01

MethodologyHow they did it

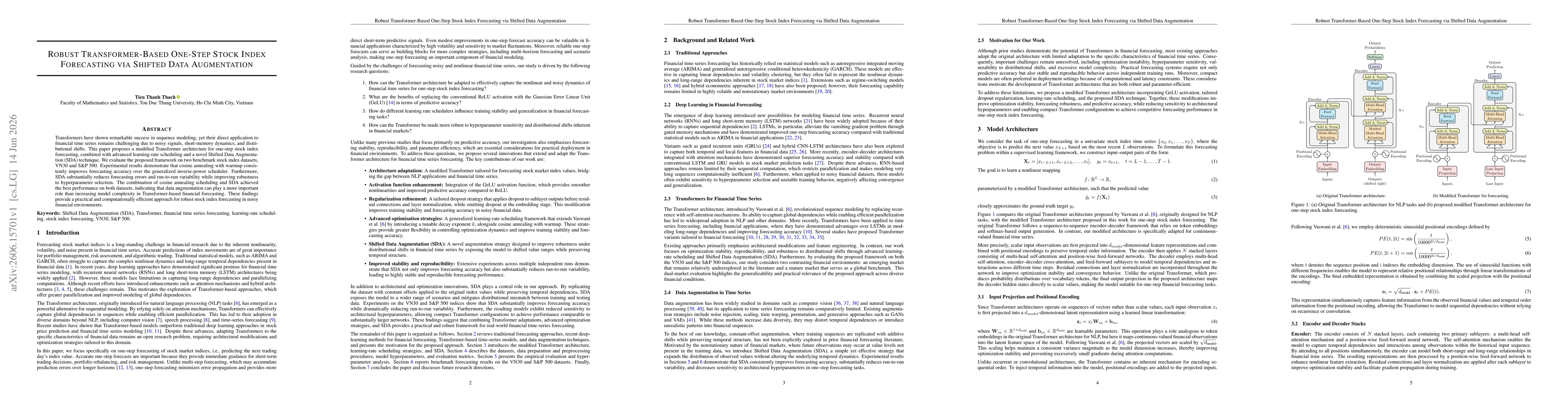

A modified Transformer architecture tailored for one-step stock index forecasting, integrated with an activation enhancement (GeLU), tailored dropout, and advanced optimization strategies including a tunable decay exponent and cosine annealing with warmup. The approach also introduces Shifted Data Augmentation (SDA) to expose the model to drifted value ranges while preserving temporal structure, thereby improving robustness to distributional shifts. Training employs multiple independent runs to assess stability and reproducibility across VN30 and S&P 500 datasets, with evaluation focused on forecasting accuracy and run-to-run variability.

Discussion 0