01

MethodologyHow they did it

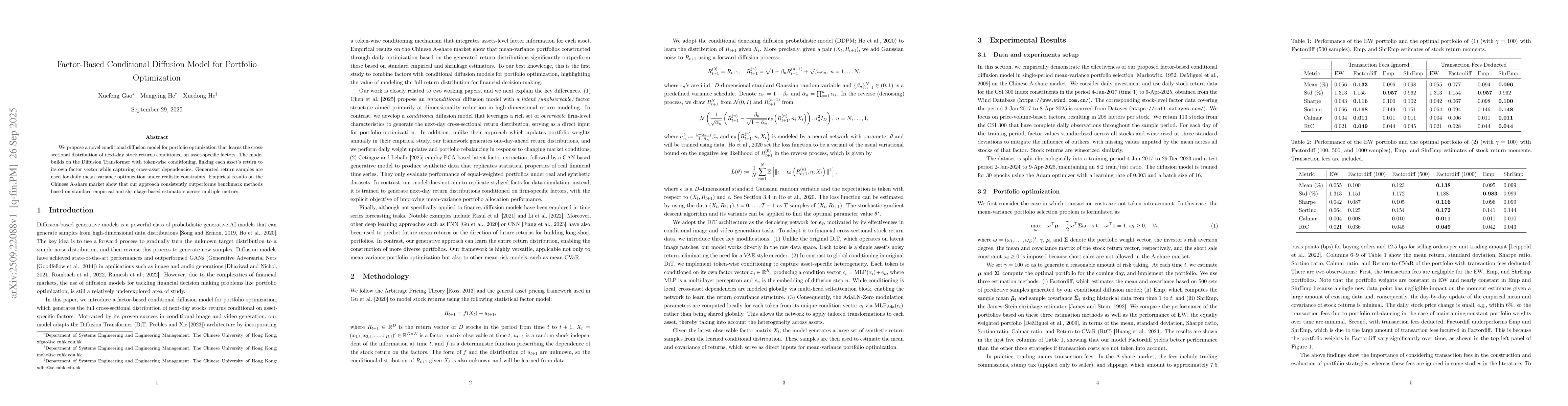

The paper proposes a factor-based conditional diffusion model that learns the cross-sectional distribution of next-day stock returns conditioned on asset-specific factors. It uses a diffusion transformer with token-wise conditioning to link each asset's return to its own factor vector while capturing cross-asset dependencies. Generated return samples are used for mean-variance portfolio optimization under realistic constraints.

Discussion 0