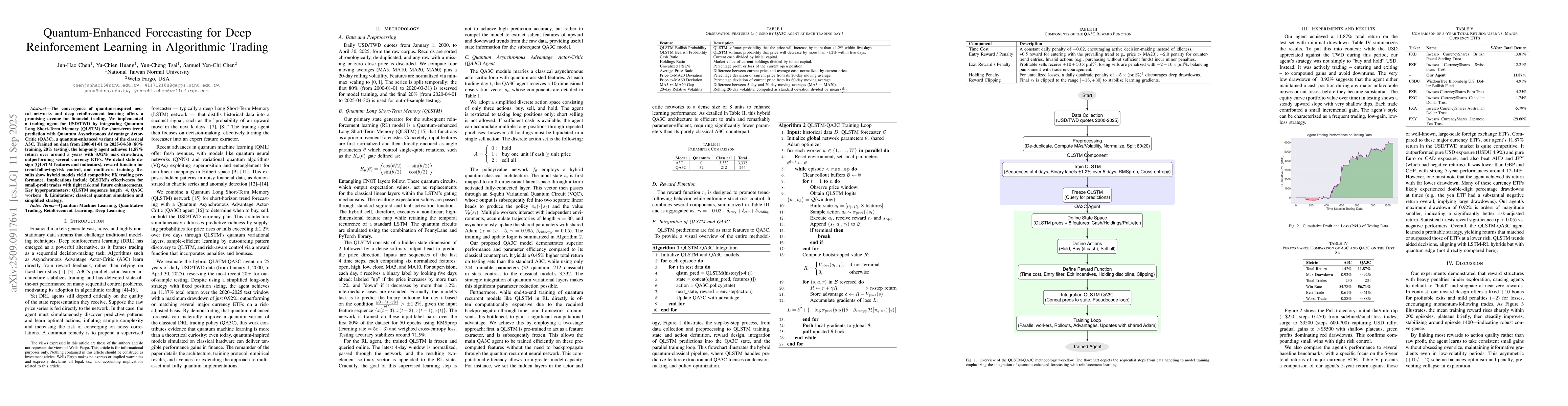

The convergence of quantum-inspired neural networks and deep reinforcement

learning offers a promising avenue for financial trading. We implemented a

trading agent for USD/TWD by integrating Quantum Long Short-Term Memory (QLSTM)

for short-term trend prediction with Quantum Asynchronous Advantage

Actor-Critic (QA3C), a quantum-enhanced variant of the classical A3C. Trained

on data from 2000-01-01 to 2025-04-30 (80\% training, 20\% testing), the

long-only agent achieves 11.87\% return over around 5 years with 0.92\% max

drawdown, outperforming several currency ETFs. We detail state design (QLSTM

features and indicators), reward function for trend-following/risk control, and

multi-core training. Results show hybrid models yield competitive FX trading

performance. Implications include QLSTM's effectiveness for small-profit trades

with tight risk and future enhancements. Key hyperparameters: QLSTM sequence

length$=$4, QA3C workers$=$8. Limitations: classical quantum simulation and

simplified strategy. \footnote{The views expressed in this article are those of

the authors and do not represent the views of Wells Fargo. This article is for

informational purposes only. Nothing contained in this article should be

construed as investment advice. Wells Fargo makes no express or implied

warranties and expressly disclaims all legal, tax, and accounting implications

related to this article.

Discussion 0