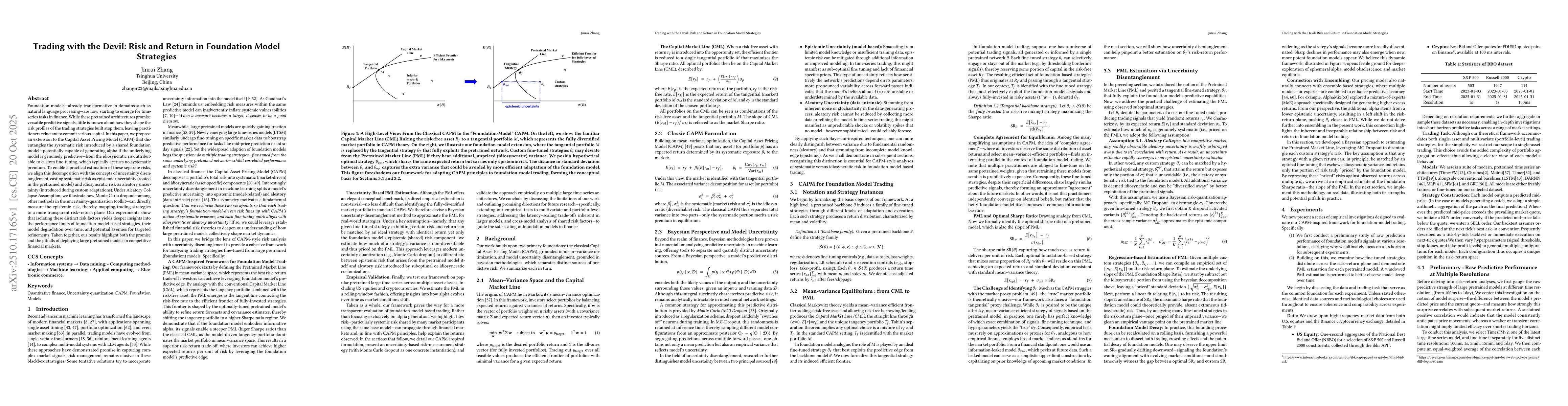

Foundation models - already transformative in domains such as natural

language processing - are now starting to emerge for time-series tasks in

finance. While these pretrained architectures promise versatile predictive

signals, little is known about how they shape the risk profiles of the trading

strategies built atop them, leaving practitioners reluctant to commit serious

capital. In this paper, we propose an extension to the Capital Asset Pricing

Model (CAPM) that disentangles the systematic risk introduced by a shared

foundation model - potentially capable of generating alpha if the underlying

model is genuinely predictive - from the idiosyncratic risk attributable to

custom fine-tuning, which typically accrues no systematic premium. To enable a

practical estimation of these separate risks, we align this decomposition with

the concepts of uncertainty disentanglement, casting systematic risk as

epistemic uncertainty (rooted in the pretrained model) and idiosyncratic risk

as aleatory uncertainty (introduced during custom adaptations). Under the

Aleatory Collapse Assumption, we illustrate how Monte Carlo dropout - among

other methods in the uncertainty-quantization toolkit - can directly measure

the epistemic risk, thereby mapping trading strategies to a more transparent

risk-return plane. Our experiments show that isolating these distinct risk

factors yields deeper insights into the performance limits of

foundation-model-based strategies, their model degradation over time, and

potential avenues for targeted refinements. Taken together, our results

highlight both the promise and the pitfalls of deploying large pretrained

models in competitive financial markets.

Discussion 0