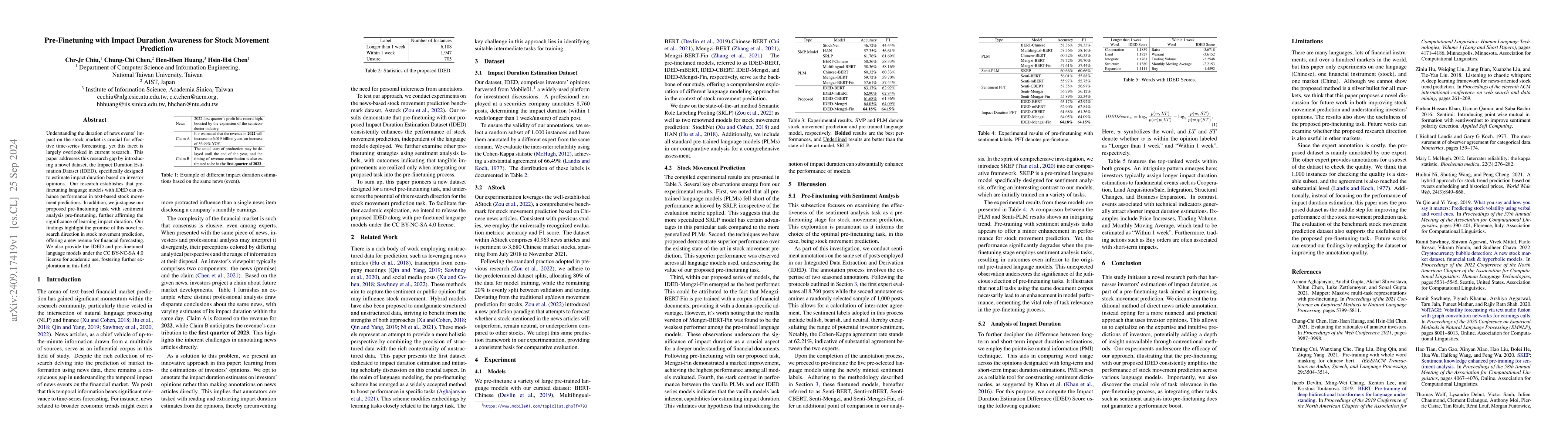

Pre-Finetuning with Impact Duration Awareness for Stock Movement Prediction

Publication

Metrics

AI Quick Summary

This paper introduces a dataset to estimate the duration of news events' impact on stock prices, showing that pre-finetuning language models with this dataset improves stock movement predictions compared to sentiment analysis pre-finetuning. The study highlights a new research direction in financial forecasting.

Paper Preview

Abstract

Understanding the duration of news events' impact on the stock market is crucial for effective time-series forecasting, yet this facet is largely overlooked in current research. This paper addresses this research gap by introducing a novel dataset, the Impact Duration Estimation Dataset (IDED), specifically designed to estimate impact duration based on investor opinions. Our research establishes that pre-finetuning language models with IDED can enhance performance in text-based stock movement predictions. In addition, we juxtapose our proposed pre-finetuning task with sentiment analysis pre-finetuning, further affirming the significance of learning impact duration. Our findings highlight the promise of this novel research direction in stock movement prediction, offering a new avenue for financial forecasting. We also provide the IDED and pre-finetuned language models under the CC BY-NC-SA 4.0 license for academic use, fostering further exploration in this field.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0