Uncertainty Discounting in Deterministic Black Box Price Predictions for Energy Arbitrage

Publication

Metrics

Paper Preview

Abstract

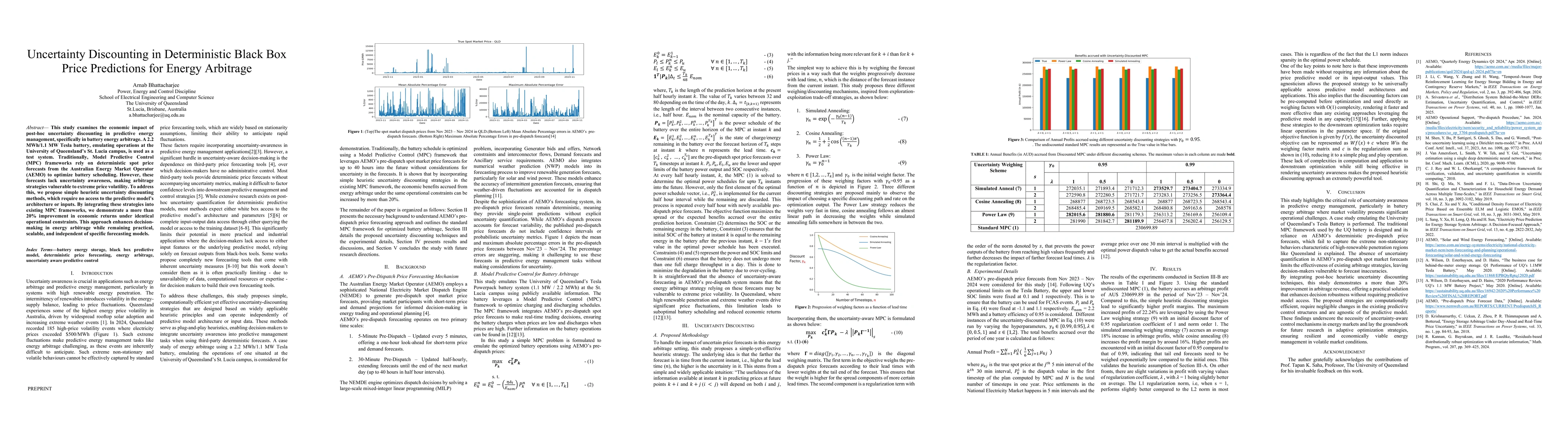

This study examines the economic impact of post-hoc uncertainty discounting in predictive energy management, specifically in battery energy arbitrage. A 2.2 MWh, 1.1 MW Tesla battery, emulating operations at the University of Queensland's St. Lucia campus, is used as a test system. Traditionally, Model Predictive Control (MPC) frameworks rely on deterministic spot price forecasts from the Australian Energy Market Operator (AEMO) to optimize battery scheduling. However, these forecasts lack uncertainty awareness, making arbitrage strategies vulnerable to extreme price volatility. To address this, we propose simple heuristic uncertainty discounting methods, which require no access to the predictive model's architecture or inputs. By integrating these strategies into existing MPC frameworks, we demonstrate a more than 20% improvement in economic returns under identical operational constraints. This approach enhances decision-making in energy arbitrage while remaining practical, scalable, and independent of specific forecasting models

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0