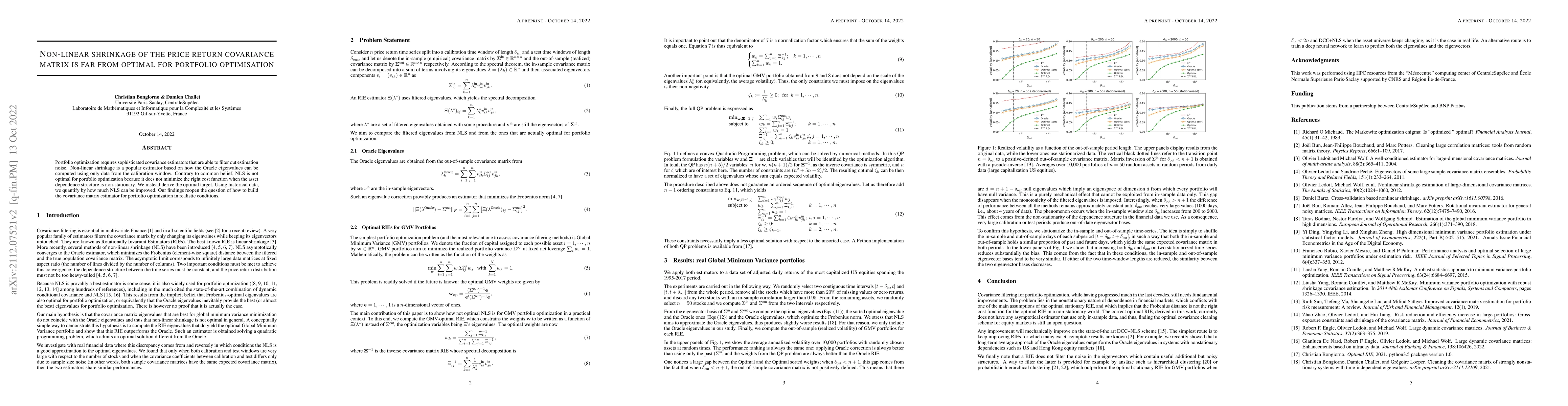

Non-linear shrinkage of the price return covariance matrix is far from optimal for portfolio optimisation

Portfolio optimization requires sophisticated covariance estimators that are able to filter out estimation noise. Non-linear shrinkage is a popular estimator based on how the Oracle eigenvalues can ...

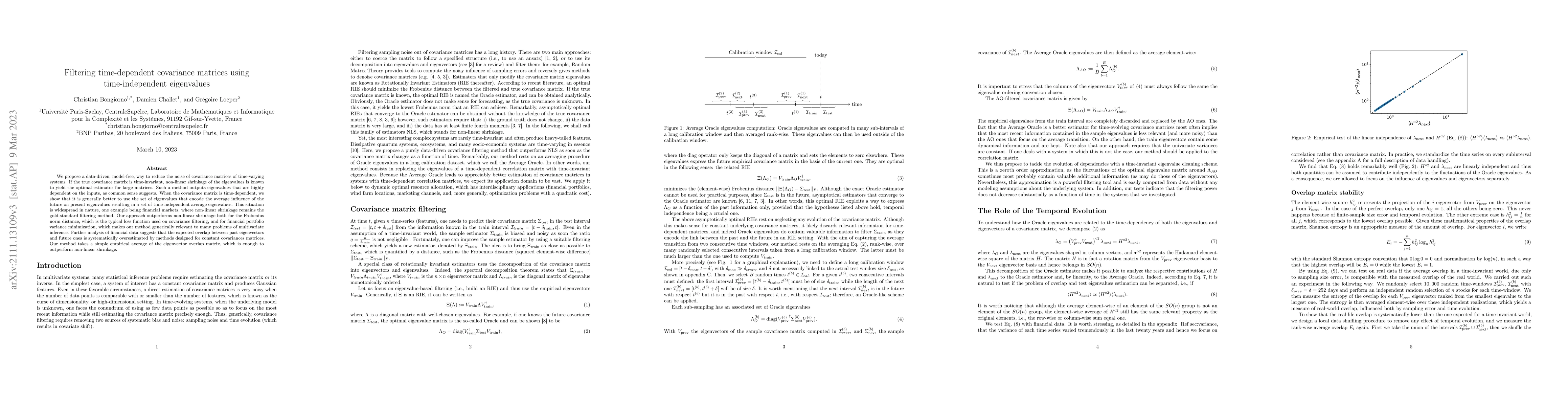

Cleaning the covariance matrix of strongly nonstationary systems with time-independent eigenvalues

We propose a data-driven way to reduce the noise of covariance matrices of nonstationary systems. In the case of stationary systems, asymptotic approaches were proved to converge to the optimal solu...

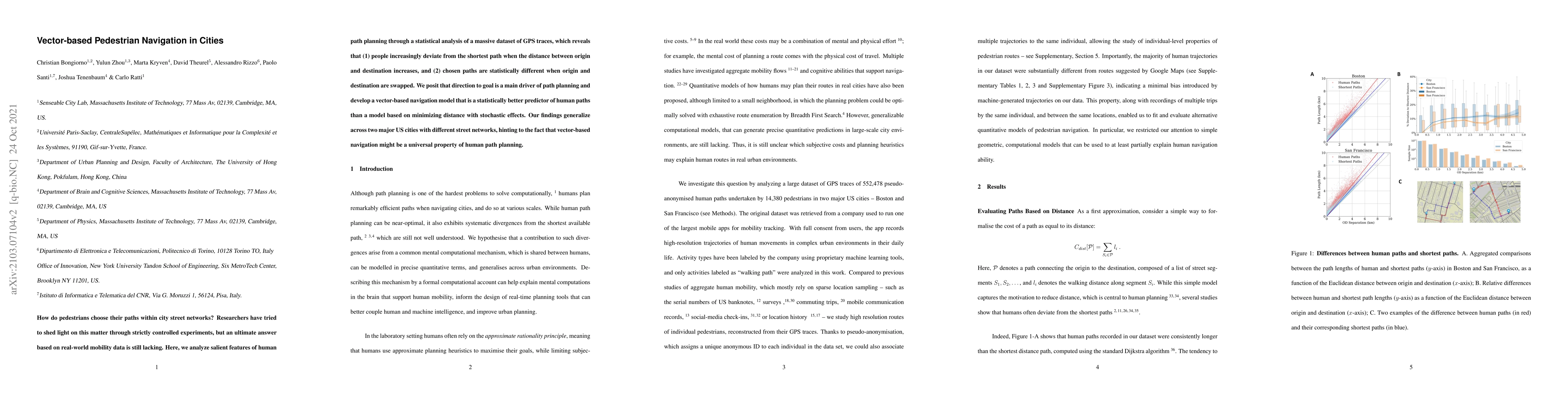

Vector-based Pedestrian Navigation in Cities

How do pedestrians choose their paths within city street networks? Researchers have tried to shed light on this matter through strictly controlled experiments, but an ultimate answer based on real-w...

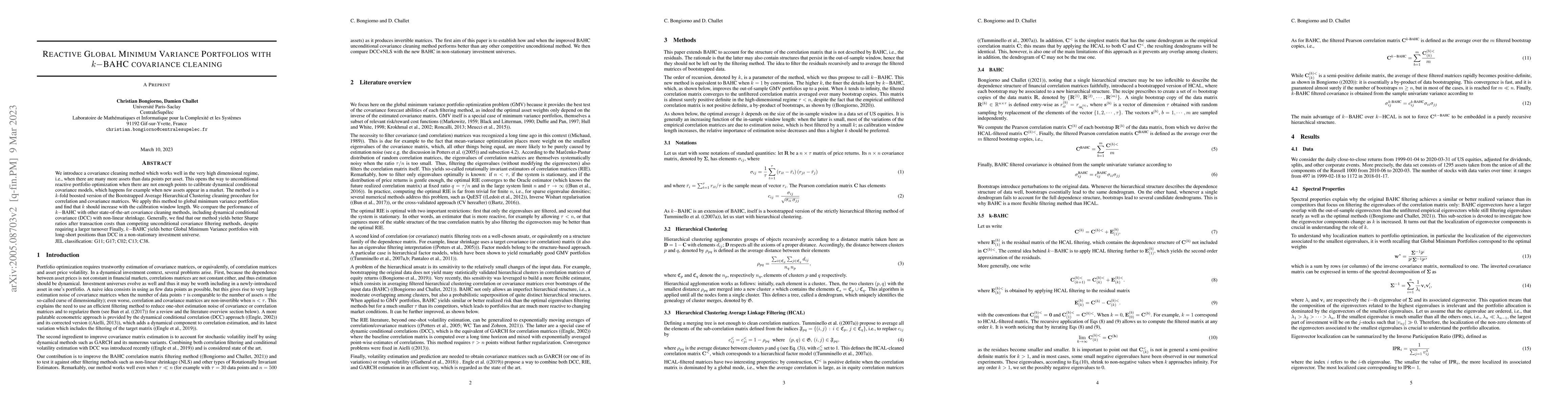

Reactive Global Minimum Variance Portfolios with $k-$BAHC covariance cleaning

We introduce a $k$-fold boosted version of our Boostrapped Average Hierarchical Clustering cleaning procedure for correlation and covariance matrices. We then apply this method to global minimum var...

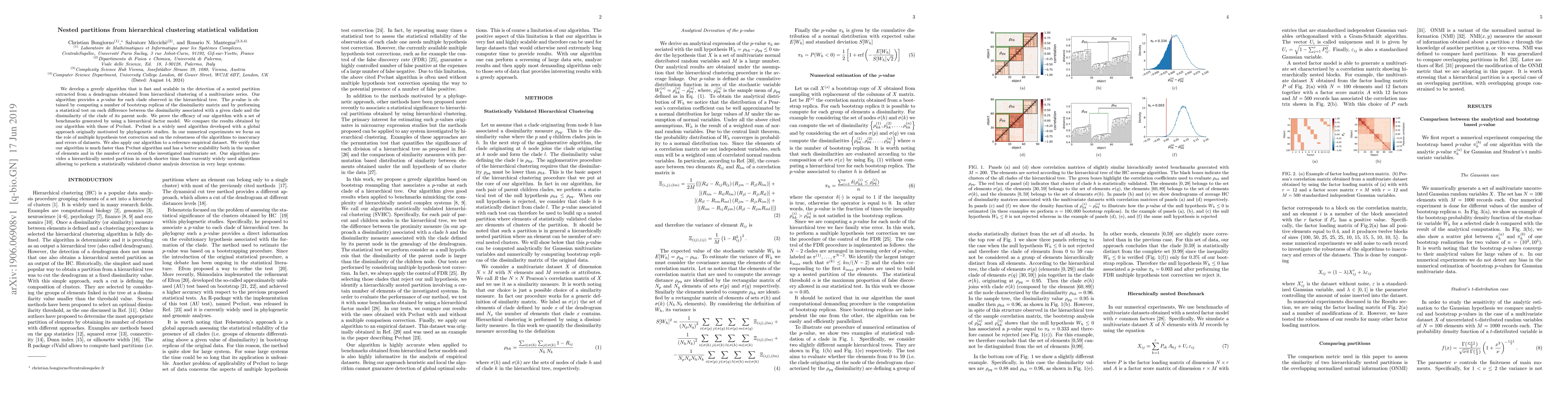

Nested partitions from hierarchical clustering statistical validation

We develop a greedy algorithm that is fast and scalable in the detection of a nested partition extracted from a dendrogram obtained from hierarchical clustering of a multivariate series. Our algorit...

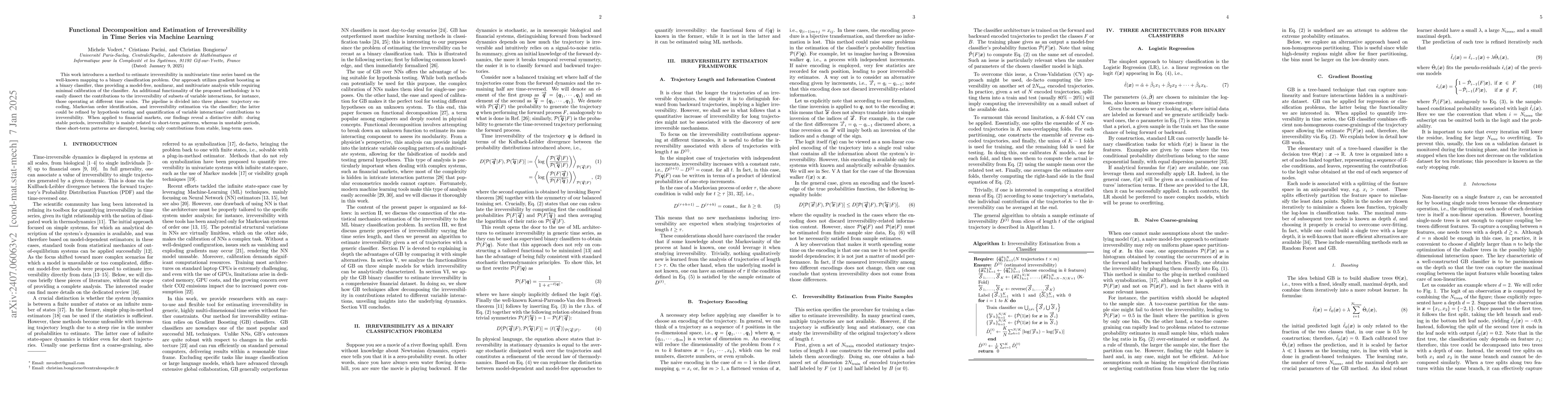

Functional Decomposition and Estimation of Irreversibility in Time Series via Machine Learning

This work introduces a novel, simple, and flexible method to quantify irreversibility in generic high-dimensional time series based on the well-known mapping to a binary classification problem. Our ap...

Optimal Data Splitting for Holdout Cross-Validation in Large Covariance Matrix Estimation

Cross-validation is a statistical tool that can be used to improve large covariance matrix estimation. Although its efficiency is observed in practical applications, the theoretical reasons behind it ...

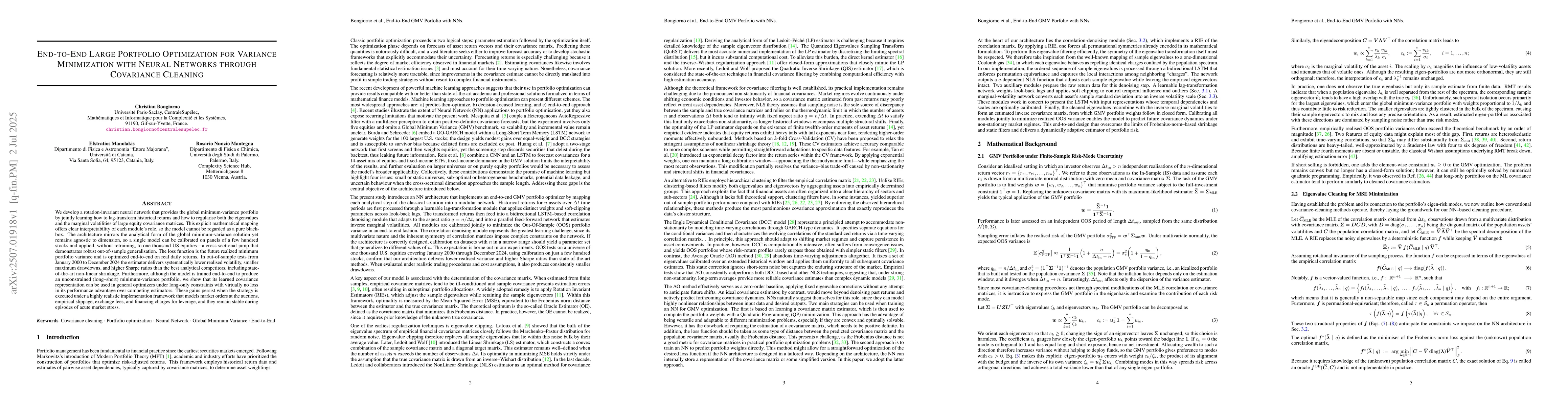

End-to-End Large Portfolio Optimization for Variance Minimization with Neural Networks through Covariance Cleaning

We develop a rotation-invariant neural network that provides the global minimum-variance portfolio by jointly learning how to lag-transform historical returns and how to regularise both the eigenvalue...