01

MethodologyHow they did it

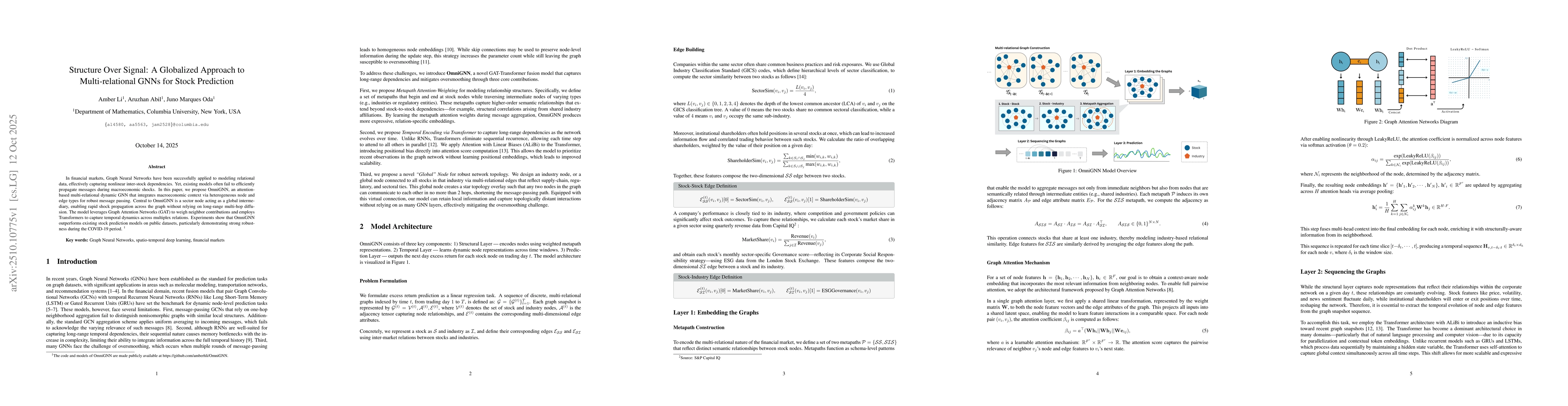

The paper proposes OmniGNN, an attention-based multi-relational dynamic GNN that integrates macroeconomic context through heterogeneous node and edge types. It uses Graph Attention Networks (GAT) for neighbor contribution weighting and Transformers for temporal dynamics across multiplex relations. The model incorporates sector nodes as global intermediaries for efficient shock propagation.

Discussion 0