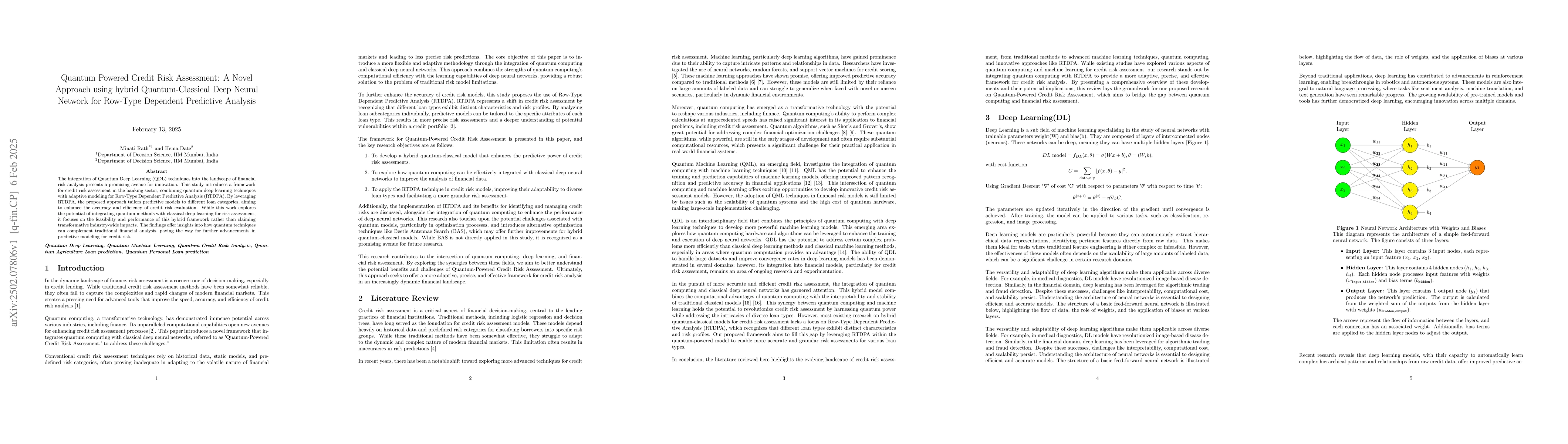

The integration of Quantum Deep Learning (QDL) techniques into the landscape

of financial risk analysis presents a promising avenue for innovation. This

study introduces a framework for credit risk assessment in the banking sector,

combining quantum deep learning techniques with adaptive modeling for Row-Type

Dependent Predictive Analysis (RTDPA). By leveraging RTDPA, the proposed

approach tailors predictive models to different loan categories, aiming to

enhance the accuracy and efficiency of credit risk evaluation. While this work

explores the potential of integrating quantum methods with classical deep

learning for risk assessment, it focuses on the feasibility and performance of

this hybrid framework rather than claiming transformative industry-wide

impacts. The findings offer insights into how quantum techniques can complement

traditional financial analysis, paving the way for further advancements in

predictive modeling for credit risk.

Discussion 0