Temporal Relational Ranking for Stock Prediction

Publication

Metrics

AI Quick Summary

This paper introduces a novel deep learning method called Relational Stock Ranking (RSR) for stock prediction, which focuses on stock ranking and captures temporal stock relations. The proposed Temporal Graph Convolution component models both temporal evolution and stock relations, outperforming existing methods with an average return ratio of 98% on NYSE and 71% on NASDAQ.

Paper Preview

Abstract

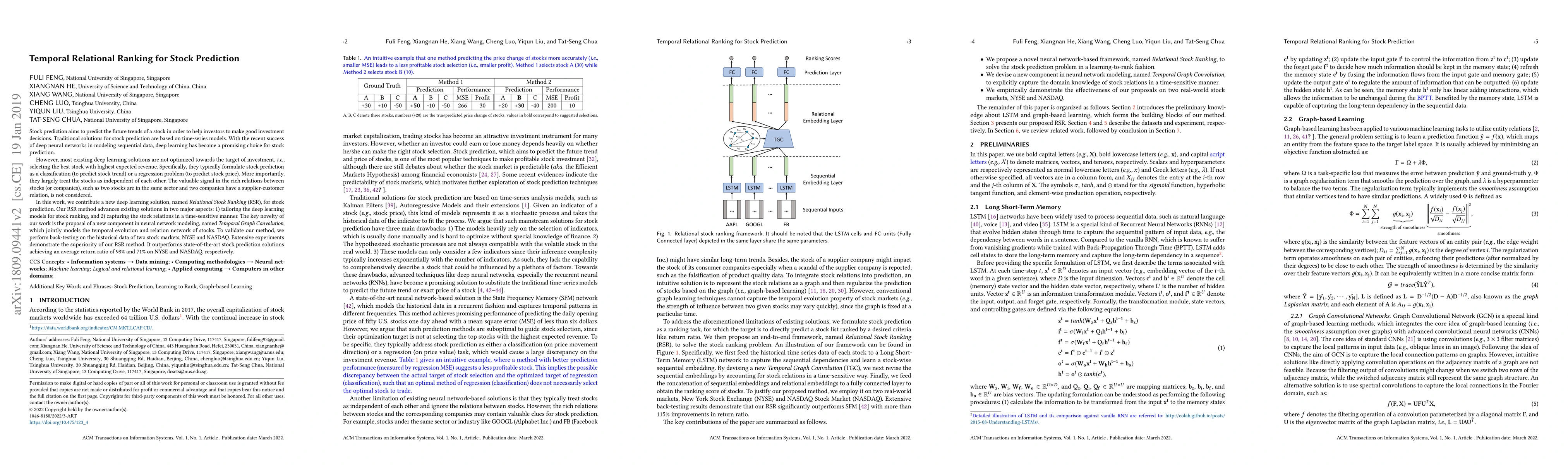

Stock prediction aims to predict the future trends of a stock in order to help investors to make good investment decisions. Traditional solutions for stock prediction are based on time-series models. With the recent success of deep neural networks in modeling sequential data, deep learning has become a promising choice for stock prediction. However, most existing deep learning solutions are not optimized towards the target of investment, i.e., selecting the best stock with the highest expected revenue. Specifically, they typically formulate stock prediction as a classification (to predict stock trend) or a regression problem (to predict stock price). More importantly, they largely treat the stocks as independent of each other. The valuable signal in the rich relations between stocks (or companies), such as two stocks are in the same sector and two companies have a supplier-customer relation, is not considered. In this work, we contribute a new deep learning solution, named Relational Stock Ranking (RSR), for stock prediction. Our RSR method advances existing solutions in two major aspects: 1) tailoring the deep learning models for stock ranking, and 2) capturing the stock relations in a time-sensitive manner. The key novelty of our work is the proposal of a new component in neural network modeling, named Temporal Graph Convolution, which jointly models the temporal evolution and relation network of stocks. To validate our method, we perform back-testing on the historical data of two stock markets, NYSE and NASDAQ. Extensive experiments demonstrate the superiority of our RSR method. It outperforms state-of-the-art stock prediction solutions achieving an average return ratio of 98% and 71% on NYSE and NASDAQ, respectively.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0