Weak Convergence Methods for Approximation of Path-dependent Functionals

Publication

Metrics

Paper Preview

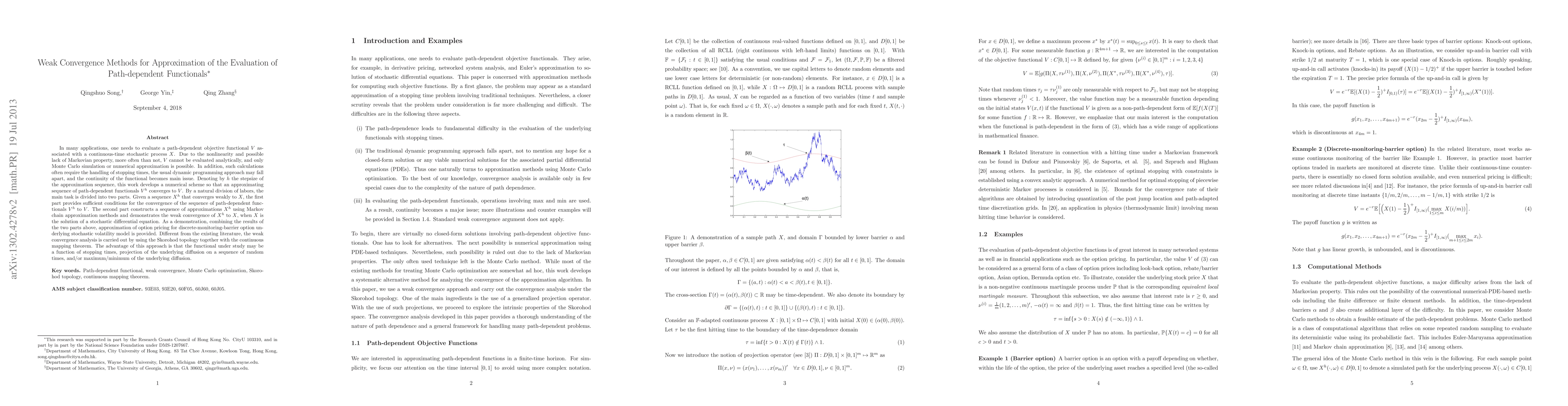

Abstract

This paper provides convergence analysis for the approximation of a class of path-dependent functionals underlying a continuous stochastic process. In the first part, given a sequence of weak convergent processes, we provide a sufficient condition for the convergence of the path-dependent functional underlying weak convergent processes to the functional of the original process. In the second part, we study the weak convergence of Markov chain approximation to the underlying process when it is given by a solution of stochastic differential equation. Finally, we combine the results of the two parts to provide approximation of option pricing for discretely monitoring barrier option underlying stochastic volatility model. Different from the existing literatures, the weak convergence analysis is obtained by means of metric computations in the Skorohod topology together with the continuous mapping theorem. The advantage of this approach is that the functional under study may be a function of stopping times, projection of the underlying diffusion on a sequence of random times, or maximum/minimum of the underlying diffusion.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0