Publication

Metrics

AI Quick Summary

Research finds that stock market values exhibit power law decay over time, indicating a persistence exponent of approximately 0.5, suggesting a moderate level of stability in the market.

Paper Preview

Abstract

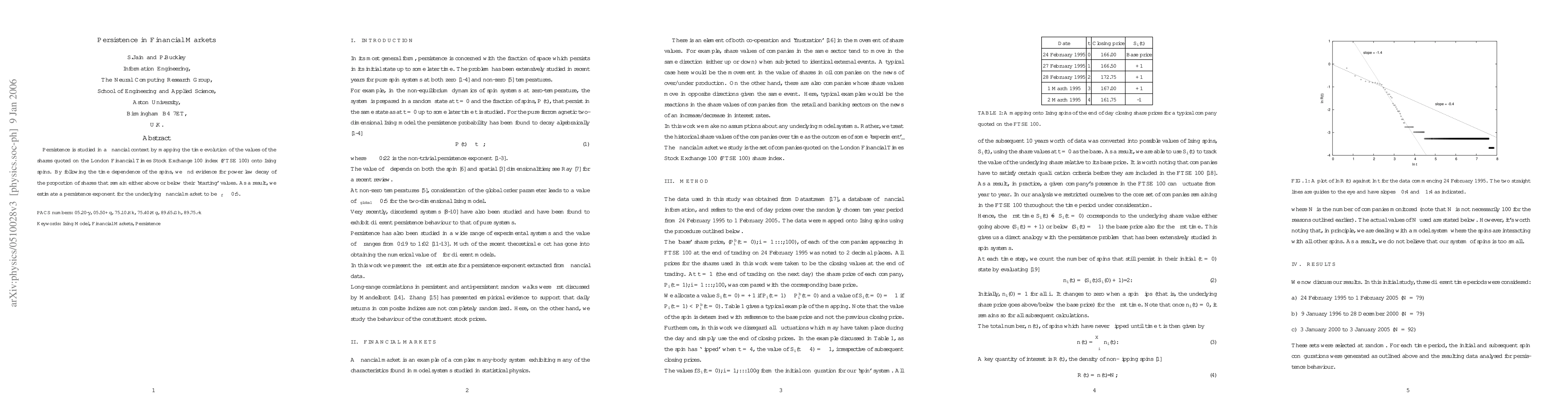

Persistence is studied in a financial context by mapping the time evolution of the values of the shares quoted on the London Financial Times Stock Exchange 100 index (FTSE 100) onto Ising spins. By following the time dependence of the spins, we find evidence for power law decay of the proportion of shares that remain either above or below their ` starting\rq values. As a result, we estimate a persistence exponent for the underlying financial market to be $\theta_f\sim 0.5$.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0