The public debt multiplier

Publication

Metrics

AI Quick Summary

This paper examines the impact of temporary changes in government debt on economic activity, finding that the debt multiplier is small in normal times but significantly larger during crises. It concludes that fiscal consolidation during recessions is ill-advised, and higher steady-state debt-to-GDP levels can increase real interest rates, aiding monetary policy in combating deflationary shocks.

Paper Preview

Abstract

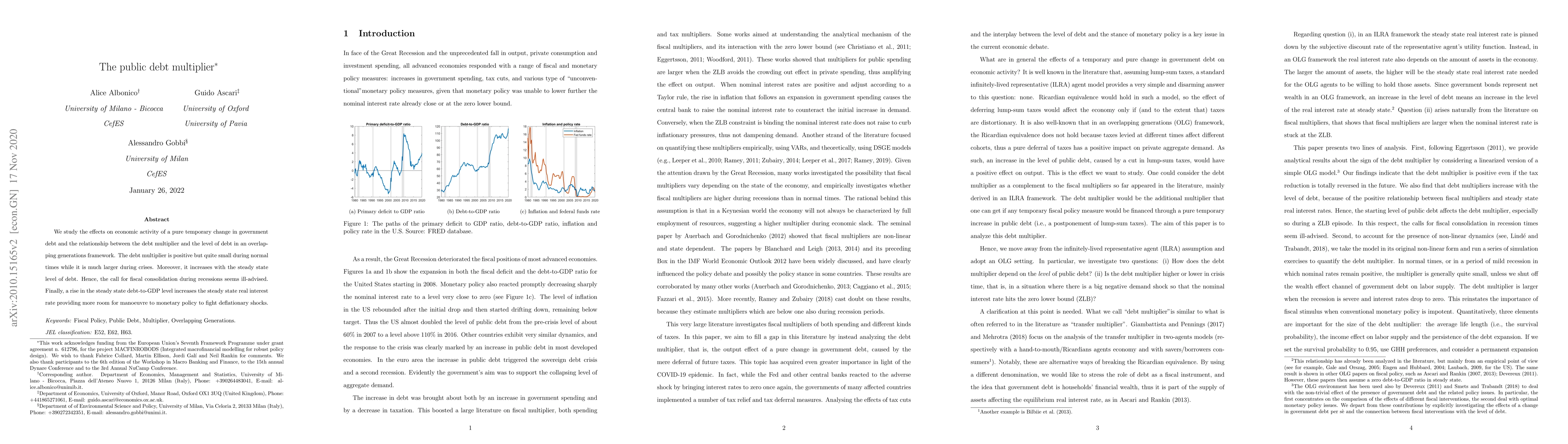

We study the effects on economic activity of a pure temporary change in government debt and the relationship between the debt multiplier and the level of debt in an overlapping generations framework. The debt multiplier is positive but quite small during normal times while it is much larger during crises. Moreover, it increases with the steady state level of debt. Hence, the call for fiscal consolidation during recessions seems ill-advised. Finally, a rise in the steady state debt-to-GDP level increases the steady state real interest rate providing more room for manoeuvre to monetary policy to fight deflationary shocks.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0