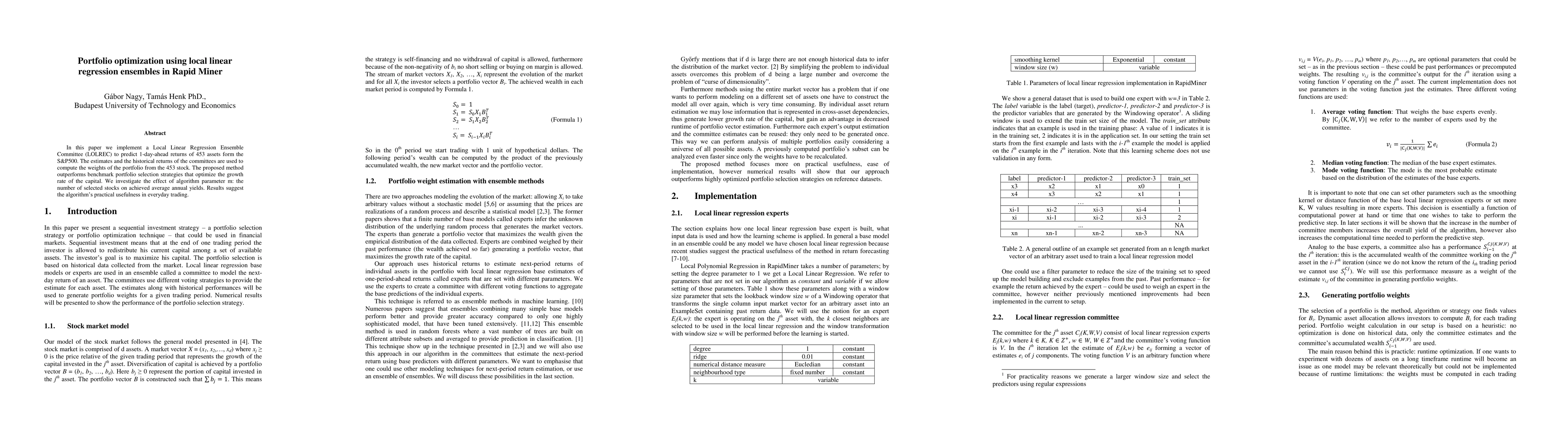

Portfolio optimization using local linear regression ensembles in RapidMiner

Publication

Metrics

Paper Preview

Abstract

In this paper we implement a Local Linear Regression Ensemble Committee (LOLREC) to predict 1-day-ahead returns of 453 assets form the S&P500. The estimates and the historical returns of the committees are used to compute the weights of the portfolio from the 453 stock. The proposed method outperforms benchmark portfolio selection strategies that optimize the growth rate of the capital. We investigate the effect of algorithm parameter m: the number of selected stocks on achieved average annual yields. Results suggest the algorithm's practical usefulness in everyday trading.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0