Erratum for: Smile dynamics -- a theory of the implied leverage effect

Publication

Metrics

AI Quick Summary

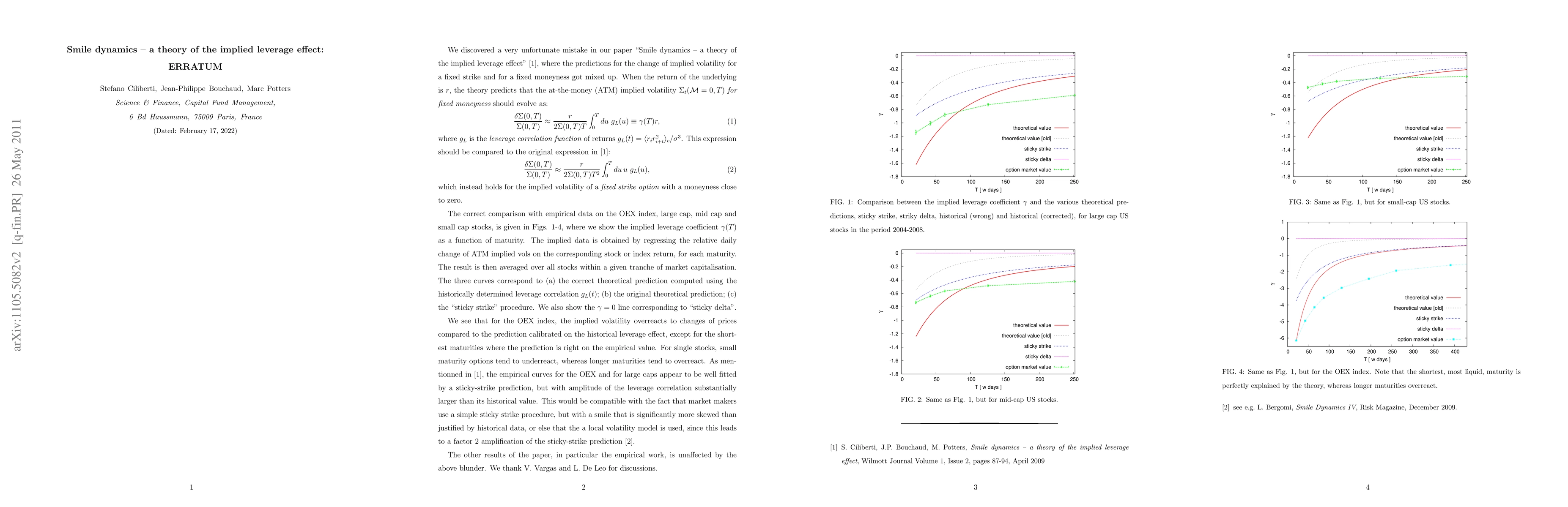

Erratum corrects the original paper's findings on the implied leverage effect, showing that option markets underestimate it for short maturities and overestimate it for long maturities in single stocks, while OEX options are always overestimated except for very short maturities.

Paper Preview

Abstract

We correct a mistake in the published version of our paper. Our new conclusion is that the "implied leverage effect" for single stocks is underestimated by option markets for short maturities and overestimated for long maturities, while it is always overestimated for OEX options, except for the shortest maturities where the revised theory and data match perfectly.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0